The Coming Week: 12 Market Drivers To Watch

This is the most event packed week thus far in 2013. Here’s a brief rundown of what’s coming.

Fundamental Picture

There are significant top-tier events from all of the top three economic zones this week.

EU

Perhaps the one positive out of the Cyprus mess is that markets now remember that contrary to EU leadership claims, the sovereign debt and banking crisis isn’t any closer to resolution than it was after the ECB’s OMT program was announced in mid 2012.

Complacency about the EU has been a huge plus for risk asset markets, probably the #2 most bullish factor in the global risk asset rally after assorted central bank stimulus programs, actual or verbal. That prop is gone for now.

1. SLOVENIA

Slovenia is the likely spot for a new EU crisis. It is perhaps the biggest sovereign loser out of the whole Cyprus debacle, after Cyprus itself, because it has the most in common with Cyprus, and is likely to need a bailout itself soon.

- Not in a rescue program yet but soon to need one. Events in Cyprus have reminded everyone that it too has an oversized banking sector that’s in trouble. Rising bond yields are the big warning sign of a new EU crisis, and Slovenia’s are up over 40% in the past two weeks thanks to Cyprus.

- Like Cyprus, its request will come at time when conditions make it harder to make a credible contagion threat and thus pressure the EU for concessions, because markets appear to be suffering from a combination of

- Pre German electoral concerns: Most importantly, Europe’s paymasters need to show Germany’s voters that their interests have been well protected. Thus Germany will be sparing with concessions, and force others to bear more of their own burdens than in the past. Indeed, the big winner of the Cyprus affair was likely Angela Merkel.

- Crisis fatigue (they’re less easily spooked by contagion threats, having become used to them and used to last minute deals)

- Unwarranted confidence that the EU leadership knows what it’s doing and has the common good at heart, despite the events of the past week

- It may be too small to present a systemic threat, and so be more vulnerable to a Cyprus-type harsh treatment program. Per assorted GDP rankings Slovenia ranks in the high 70s, right in the middle between of the rankings between Cyprus’ (around # 100) and Greece (#34 – 40).

2. -3. Italy, Cyprus,

Continued lack of a coalition in Italy and Cyprus’s evolving bank rescue (no EU money actually paid out until an official assessment made) should continue to influence markets, mostly in a bearish manner, the only question is when the next headline hits.

For this week, the more likely Italian market moving event may be Italy’s 10 year bond auction. Given the stakes, the EU tends to do its best to insure all looks ok. However after the failed coalition attempts, it may feel that Italy (or more specifically, its President) needs a reminder to do what’s needed and install a pro-EU (i.e. austerity) caretaker government until either a stable coalition or new elections are chosen. Spiking bond yields were the weapon that pried Berlusconi from office, so bond markets may again be the tool for influencing Italy.

As we noted in our review of last week’s lessons for this week here, the significance of the Cyprus deal is that it casts doubt on the safety and liquidity of all GIIPS bank deposits and hence makes them all more at risk of capital flight. Cyprus’s capital controls are officially in place for just seven days, but they’re likely to be renewed into the foreseeable future. The longer they’re in place, the deeper the damage to confidence in GIIPS banks and the bigger the risk of bank runs that by themselves could spark a new chapter in the EU crisis.

4. – 5. EU Calendar Events: PMIs, Bond Auctions

Purchasing Manager Index surveys will provide the latest update on the EU. These are likely to continue to paint a bearish picture of continued contraction for the EU outside of Germany.

Italian and French auctions of benchmark 10 year notes will also provide potentially market moving news from the EU. Italy suffers from deep recession and a lack of a stable coalition to deal with that, so it’s vulnerable to a spike in borrowing costs.

6. ECB

The ECB’s monthly meeting and rate statement are not expected to yield any changes, but any hints at coming easing measures would help boost risk assets and further pressure the EUR. Given the deterioration since the last meeting, most notably events in Cyprus and Italy, as well as spiking bond Slovenian bond rates, a surprise attempt to ease cannot be ruled out.

7. – 8. Other Central Bank Meetings

The big one this week is made in Japan. The Bank of Japan (BOJ) rarely provides much market moving news, but this time it is likely to move both Japanese and related Asian stocks, as wells as the USDJPY and other Yen pairs. That’s because these have been moving (stocks rising, Yen falling) for months now on little else but anticipation of new BoJ easing. The Yen is down nearly 14%, and Japanese stocks are up nearly 20%, since new elections were called in mid-November. That started the speculation about a more pro-easing government and BoJ head. Although new easing steps are expected at this meeting on Thursday, it’s hard to believe the BoJ will exceed expectations, so the trends in the Yen and Japanese stocks could well see at least a short term reversal on profit taking from long Japanese stock and short Yen positions.

The central banks of Australia and England also have meetings and rate statements this week. Any surprises would move their own currencies and indexes.

US

Monthly jobs reports, manufacturing and service PMIs, Fed speeches, as well as speculation on quarterly earnings, all combine to make this week particularly significant.

US monthly jobs reports, as well as those that come earlier in the week and offer hints on the outcome (the jobs components of the PMIs, ADP NFP report, for example), are typically among the biggest events of the month. If anything, these NFP and unemployment reports are even more important than usual.

9. Monthly Jobs (And Related) Reports: The Big QE 3 Indicator

US monthly jobs reports, as well as those that come earlier in the week and offer hints on the outcome (the jobs components of the PMIs, ADP NFP report, for example), are typically among the biggest events of the month. If anything, these NFP and unemployment reports are even more important than usual.

Last week Chicago Federal Reserve Bank Charles Evans noted that he wanted to see 6 consecutive month of over 200k job growth before he’d support any reduction of QE 3. Bernanke probably feels the same way.

QE 3 is the primary driver of the US stock rally in the face of data and earnings that don’t support the current historical high or high levels in stocks, US farmland, and other risk assets.

US jobs reports (ok, retail sales and GDP also important) are the biggest single driver of the decision for when to pare back QE 3, and probably these same asset prices.

The last three months showed 155k, 157k, and most recently 236k for February.

Markets are forward looking, so it will be interesting to see how many months in advance risk asset markets will start pricing in QE 3 withdrawal, and whether it makes investors feel optimistic enough to continue the rally or if it causes a selloff.

Thus far the consensus estimate for Friday’s NFP is just around 200k. A second straight 200k month makes it two out of six.

However it’s not clear how that news would be interpreted. Remember, markets have been moving higher on little besides speculation for continued stimulus for the foreseeable future. A strong report that suggests an early end to that easing could thus be taken as more negative than positive

10. Earnings Season Speculation

Q1 2013 earnings season kicks off with global materials bellwether Alcoa (AA) earnings announcement April 8th, but speculation about it, as well as US earnings in general, could hit even this week. Expectations are not high given the steady stream of downward revisions, so it’s unlikely we get any bearish surprises. Typically, the idea is to low ball expectations in order to allow more companies to beat expectations, which many forget were just recently lowered.

11. China Manufacturing PMIs

Chinese manufacturing PMIs, both the official and HSBC versions, come out Monday and are the only potentially market moving events until the US manufacturing PMI comes out later in the day.

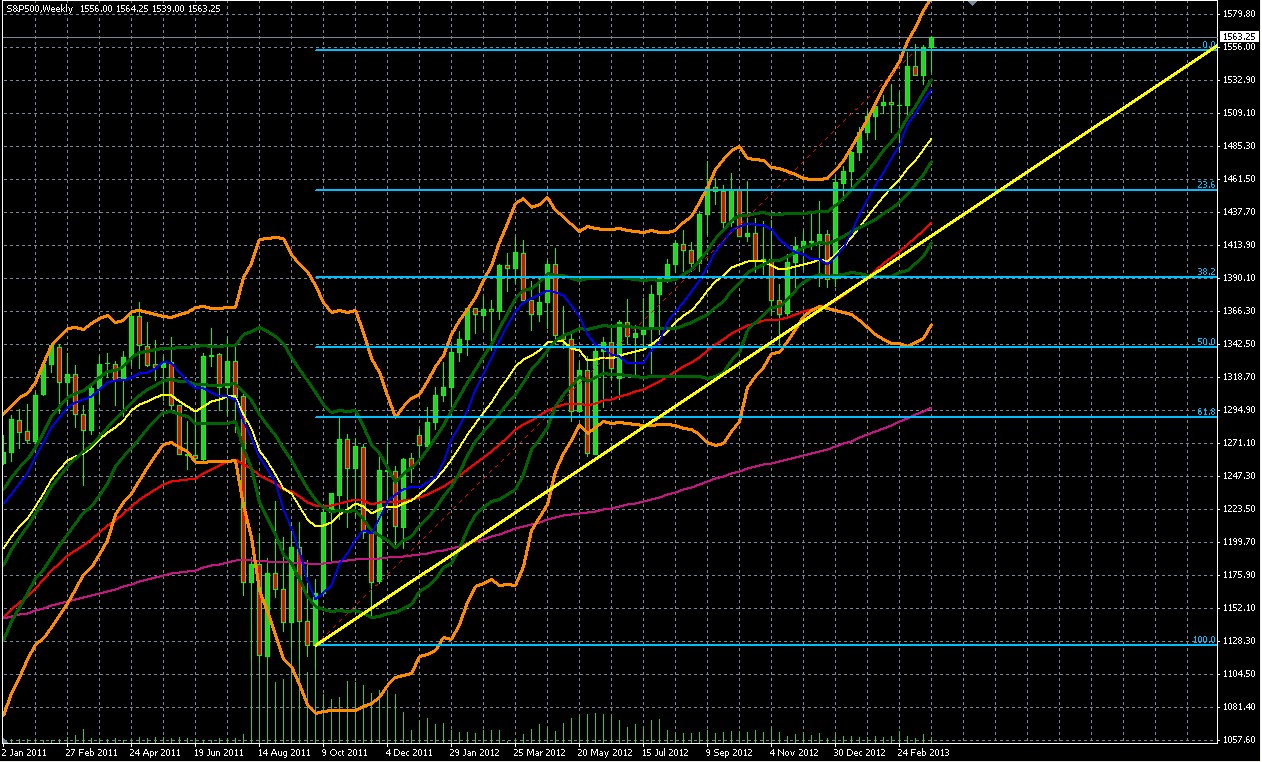

12. Technical Picture: Bullish Momentum Vs. Bearish Resistance At Decade Highs

As in prior weeks, the weekly chart for the bellwether S&P 500 shows nothing but upward momentum.

- Weekly EMAs from 1- to 200 weeks all moving up

- Price firmly in the upper, double Bollinger band buy zone. See here for a quick summary of the rules for interpreting these.

Yes, we’re at decade highs, but we’ve been near them for weeks, so this too isn’t new. In sum, we still have a case of bullish momentum vs. bearish decade-old resistance. Thus far stimulus-fueled momentum and relative outperformance of the US economy has kept US risk assets and, contrary to normal correlations of the past years, the USD, rising higher.

S&P 500 Weekly Chart January 2011 – Present

Source: MetaQuotes Software Corp, thesensibleguidetoforex.com

01 mar31 0515

One True Thing

All of the above event risk brings uncertainty. However one thing is clear.

While the BOJ has talked about easing, so far it’s been nothing but talk. Japan’s central bank is expected to announce actual easing at this week’s meeting. The Fed is already committed to pumping $85 bln per month into the markets. It’s just a matter of time before the ECB and BOE need to start new easing steps to prop up their weakening economies. That may be good for their growth, but it’s likely to drag down their currencies and anything attached to them.

See here for the most up to date guide of simpler, safer solutions than you’ll find in other guides to forex or foreign investing.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.