Lessons For This Week: 24 Fundamental, 2 Technical Market Drivers

Part 2 of 2: Lessons and Conclusions

See here for part 1, a day by day breakdown of the week’s top market movers, on which we base the following lessons and conclusions for the coming week.

See also special report on USD’s changing behavior, and what it does and does not mean.

Fundamental Market Drivers: 5 Bullish, 20 Bearish

First let’s review the balance of bullish and bearish factors.

5 Bullish Fundamentals

As we’ve noted in the past weeks, the combination of ongoing stimulus from the governments of most of the major developed economies has fed Greed, while a dubious calm about the EU debt crisis and US sequestration has starved away the fear.

There are other arguments that support continued gains for stocks and other risk assets. Highlights include:

- US and EU stocks will prosper by selling to faster growth emerging markets. However because most of these EM nations grow by exporting to the developed world, we wonder how solid that reasoning really is.

- The feared cutbacks in consumer spending as payroll taxes increased haven’t happened, at least not yet.

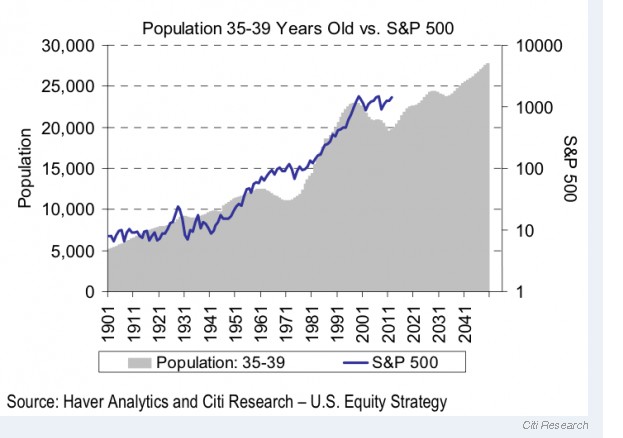

- “Echo boomer,” (children of the baby boomers) are entering their prime investing years. This is one of the more compelling long term bullish stories, assuming the generation experiences enough growth to have what to invest.

05 mar 09 21 52

Source: Citi, Business Insider

- Stimulus Hopes: Although 5 central banks this week held rates steady, most continue to believe that more stimulus is coming, not just from the US and Japan, but also the EU and UK, with others such as Australia and China making occasional noises about being ready to do more if needed.

- Technical Momentum Feeding Bullish Sentiment? In other words, rising stocks and other risk assets are tempting more money into the market.

- US jobs reports feed US recovery theme, US struggling but looking best of developed world.

See here for more arguments cited by the bulls.

19 BEARISH FUNDAMENTALS

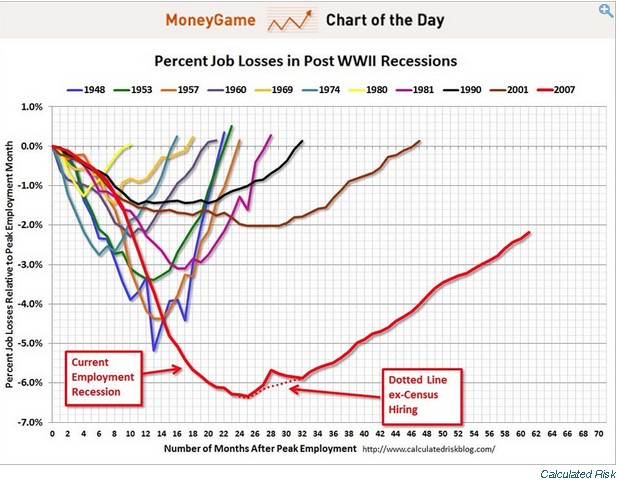

- Jobs Recovery Remains Weaker Than Believed: For example, Bill McBride of Calculated Risk posted his monthly chart that compares the current employment recovery versus that of earlier recessions and put its true weakness into perspective.

Source: Calculated Risk

01 Mar 09 2014

The key point: the current weakness in the jobs market from this recession is still deeper and slower to recover than in past recessions due to the dual ongoing effects of the collapse in the housing and financial sector, both of which are also recovering at a slow pace.

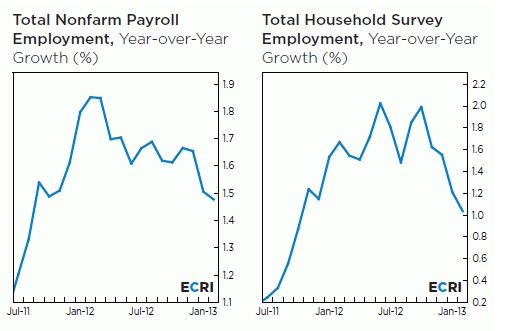

- ECRI’s Lakshman Achuthan posted a presentation on ECRI’s website that concludes that year of year jobs growth in the US has been falling since mid 2011.

02 Mar 90 20 33

On Friday March 8th he also issued a full report arguing the US entered recession in July 2012. In essence he argues that (we continue the above numbering)

- In mid 2012 US growth fell below the minimum needed to keep the economy from stalling and contracting into recession

- That the current indicators used to suggest recovery are either temporarily distorted or are worse than they appear when placed in the correct context.

- That we’ve seen improving housing data and stock prices in prior recessions

- Prices of exchange traded assets can (and are) inflated by monetary policy

- Consumer and business sentiment remains recessionary

- Even the optimistic CBO economists have been cutting growth forecasts

- The number of firms with consecutive quarters of earnings decreases is growing to a degree seen only during recessions.

- Velocity of money has fallen to levels seen only in prior recessions, despite the assorted QE programs, showing that Fed policy has been losing effectiveness since 2011, in contrast to popular belief that as long as exchange traded asset prices remain high, stimulus must be working.

See the above link for the full report

While we’re on the topic of bearish things to consider as a counterpoint to the prevailing bullish sentiment and momentum, just keep in mind the following reasons to curb your enthusiasm.

- Too Much Borrowed Money/Margin Debt A Red Flag

–From Pragmatic Capitalist: Much of the rally in stocks since 2009 has been fueled with borrowed money, and margin levels are rising at accelerating rates. That’s dangerous because it means that once a pullback begins (and a perfectly normal 10 % pullback on the S&P 500 wouldn’t even break the current uptrend on its weekly chart), it can start a chain reaction of margin calls that force selling, which brings lower prices that force more margin call generated selling.

— BofA Merrill Lynch technical analyst Mary Ann Bartels said last week that NYSE margin debt was sending a sell signal. “The last time a sell signal was generated was on April 2010 and the S&P 500 subsequently corrected by 16% in two months.”

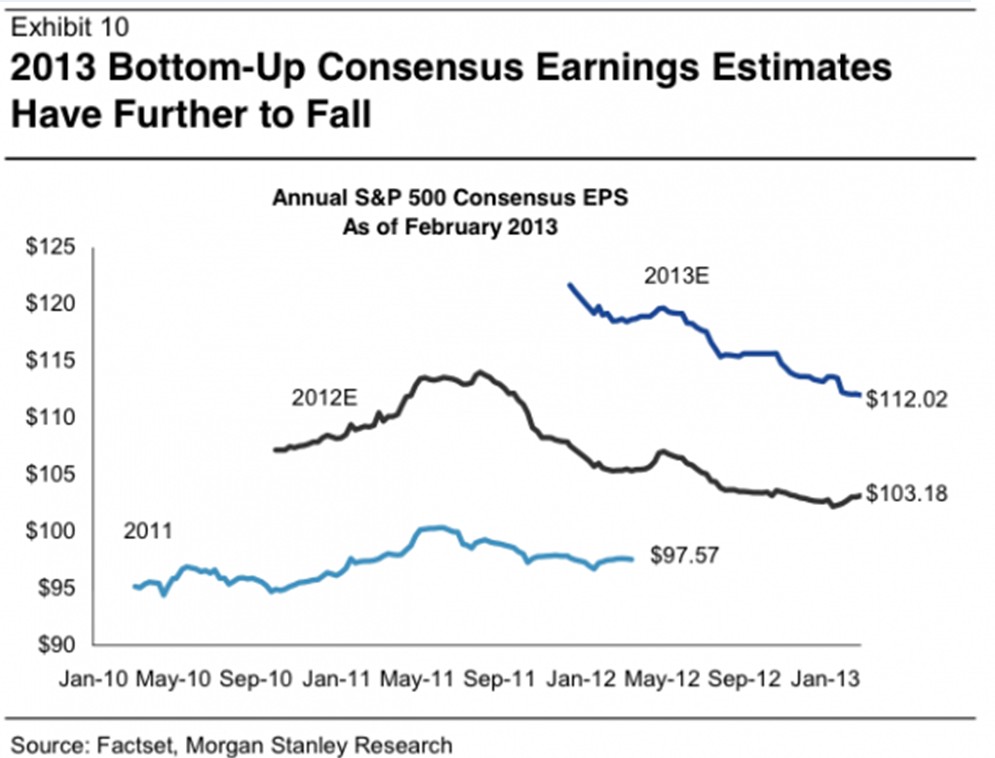

- Earnings growth expectations are the key drivers of stock prices, and they are falling.

04 Mar 09 21 17

- Profit margins are at record highs, and are expected to go higher. However they tend to be mean reverting, meaning they should fall.

- US stocks are, by an assortment of measures, among the most expensive in the world. That differential also tends to revert to mean.

- While weekly flows of funds into equities (aka the great rotation) are seen as a leading indicator of more gains, historically they are a lagging indicator that follow, rather than predict, stock market performance.

- Assorted investor sentiment readings are exceptionally high, which can be a warning that the supply of new buyers to fund future gains is waning.

- Trading volumes are low by historical standards, which confirms the above suspicion that the supply of new buyers may be running out.

- As I pointed out a few weeks back here, the last two times stocks were at these levels, they fell hard. Is it different this time? Yes, but not the way you’d want it to be. Supporting fundamentals of virtually every kind (growth of GDP, jobs, PMI readings, earnings) are deteriorating globally.

- Italy remains a potent disturber of that calm. We’ll know more in the weeks ahead

In sum, stocks and other risk asset prices collapsed when they hit these levels in 2000 and 2007, so markets remain vulnerable to any kind of bad news that can’t be fixed by quick money printing.

Technical Picture Remains Mixed: Bullish Strong Upward Momentum Vs. Bearish Resistance

Bullish: As we’ve noted repeatedly in recent articles, most global indexes are in up trends backed by established rising momentum on their weekly charts.

Bearish: The bellwether global stock indexes are hitting resistance that has been tested twice in 2000 and 2007, and held. Momentum then too was strong, as it tends to be near such long term highs.

US Jobs Reports Help Rallies, Europe Reacts Better

The monthly US jobs reports supported risk assets, for reasons unknown, more so in the EU than the US. Perhaps that’s because US traders had more time to digest them and see how much progress remains to be done, as noted above. The report came out before the start of US trading, whereas in Europe it fell within the final hour and traders had only time for quick reaction.

Conclusions And Lessons

So what did we learn for this week?

Stimulus, Momentum Stir Greed, EU Complacency Dampens Fear

As noted above there are only two things supporting this rally, and while they could indeed continue for a while, neither is sustainable for the long term:

–Ongoing stimulus: admittedly it can and likely will continue for years, until bond markets start demanding more interest to compensate for the risk of being paid in less valuable money. This is feeding the Greed that powers assets higher.

–Ongoing calm about the EU, which remains a giant confidence game with overleveraged banks holding increasing amounts of garbage debt. EU’s banking system remains shaking. For example in recent weeks LTRO repayments have been about half of what the ECB expected, suggesting liquidity is not great. Prevailing calm about the EU is quelling the primary Fear that has restrained asset prices in recent years.

Big Themes In Forex And Ramifications

There were a few things of note for all investors, even those who ignore currency markets.

Central Banks Disappoint Hopes For New Stimulus – For Now

All of the 5 central banks that held monthly rate announcements this week, which disappointed some. It wasn’t so surprising, really.

Both the BoJ and BoE have new incoming bosses, so no changes will be made until they settle in.

While many thought the ECB might do something, we suspect it will hold off on any EUR debasing action unless there is a very compelling need. Why? German PM Merkel has elections this fall, and Germany leaders will likely be more pliant about weakening the EUR after their jobs are secured.

USD Set To Benefit As Both Risk And Safe Haven?

One of the most potentially important charts of the past week came from Morgan Stanley’s currency team, which in essence suggested that the USD may be evolving from a safe haven currency into a risk currency.

That means that how the USD both influences and is influenced by other markets could be reversing its normal behavior.

Given the profound affect such a change could have across a variety of markets in addition to forex, we’ve dedicated a separate article to this topic. See it here for full details

Key Conclusions

Market Risk Complacency

As noted above, the extent of bullish sentiment seems unjustified given the prior market experience at these levels. How much do you believe in stimulus? The only ones who should be going long are:

- Short term traders

- Long term income investors who with long time horizons who can ride out a long downturn, or are able to keep disciplined stop losses on their holdings

Informed Investors Need A Basic Understanding Of Currency Markets

As governments continue to attempt to manipulate their economic performance via manipulating their currencies, however well intentioned they may be, it’s more important than ever for investors to understand the basics of what drives currency markets and how they influence other markets and signal changes in those markets.

Diversify Your Assets By Currency As Well As Sector And Asset Class

Don’t get distracted by short term currency movements. As long as the folks at the Fed, ECB, BoJ and BoE believe want to cut the value of the USD, EUR, JPY, and GBP, then all of them are going to lose ground against both hard assets and better managed currencies. The same goes for any other currency subject to similar dilutive policies.

Anyone heavily exposed to these currencies will see their wealth dragged down with them. Just because you spend in that currency does not at all insulate you from the effects of a devalued currency (though I’m constantly amazed at how many bright people think otherwise). Just think about how many goods and services you buy either contain imported inputs or inputs that are subject to global prices.

Fortunately you can achieve both of the above without a lot of work, and you don’t have to get involved with demanding, risky styles of currency trading. There are ways to benefit from currency trends that are no riskier or more demanding than stocks or bonds (ok, perhaps not the best recommendation these days). See here or here for more information about my book, written specifically to help with both, or just search The Sensible Guide To Forex. It recently sold out at amazon and other online retailers after winning Best Forex Book For 2013, but should be restocked shortly.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.