Prior Week’s Lessons For This Week: Prime Movers And Threats

Hope Is Trumping Data, The EU Is Recovering, So Why Does Germany Suddenly Want Its Gold Back?

Here’s a:

- Summary of the bullish and bearish forces confronting markets

- Daily breakdown of top market movers

- Our conclusions and lessons for the coming week for global financial market traders and investors, including a not-so-subtle warning from the world’s leading central bankers and Germany’s Bundesbank

The bullish forces remain the bigger market movers, despite the concerns posed by the bearish forces for those long risk assets and currencies.

Quick Summary

The Bullish

- Focus on Japan stimulus

- EU calm continues as markets focus on good German reports, ignore French and other negative data

- US defers debt ceiling and austerity debate until May

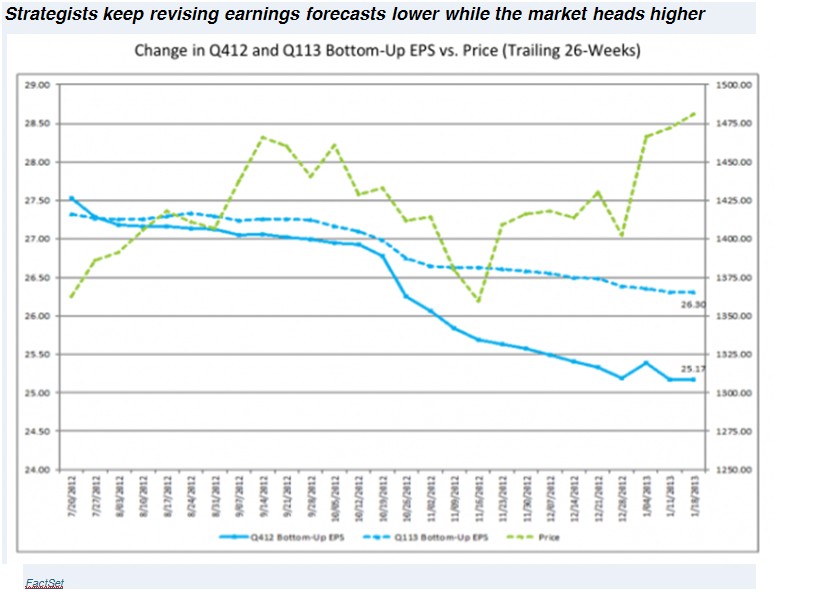

- Earnings falling but beat reduced forecasts and market interprets that as positive

- Prevailing belief greed for yield will outweigh fear of loss from buying at market peak (more on this in our article on coming week market movers)

Bearish

- Most Economic Data

- Technical resistance as risk markets hit decade highs

- Caterpillar burned by yet another Chinese accounting fraud

- Germany wants its gold back and what that really means

Top Market Movers Each Day

MONDAY

Asia was mixed with mostly modest moves up or down as investors stayed cautious on uncertainty about both

- The BOJ meeting that was expected to announce bold a new stimulus plan. Anticipation of this had kept the Nikkei and other Asian markets rising for months, ever since it became clear that the LDP would regain power and pressure the BoJ to cooperate in further stimulus

- A wave of major earnings announcements this week

The only big move was a ~1.5% drop in the Nikkei on cautious profit taking ahead of the BoJ meeting.

Europe was higher for no clear reason, and US exchanges were on holiday

TUESDAY

Asia was down on a combination of disappointment over the BOJ’s announced inaction and sheer ‘sell the news’ profit taking. The BoJ did announce bold new stimulus plans, however it also said none would be implemented in near future.

Europe was down on a combination of the effects of that BoJ announcement and continued caution ahead of major earnings announcements.

The US was up modestly due to both some big name earnings beats (DD, TRV, VZ) and relief over the anticipated passage of a Republican sponsored bill to suspend the debt ceiling (and thus defer the political battle and market uncertainty on it) until May 19th.

It was a big day for the British pound sterling after BOD Governor King hinted at (surprise – not) additional QE, saying that q4 GDP would probably be much weaker than in Q3 and that the bank was ready to implement more stimulus.

WEDNESDAY

Wednesday was very similar to Tuesday

Asia was again mixed with modest up or down moves, and again saw the Nikkei dive ~2% on continued disappointment that no new stimulus was coming any time soon.

Europe closed mixed with minor up or down moves, largely ignoring the only major news of the day, good earnings results from Unilever and Novartis.

US indexes were up a bit, again on relief over the Republicans’ willingness to defer the debt ceiling fight until the spring. Better than expected earnings from IBM, Google, and AMD also helped a bit, and so US indexes edged closer to their October 2007 all time highs.

Despite all the happy talk about the EU and the continued climb of global risk asset markets, the IMF reduced its 2013 global growth forecast, echoing the World Bank’s view from last week that global growth would be less than previously anticipated in 2013. The main reason for the IMF’s reduced expectation was risk of a potential contraction in the ‘improving’ Euro-zone.

THURSDAY

Asia was mixed. Better than expected Chinese manufacturing data boosted Japan, yet ironically Chinese indexes were down, as was Korea’s. Many consider Korea to be a leading indicator of overall global economic health.

Europe was mostly higher as it focused on strong German and EU manufacturing and services PMI reports, and shrugged off weak French factory data and Spain jobs reports, perhaps because these were expected to be weak, and because the big question has been whether Germany, Europe’s economic driver and paymaster, was holding up under the overall EZ slowdown. Some traders suggested that the recent rally in stocks and the EUR has caused many shorts on these to be closed, which has helped boost EZ markets and the EUR.

The US closed essentially flat. Its biggest cap stock, Apple, plunged 12% on a disappointing earnings report Wednesday after the close, so the relatively mild damage could be taken as a sign of resilience.

FRIDAY

Asian indexes were almost all solidly higher, up around 1% (except for China which was flat-to-lower) on continued Yen weakness following comments from BOJ governor Shirakawa and the December BOJ meeting minutes, both of which reminded markets that the bank is worried about Japan’s economy, doubts it can easily achieve its 2% inflation target and so remains strongly dovish and plans “powerful easing.”

European markets were also solidly higher on

- A better than expected German Ifo business confidence report, which confirmed the earlier German ZEW survey’s message of German economic health and boosted hopes that Germany growth could exceed expectations despite recent dour outlooks on the EU from the World Bank and IMF.

- Larger than expected bank repayments of emergency LTRO loans, which suggests the European banking sector is healthier, that greater confidence in it, and by extension the EU, is justified.

These latest data points, along with the continued uptrend of most risk asset barometers like global stock indexes like the S&P 500, and falling GIIPS bond yields, combined to drive the EURUSD breakout above strong resistance around 1.34.

US markets also closed solidly higher, aided by the above bullish developments in Asia and Europe, as well as some strong earnings reports from big names P&G and Halliburton.

CONCLUSIONS

So here’s what the above tells us about last week and the coming weeks.

Last Week’s Top Market Drivers

1. Anticipation of and reaction to BoJ stimulus- Bullish: After initial disappointment that the much anticipated stimulus from the BoJ would not be implemented in the near future, remarks later in the week from senior officials assured markets that aggressive easing is coming, and that kept the Yen falling and stocks in Asia and elsewhere rising.

Earning results and market response-Bullish: The tone stayed positive and markets chose to ignore the overall decline in performance as companies ‘beat’ recently reduced forecasts.

01 jan 26 2331

(via businessinsider.com)

3. Republicans Back Down For Now On Debt Ceiling-Bullish: Relief Wednesday-Thursday following Republican’s willingness to suspend the debt ceiling until May 19, thus deferring once again any moves to reign in the US deficit that could dampen bullish sentiment, added to near term bullish sentiment.

4. Regarding The EU, Markets Focus on the Good, Ignore the bad-bullish: The big EU data dump this week was decidedly mixed.

- The Bullish

- German ZEW and Ifo surveys beat expectations, as did its manufacturing and services PMIs. These helped lift markets Thursday and Friday

- Larger than expected big-bank repayment rate of LTRO emergency loans

- The Bearish: Everything else, but markets ignored them as stocks and the EUR drove higher:

- France factory and services PMIs missed badly

- Spain’s joblessness and Italy’s retail sales deteriorated

- UK data was bad enough for the BOE to be openly considering new stimulus

- The IMF cut its growth forecasts for the EU citing contraction risk, echoing the same thoughts issued by the World bank the week before.

Lessons For The Coming Week And Beyond

Here’s what last week tells us about this week.

EU Calm, Stimulus Provide Hope, Outweighing Reality

Here’s how the bullish bearish forces align for this week and beyond.

Bullish EU Calm

In sum, as long as GIIPs bond rates remain low and there are no near term solvency issues, markets aren’t pricing in risks of future trouble that is likely given that nothing in the EU has been fixed.

The EU has been the big source of bearish anxiety of the past years, so as that big source of worry is off the menu, and markets continue to rise with headlines of real (the Fed), promised (ECB, BOJ) unlimited easing, or the possibility of more to come (BOE, RBA), the current rise in risk assets despite deteriorating economic data looks ready to continue even as markets edge closer to all time highs.

Indeed at the end of the day banks and other investors are swallowing ever growing amounts of bonds from assorted GIIPS nations that can’t repay their current debt loads. Greek bondholders have already taken a ~90% ‘voluntary’ (don’t you dare call it default) haircut on their bonds, but those losses are small change compared to the damage EU banks will take on similar hits to their Spain and Italy bond holdings.

No one is worried about default given those consequences. Of course they’ll get paid; the ECB can print all the Euros it needs. What’s some currency debasement compared to crashing Europe’s banking system?

The only question is whether those Euros will still be close to their current value, and whether bond markets will want higher rates to compensate for that risk. Morgan Stanley’s chief currency strategist Hans Redeker thinks not, and predicts the EURUSD hits parity within the next 2 years. At current levels, and the EURUSD uptrend is widely expected to go higher yet, that’s about a 25% hit just on the currency loss. However that’s a longer term risk, and markets aren’t moving on such considerations.

Given that risk, do EU stocks still look cheap?

Central Banks To Markets: Hedge Your Currency Risk While You Still Can

I deliver this message almost weekly in words simply because the Fed, BOJ, ECB keep delivering it by their actions. This week BOE head King joined his colleagues, as noted in above for Tuesday.

For anyone with most of their wealth tied to or denominated in the EUR, Redeker’s under-reported interview is a stark warning to take advantage of the ongoing EUR rally to diversify out of the Euro. The same goes for those whose wealth is mostly in USD and JPY. For those holding Yen, remember that the BOJ is actively trying for 2%/year inflation, and the Fed is rumored to be fine with inflation up to about 3%.

See here or here for a layman’s guide on safer, simpler ways to protect yourself against a debased EUR, JPY, or USD (while you still can) than generally found in the forex or foreign investing advice industry.

Bullish Anticipation of More Easing

Many may not believe the risk asset rally has legs, but while so many big central banks continue to ease, no one is selling against the current uptrend.

Bearish Growth Data, Technical Resistance, Geopolitical Risks

Sure, earnings are lower, growth is falling, leading global stocks are edging closer to decade highs, and there’s potential military conflict in the South China Sea and in multiple Mideast hotspots. That doesn’t inspire confidence, but these conditions have been in place for a while and haven’t brought the widely anticipated correction.

Not Market Moving But Noteworthy

Investing in China: Growth Vs. Fraud Risk

Despite China’s world leading growth figures (7-8%) even as it slows, we had yet another story illustrating why hedge fund manager Whitney Tilson (among others) has called China “completely uninvestable” due to the difficulty in getting reliable data

Caterpillar announced it found accounting fraud at its Chinese subsidiary and will taka Q4 non-cash charge of ~ $580 million. See here for details. They key lesson here is that if Caterpillar, one of the largest multi-nationals in the world, with its ample staff of accountants and consultants, got burned by a Chinese company run by American executives, what chance to ordinary investors have to accurately value China’s businesses or economy?

Ultimately China is still a totalitarian-run economy that lacks the checks and balances of independent third party oversight that’s standard (though far from flawless) in more open societies.

Merkel’s Party Election Loss Raises EU Risks

German Chancellor Merkel’s party lost a regional election that it was expected to win.

She has walked a tightrope over the last few years, on the one hand promising German funding needed to keep the EU together, yet on the other trying to do so turning the German voters against her and the EU.

To do this, Merkel has maintained a position of “we’ll fund the loans or agree to Euro printing and debasement, provided conditions (that keep up hope that German taxpayer funds will be repaid) are met.”

She’s now less capable of promising funds and will need to play more market-scaring hardball with the GIIPS until at least after the September elections. That could be a problem if significant new funding or printing is needed before then.

German Gold Repatriation: The Disturbing Message

Germany announced this past Wednesday that it’s repatriating gold stored in the US and France. Of course this came with the predictable statements about the move having nothing to do with a lack of trust. However Germany’s actions clearly indicate the opposite.

As Graham Summers of Phoenix Capital Research notes in his most recent biweekly (paid subscription) newsletter, The Great Hangover, the message was clear. Germany is prudently preparing for the possible chaos of an EU breakup. In his recently newsletter he writes

Since the autumn of 2011, it has:

1. Implemented legislation that would permit Germany to leave the Euro but remain a part of the EU.

2. Revived its Special Financial Market Stabilization Funds, or SoFFin for short, allocating 480 billion Euros to the fund (and also providing German banks with a place to dump their Euro-zone Government bonds if they need to).

3. Implemented reforms that would allow it to close off its borders for as long as 30 days if it needed to (so individuals and capital couldn’t leave Germany).

4. Created a working group to assess both the economic impact of a Greek exit from the Euro as well as how to manage the impact of a collapse in France.

5. Pulling all of its Gold from France as well as a major portion of its Gold from the US.

All of these are verifiable facts that the Western Media has avoided talking about. It is very easy to connect the dots here: Germany is implementing a contingency plan to put a firewall around its financial system for when the EU finally breaks down.

What’s interesting is that the gold is that the Bundesbank’s deadline is 2020.

Why is it willing wait? Because it knows the gold has been pledged as collateral for derivative contracts, which can’t be unwound without sending the price of gold soaring, which would bring all kinds of very destabilizing consequences. Failing confidence in fiat currency is the last thing global leaders want at a time when so much of the developed world needs to print money and issue debt at low rates.

Fortunately the Bundesbank is a responsible player with a stake in the current system, and so is willing to be patient for now.

Indeed, given the rather extended eight year deadline, it’s possible that the whole announcement is just to serve as a warning to the US and France.

However, the not inconceivable risk (especially when EU solvency concern returns) is that this patience wears thin, or other players with less patience show up at the gold window.

Just sayin’.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.