2013 Outlook Year-End & Beyond: Part 3 – The 4 Rally Killers

Part 3: Four Things Could Send Markets (SPY) Plunging in 2014

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting. We stepped back from our normal weekly focus to form our outlook for the end of 2013 – start of 2014, as part of our preparation for our full forecast for all of 2014. The US government shutdown’s data delay set us back about 3 weeks.

To view other parts click on the following links: PART 1, PART 2, PART 3, PART 4. If your pressed for time, PART 1 and PART 4 are what you need to see now. They provide the overview, summary and conclusions. Then you’ll know if you need to read the rest. PART 2 provides details on what’s needed to keep markets trending higher, and PART 3 reveals what will send markets plunging.

SUMMARY OF BEARISH FORCES

- Taper: Interest Rate Shock, Fears or Actual, Undermine Rally, Recovery

- Stock Valuations: Bubble Fears Rise If Growth, Earnings Data Doesn’t

- Higher Risks Exacerbate Valuation Concerns

- Tail Risks From The US, EU, Japan, China, and Emerging Markets

DETAILS

Here are the details on each of the above.

Taper: Interest Rate Shock, Fears or Actual, Undermine Rally, Recovery

Per Brian Belski and BMO Capital Markets, “almost all bull market corrections are triggered by a Fed rate hike or a spike in oil prices, and both of these conditions are “nonexistent in the current environment.”

Ok, there’s no oil price spike on the scene, and unless the economic data is very encouraging, the Fed is unlikely to Taper until sometime in 2014, for reasons we’ve discussed in depth here.

Still, there is a chance it might begin to curtail QE this year, and even if it doesn’t, because markets are forward-looking, bond rates could start rising anyway.

The Fed is saying it can taper without tightening, essentially by calming markets with forward guidance, a fancy way for saying “we promise to keep rates down even when we curtail QE.”

I have real doubts about that, to put it mildly.

Maybe I’m missing something here, but how do you keep bond rates down if $85 bln/month of fed QE bond buying stops, while new supply keeps coming on the market at the same rate and there is no one else replacing those QE purchases? Wouldn’t bond prices have to drop, and thus rates rise?

In the past markets have not responded well to rising risk of imminent taper. Even if Janet Yellin wants to delay it, even she is unlikely to keep it away beyond March 2014 unless US jobs and growth data start heading down. That’s not expected.

Third, remember the risk that the US is in a “liquidity trap,” which means that withdrawal from QE brings interest rate increases out of proportion to the drop in bond demand from the reduction in Fed bond purchases.

See here for a look at how the revived early taper talk after the FOMC minutes of November 20th have killed off the market for new issues and refinancing of corporate debt.

Looking into 2014, the consensus remains that March 2014 is the likely taper start date, but all that assumes the US recovery continues as anticipated.

Also, as Bernanke explicitly warned last week, if yields on 10 year notes hit 3%, then a taper is back on the menu.

Stock Valuations: Bubble Fears Rise If Growth, Earnings Data Doesn’t

The short version: valuations are uncomfortably high, but that doesn’t tell us anything about when they’ll come down. Here’s the full story.

Every valuation method I know of that have some demonstrated predictive power, indicates that stocks are at least 40% overvalued, which makes them vulnerable to a pullback.

These, include:

- Cyclically adjusted price-earnings ratio (current P/E is 25X vs. 15X average)

- Market cap to revenue (current ratio of 1.6 vs. 1.0 average)

- Market cap to GDP (double the pre-1990s norm)

- Corporate profit margins well above historic mean

Assets can stay overvalued for long periods, so while these strongly point to a coming pullback, they don’t say much about when it will happen. Given the above bullish forces, that pullback is likely to come when we get:

- An interest rate shock when markets believe that the global stimulus festival is ending and/or rates that interest rates are rising anyway ( i.e. central banks lose control of rates) and bonds once again offer competitive returns.

- Energy price shock that imposes a similar large and unanticipated burden on growth and earnings

- Another contagion shock (fear of financial system instability), most likely from another chapter in the EU debt crisis (though possibly from a Japan solvency crisis if that happens first) if confidence in GIIPS/EU/ Japan bonds drops, yields rise, and the money printing that follows, (real or promised) fails to calm credit markets and bring down sovereign borrowing costs to rates that can be repaid. Instead, the money printing causes confidence in the currency to break down.

For further details on how over valued stocks have become, see this piece from John Hussman here, from French bank Societe Generale here (rising 10 year bond rates to halt further S&P 500 increases as they are due to hit 4% by end of 2014), , and from Businessinsider.com Editor Henry Blodgett here.

The message from all is that stocks are due for a correction, but no one knows when. The Societe Generale forecast, even if correct, might not slow stocks down as long as the rise is gradual and accompanied by improved growth and earnings.

On a simple level, the only obvious appeal of equities at this time is the lack of alternatives for yield seekers due to suppressed bond rates from central banks. Intuitively, it doesn’t make sense to have stocks at multi-year or all-time highs when global economic conditions are far from historically good:

Growth and earnings data are mediocre in the US and outright poor in most of Europe (ex-Germany) as well as Japan, and China is slowing down.

For example, since the start of June 2012, the S&P 500 index (SPY) has advanced from about 1257 to its current all-time high of 1790.

In other words, we have seen the S&P 500 Index increase by a remarkable 533 points, over 42%, in just a year and a half, despite a sluggish economy and equally tepid earnings and sales growth (just 1% sales growth in Q3 2013, and much of that was due to acquisitions rather than growth from current operations). This suggests that investors are now willing to pay 42% more today for the same stocks that they could have bought 18 months ago at a much lower price.

You may have heard this argument phrased as “multiple expansion,” that investors are now paying 16.5x trailing EPS, up from 13.7x at the end of 2012. However in all fairness, this is another one of those metrics that is neither necessarily bullish nor bearish. Gluskin Sheff’s David Rosenberg notes here that 16x PE multiples are basically in the middle of the spectrum that runs from around 9x or less (very bullish) to over 25x (bearish euphoria), and that anything over 16x is “generally consistent with single-digit returns thereafter — whether on a one-year or three-year horizon.”

In the end, if growth and earnings data can continue their slow but steady improvement, that might be enough to maintain hope for higher prices that brings in new long investors, as it would maintain the current consensus that stocks are neither cheap nor so overvalued that a big pullback is imminent.

Higher Risks Exacerbate Valuation Concerns

Even worse, investors are paying that much higher price for stocks in the context of increased risk of interest rate and contagion shock, two of the three biggest risks to the rally, as noted in the above ‘bullish’ section:

- Those stocks are now in a rising interest rate environment. In June 2012 benchmark 10 year treasury note yields were about 1.467, today they’re over 2.7% and in a firm uptrend, as shown in the chart below.

TWO YEAR CHART OF 10 YEAR TREASURY NOTE YIELDS

Source: Yahoo Finance

02 nov 24 1010

- They’re 18 months closer to the eventual start of a QE wind-down, however gradual that ultimately may be (we suspect it will be minimal over the coming year, barring unexpectedly good data on jobs and growth, or a sudden highly unlikely surge of inflation given the current jobs and spending trends).

- The EU remains a genuine contagion threat, currently dormant but not materially closer to a solution. As we discussed previously here, the coming ECB bank stress tests risk a new round of EU anxiety that could be the catalyst for a selloff. Japan and the US are also failing to deal with their debt issues, though neither face such potentially near term solvency risks as Europe.

- Earnings growth expectations have been falling:

(via businessinsider.com here)

05 nov 151413

- Q3 Revenues, Sales Estimates Struggling To Beat Expectations: Per FactSet: “In terms of revenues, 52% of companies have reported actual sales above estimated sales and 48% have reported actual sales below estimated sales. The percentage of companies beating sales estimates is above the percentage recorded over the last four quarters (48%), but below the average over the previous four years (59%).”

- Earnings growth, far from outstanding, has been aided by record high profit margins (9.5% vs. their 10 year average of 8.4%). Not only do these tend to revert back to their average, as shown in the above paragraph, they’re not supported by robust gains in sales revenues, but rather by cost cutting and other non-operations financial methods.

- The seemingly strong Q3 GDP 2.8% (vs. 2.0% expected) growth figure looks weak on closer inspection. The extra 0.8% was attributed to increases in inventory. The debate has been whether that increase was due to buildup from slack demand or anticipation of brisk future sales. We suspect it’s the former, and that the contribution to GDP from inventory may well reverse in Q4. Consumer spending (about 70% of GDP) was up by only 1.5%, its slowest rise in 3 years, and business spending on equipment was lower for only the second time since the start of the recovery. Retailor also reported slow back-to-school and Halloween sales. That suggests the inventory build was from slack demand resulting in unsold goods that mean less demand in Q4.

- There remains risk of yet another federal budget and debt ceiling fight. Thus far damage from the last one was minimal. If there is another one, we may not be so lucky.

Risk That Central Bank Stimulus Can’t Continue Propping Up Global Risk Assets

Fears of stocks being overvalued relative to normal economic growth and earnings metrics have been around for the entire rally in global equities that began in 2009. The ongoing key counter-argument remains the same: as long stimulus continues to keep yields down, leaving all that newly printed yield seeking cash few alternatives, risk asset prices can hold on and go higher.

Eric Parnell of Gerring Wealth Management argued recently that despite the new highs in many major indexes, an increasing number of risk asset classes and stock sectors are no longer rising with continued QE, including:

- Big-cap companies like Ford Motor (F), Apple (AAPL) and ExxonMobil (XOM)

- Income generating areas of the market such as real estate (VNQ), high yield bonds (HYG), preferred stocks (PFF) and AT&T (T), mortgage REITS like Annaly Capital (NLY)

- The industrial metals and precious metals sector, such as Freeport McMoRan (FCX) and BHP Billiton (BHP), while other major base metals such as aluminum (JJU) and nickel (JJN) have done even worse.

Obviously there are other forces at work here. Interest rate sensitive instruments are seen as at risk from a coming QE taper, and industrial commodities move mostly with Chinese demand. The point is, QE’s ability to prop up stock prices cannot be assumed to continue.

See here for the full article.

Nor is Parnell a lone voice.

London-based director of the McKinsey Global Institute, Richard Dobbs, recently issued a research report that challenges the assumptions that QE is behind the current leg of the rally, and that stimulus-suppressed low rates are forcing yield seeking income investors into stocks.

Other Stock Market Crash Indicators

Dangerously high bullish sentiment indicators including:

The Yale Crash Confidence Index (measures confidence that stocks won’t crash) at its highest since 2007

Citibank’s Panic/Euphoria model indicates extreme complacency

Record high margin debt during this rally means investors are increasingly using borrowed funds, so any sudden pullback could become self-feeding if it causes enough margin call-driven selling.

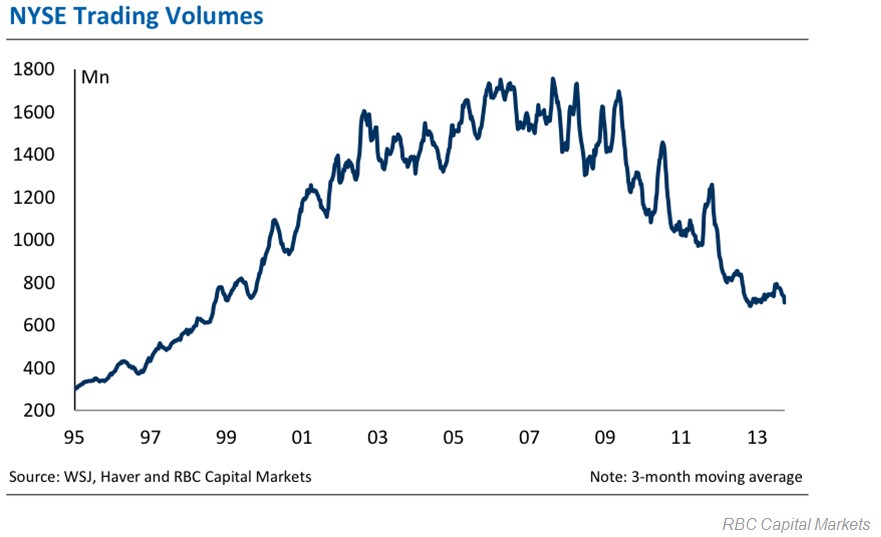

Trading volumes continue to trend lower throughout the rally that began in 2009, and those volumes continue to fall in 2012-3, suggesting a lack belief in the rally, and thus of new buyers to fuel further gains, despite the recent record highs.

(via businessinsider.com here)

06 nov 151425

Tail Risks From The US, EU, Japan, China, and Emerging Markets

If the below risks in fact happen, they will more likely hit at some point in 2014 than before the year end. Still, we decided to include mention of them here, given that there is a risk that they do influence year-end market activity. That risk rises if before the year’s end the QE taper starts or the EU’s bank stabilization plan isn’t finalized.

Each of these is large topic unto itself, but given the US market focus of this article, we’ll just briefly summarize the risks posed from each to US as well as global financial markets

US

The US debt ceiling and budget fight round III kicks off in early 2014. Most don’t expect another battle, but few would say it isn’t possible. Certainly there’s been no shortage of acrimony in Washington in recent weeks, with Republicans threatening to block Obama appointments and democrats bringing in rule changes to prevent that. This is hardly the atmosphere for optimism about a quick agreement.

Three big policy challenges converge on Washington in early 2014: the budget, Obamacare, and the debt ceiling. The government’s spending authority expires in the middle of the month, only three weeks before the US hits the debt ceiling. There is also likely to be continued trouble with the implementation of ObamaCare. Suffice to say they could provoke some volatility. Given that markets are forward looking, and also sitting on significant profits, risks of trouble in January, don’t be shocked if these challenges tempt some profit taking along with end of year tax loss selling.

EU

We’ve written repeatedly about how the EU sovereign debt and banking crisis has been merely deferred, not solved. Indeed, since it calmed markets in 2012 with a combination of the LTRO and OMT programs, the EU has made minimal progress towards the reforms needed to make it a viable currency union, primarily:

- Centralized EU supervision of banking and budgets, needed to prevent another debt crisis, and convince lenders it’s therefore safe to lend to EU businesses and institutions.

- A mechanism to transfer wealth to poorer areas

They haven’t made progress because #1 requires that member states give up a substantial degree of sovereignty, and #2 requires the wealthier states to give up cash and the debtor states to accept politically unpopular conditions. All of these issues can cost politicians their jobs.

Meanwhile, as we discussed in some detail last week here, the EU may not be able to defer decisions on these issues much longer. The coming ECB bank stress tests can’t start without first having a funding mechanism (and member states’ commitments to fund it) to pay for and estimated $50 bln in bank recapitalizations. Without this, the tests can’t proceed, because revealing bad banks without having the funding ready to stabilize them would just risk a new EU crisis as soon as the tests revealed the expected bad debts and undercapitalized banks.

However, that brings up a host of deferred issues that lie at the core of the EU crisis. See here for just how many problems the ECB bank stress tests bring to the surface, and why the usual solutions (kick the can down the road yet again, buy time by lending printed money) may not work much longer.

There are other threats to the EU. They include:

Weak Economies: A continued stagnation in most economies outside of Germany that has gotten bad enough for the ECB to begin considering a new round of easing measures, against the outraged opposition of Germany and other key funding nations that the EU cannot afford to lose. These include some form of a US-style sovereign bond purchase program, new LTRO programs, negative ECB deposit rates to force banks to lend more, etc.

More Sovereign Bailouts: The FT reported last week that Portugal may need another bailout . “Many officials in Lisbon and Brussels believe Portugal is almost certain to avail itself of the backstop Dublin shunned when its bailout ends next June: a short-term line of credit from the eurozone’s €500bn rescue fund. But several senior officials directly involved in overseeing Portugal’s €78bn bailout fear a so-called ‘precautionary programme’ may not be enough.” Nor is Portugal the only possible new bailout candidate. Slovenia remains at risk of needing aid as well.

QE Taper Could Send GIIPS And Other EU Bond Rates Higher: If US bond rates continue rising as the QE taper nears and ultimately hits, that ultimately means higher interest rates and/or lower demand for their debt and thus rising interest rates and asset prices, including those of bonds, stocks etc. That’s because higher US debt yields drain demand for their sovereign and commercial debt, as the gap between their higher bond rates and that of the less risky US shrinks. That means their bond prices must fall (and thus their yields must rise) to compensate for the additional risk of emerging market bonds compared to those of the US. Those higher rates then hit stocks as higher rates are an additional cost of business.

In other words, rising US rates would risk un-doing much of the ECB’s stimulus efforts.

Emerging Markets: If Taper Brings Continued Rising US Interest Rates

The big risk for emerging market nations as a group is that if US bond rates continue higher as the taper approaches, then hits, they face the same problem as detailed in the above final paragraph on the EU.

Indeed, the knock-on effects of rising US rates causing rising rates everywhere is a problem for everyone.

Japan

The big risk with Japan is that it becomes clear Abenomics isn’t working. Japan doesn’t have a Plan B because Abenomics IS Japan’s plan B. After that, it’s either back to austerity and likely recession, or defaults. Either way things likely get really ugly, for everyone, because a crisis in Japan (the world’s third largest economy) is unlikely to stay in Japan. For perspective, consider that if Greece can be a contagion risk, then all the more so for Japan.

China

China’s government continues to walk a very thin line between too much and too little liquidity. It needs to keep rates low enough to maintain growth, yet at the same time keep inflation in check.

Much of China’s GDP comes from funneling easy into infrastructure projects (a record 49% of China’s GDP is in investment), but it comes at a cost of higher inflation. Although China reports an inflation rate of about 3%, the increase in strikes and worker unrest suggests it’s much worse. See here for details.

Indeed, the fact that the PBOC has been draining liquidity from markets to combat inflation, particularly surging housing prices, indicates that the inflation threat is big enough for China to accept slower growth. Euphoria reflected in markets over reforms announced at China’s third plenum in Mid-November have been overdone, given that these will take years to implement.

Meanwhile, PBOC tightening presents a risk of a China slowdown that could be a drag on global growth. Falling Chinese exports would be a big deal for everyone. They’re America’s third largest export customer, and tend to be a top-3 export customer for many of the world’s largest economies.

Click here to view Part 4, where we summarize and offer concluding thoughts on the things you must watch in the coming weeks, and the big questions you need to answer in the weeks and months ahead. If you only read one other section, that’s the one.

To view other parts click on the following links: PART 1, PART 2, PART 3, PART 4. If your pressed for time, PART 1 and PART 4 are what you need to see now. They provide the overview, summary and conclusions. Then you’ll know if you need to read the rest. PART 2 provides details on what’s needed to keep markets trending higher, and PART 3 reveals what will send markets plunging.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.