The Coming Week: The State of The Bull Market & What Could Kill It

How bullish and bearish forces align for stock indexes, forex and other global markets , both technical and fundamental outlooks, likely top market movers

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we cover the lessons and market drivers that apply to most global asset markets in the coming week.

Summary

- Technical Outlook: Long, medium, and short term

- Fundamental Drivers: What’s key, what changed, what hasn’t

- One Big Bearish Concern

- What To Watch In This Week’s Calendar, Earnings

- Conclusions, And What Would Change Them

TECHNICAL OUTLOOK: Long & Medium Term Bullish, Short Term Neutral

First we look at overall risk appetite as portrayed by our sample of global indexes.

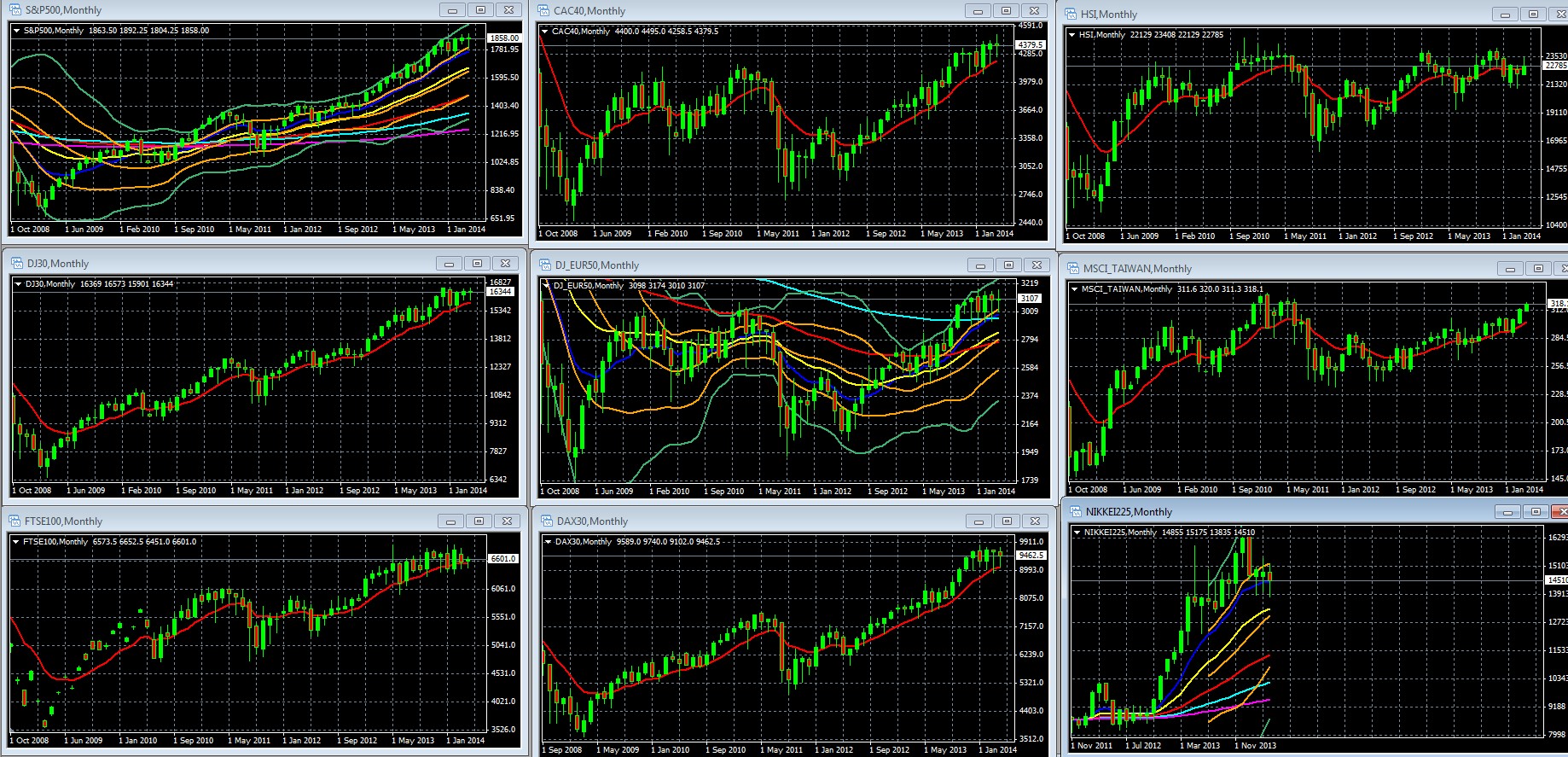

Monthly Charts Of Leading Global Stock Indexes: Upward Momentum Still Strong

Monthly Charts Of Large Cap Global Indexes With 10 Month/200 Day EMA [DATES] In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

Key For S&P 500, DJ EUR 50, Nikkei 225 Monthly Chart: 10 Week EMA Dark Blue, 20 Month EMA Yellow, 50 Month EMA Red, 100 Month EMA Light Blue, 200 Month EMA Violet, DOUBLE BOLLINGER® BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

02 Apr. 20 02.00

Index Monthly Charts Key Points: Support Holds, Uptrends & Momentum Intact – However…

The monthly charts of our sample global indexes show upward momentum remains strong:

–Most indexes (particularly our US and European indexes) remain firmly in their double Bollinger® Band Buy Zone, suggesting the odds favor enough continued upside strength to justify new long positions.

–Most EMAs continue to slope higher, with shorter term EMAs rising faster, indicating accelerating uptrends.

The one caveat is that among the US and European indexes we’re seeing a growing string of ‘doji’ shaped candles (small body, long tail) that indicate indecision. When these occur at the top of a long uptrend, as most here do, that’s a bearish indicator that investors are losing enthusiasm and that a selloff is more likely.

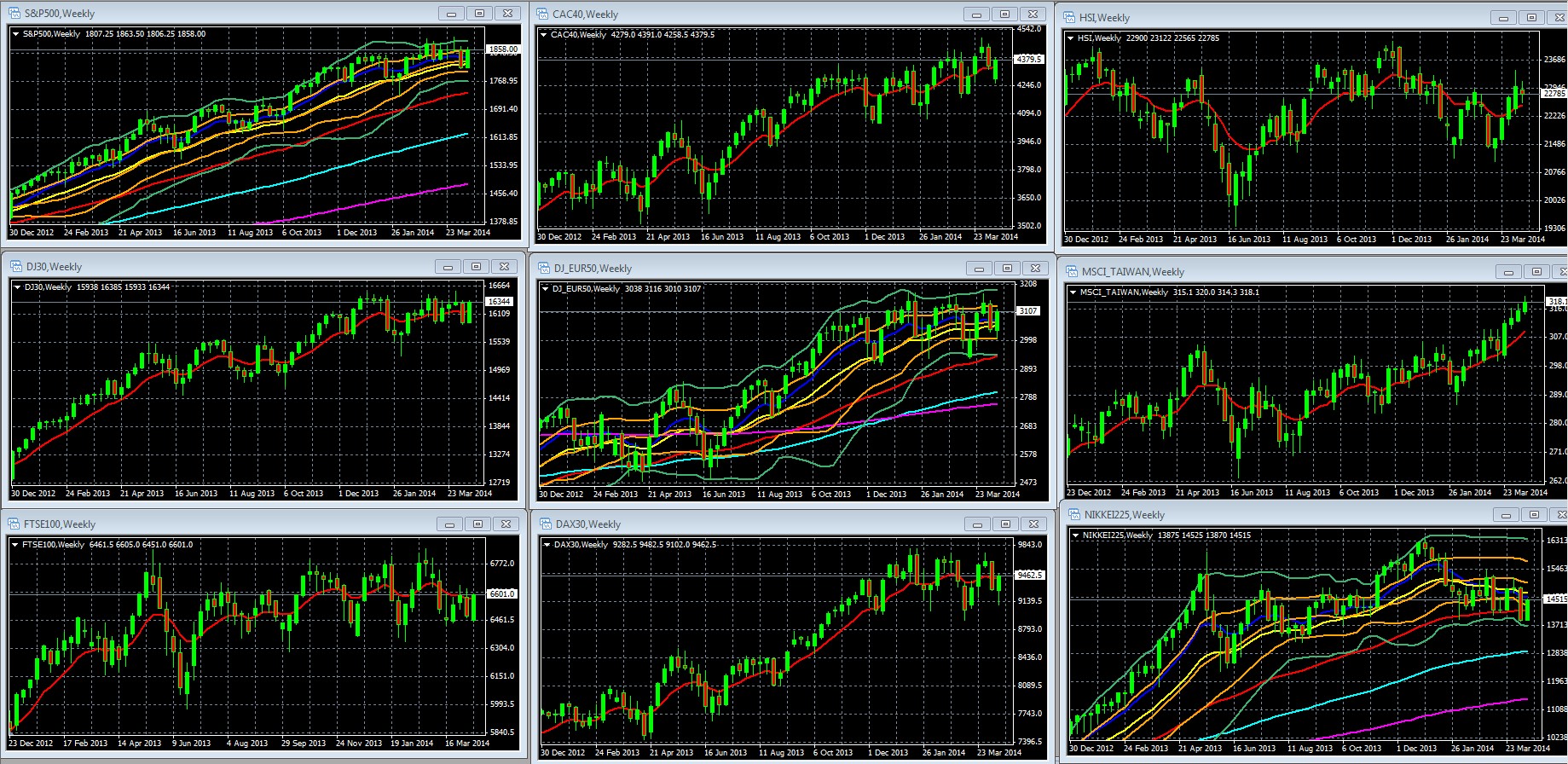

Weekly Charts Of Leading Global Stock Indexes: Risk Trends Growing But Slowing

Most indexes recouped most or all of the prior week’s losses. In other words, support held. As we predicted last week, so far we’ve just a minor normal bull market pullback in risk appetite.

Weekly Charts Of Large Cap Global Indexes With 10 Week/200 Day EMA [DATES] In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

Key For S&P 500, DJ EUR 50, Nikkei 225 Weekly Chart: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER® BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

16 Apr. 18 18.33

Index Weekly Charts Key Points: Support Holds, Uptrends Intact But Losing Momentum: Still Bullish

Overall the medium term uptrends are intact (Hong Kong and Japan the obvious exceptions).

That said, the momentum indicators on the weekly charts continue to weaken, as most of our sample leading global stock indexes have been flat since early December.

–They’ve closed in their double Bollinger band neutral zone, implying no strong trend up or down, range trading ahead.

–The EMAs are flattening.

Conclusion: Risk appetite over the medium term is still drifting higher. That’s still bullish for the EURUSD, which tends to rise or fall with risk appetite. However the weakening momentum means that risk appetite could soon cease to support the pair.

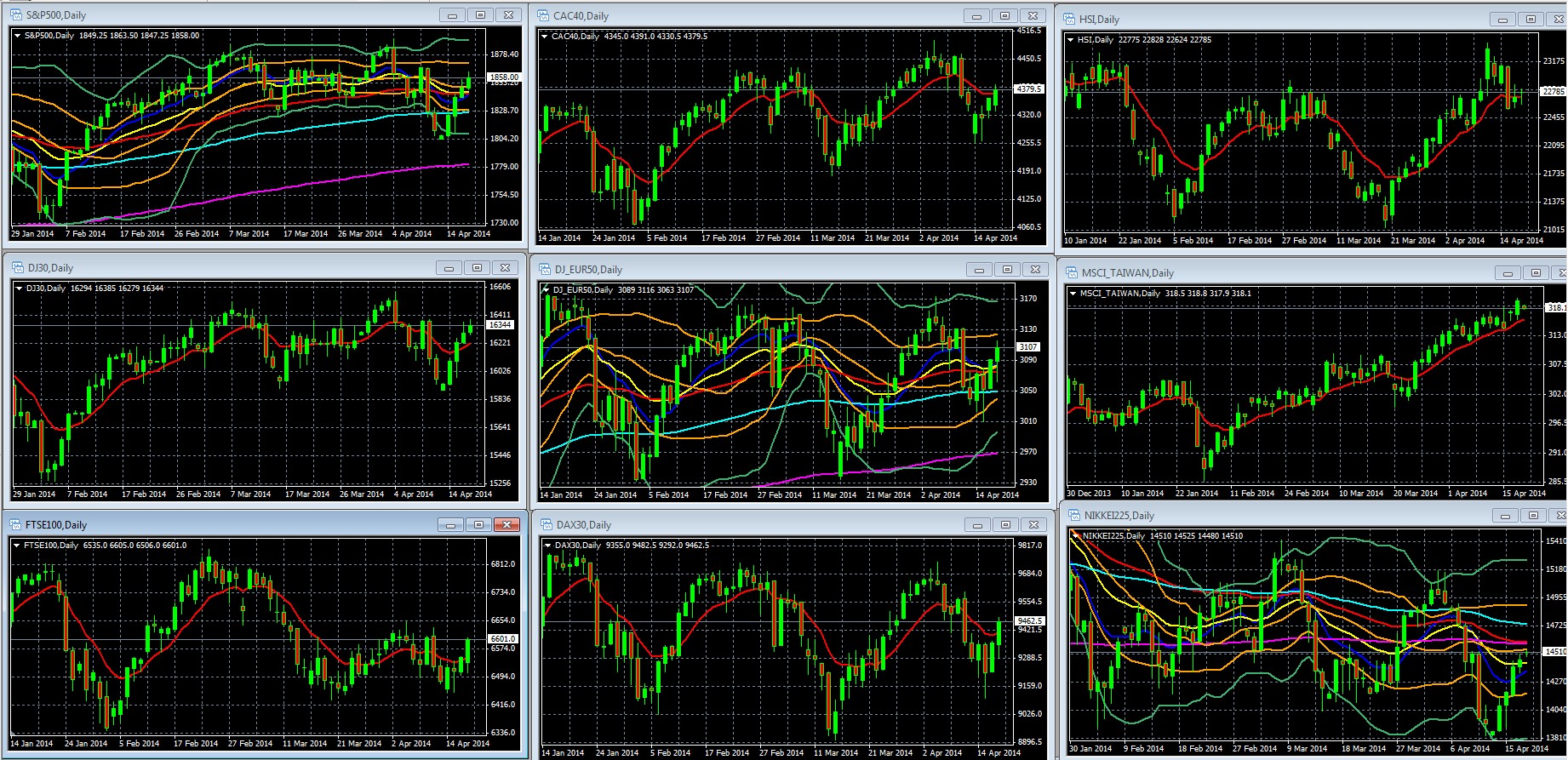

Index Daily Charts Key Points: Support Holds, Downtrends Forming, Momentum Neutral

Daily Charts Of Large Cap Global Indexes With 10 Day EMA In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

Key For S&P 500, DJ EUR 50, Nikkei 225 Daily Chart: 10 Day EMA Dark Blue, 20 Day EMA Yellow, 50 Day EMA Red, 100 Day EMA Light Blue, 200 Day EMA Violet, DOUBLE BOLLINGER® BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

04 Apr. 20 02.21

Key Points

- On a daily basis, momentum is now flat, in neutral mode

- the indexes are in their double Bollinger® band neutral zones,

- Note that since mid-January most indexes have gyrated in clear trading ranges, and most are building downtrends over the past weeks.

FUNDAMENTAL OUTLOOK

What are the fundamental drivers behind the recent weakness in the daily charts?

The short version: there’s no obvious explanation.

Central Bank Policy Unchanged

Loose central bank policy, the biggest single driver of asset prices in recent years remains extremely accommodative for the foreseeable future. Fed and PBOC tightening moves have been very slow and cautious. Fed stimulus continues for the rest of 2014, the taper is merely slowing it.

More importantly, the Fed has succeeded thus far in convincing markets that it can keep rates low.

Via Business Insider/Matthew Boesler

11 Apr. 18 15.21

The ECB is getting ready to ease more. See here for details on why ECB easing is just a matter of time – probably coming this summer at latest unless there’s unanticipated strength in EU growth, or weakness in the EUR.

Japan is also set to do more, saving its next bullets to counter the effects of the new sales tax on spending.

Data No Worse

Economic data has overall been better than in recent months. The struggles of China and Japan are old news that didn’t stop the rally before.

The EU still stinks but is if anything steady to improving, with funds continuing to flow into GIIPS bonds and stocks despite the lack of reforms to prevent another EU crisis.

The US continues to recover and early signs of improvement in recent jobs and spending data suggest that earlier weakness was indeed mostly from the temporary effects of bad weather.

In fact, considering recent upbeat jobs and spending data, the US recovery is if anything looking a bit better.

Valuations: Stocks Look Expensive

This debate is also old news and remains unresolved. Shiller’s CAPE and Tobin q do suggest stocks are expensive, but that’s been the case for some time too.

Remaining Excuses?

We appear to be left with the following:

Uncertainty Ahead Of Earnings Season

So far earnings season has been ok. Per a recent Reuters article

With less than one-fifth of S&P 500 companies having reported results so far, about 63 percent have topped earnings expectations, according to Thomson Reuters data, exceeding the 56 percent average over the past four quarters. About 52 percent have beaten revenue forecasts, about even with the 54 percent average over the past four quarters.

This may explain the past week’s bounce off of support.

Fears of Economic Damage From Exchanges Of Russia Sanctions

So far market reactions to Ukraine have been short lived, and there’s little evidence that Europe or the US is prepared to bear the economic costs of a serious sanctions and potential counter-sanctions from Russia.

So far there’s nothing to suggest that this crisis should bring the long-anticipated selloff.

For details on this view, see our coming post Fools Russian: 1 Chart Shows Why Russia Tension-Related Selloffs A Buying Opportunity.

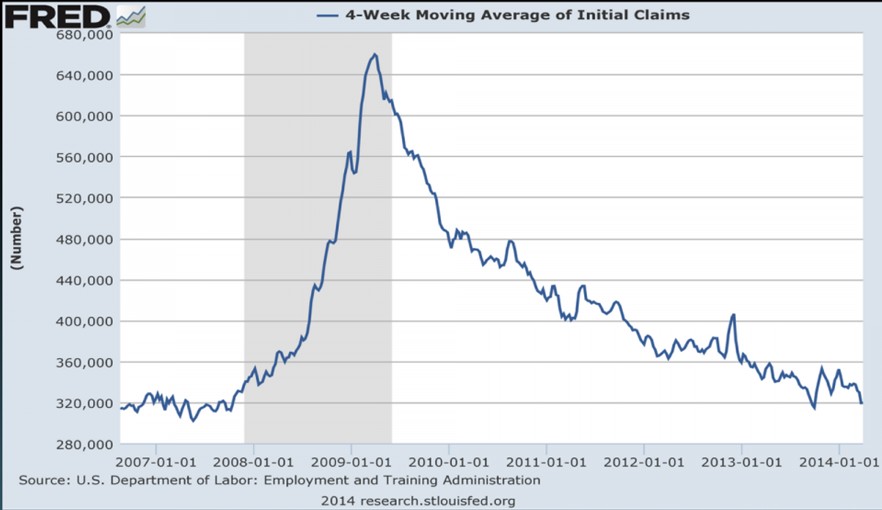

One Big Bearish Point Of Concern

I know the US recovery is continuing, but for a country where ~70% of GDP is consumer spending, this simple comparison below is troubling.

Per the below chart, about 320k jobs are being lost each month.

12 Apr. 18 16.25

Per the following chart, the US has been adding well under 200k jobs per month.

Source: forexfactory.com

05 Apr. 20 04.10

So even if we assume that the jobs gained pay as well as the jobs lost (?), the US continues to lose jobs while the working age population grows.

How sustainable is this recovery? Am I missing something?

Top Calendar Events To Watch

Summary: Will We Get Answers To The Biggest Questions On Everyone’s Mind?

These are, of course:

- Is long bull market in global stocks and other risk assets likely to endure for the coming months or longer/ the timing and extent of the next big pullback or normal correction that gives us a new chance to enter new long EURUSD or other risk asset positions? A variation on this same question is the ongoing debate on stock valuations (less productive given that valuation and sentiment metrics offer little help for timing market moves).

- More fundamentally, are the two most likely causes of the above, ECB or Fed policy changes, coming sooner or later than currently believed?

The best evidence for influencing sentiment on both of the above will be whether or not the below reports mostly surprise to the upside or downside. Mixed results don’t change market sentiment

Highlights

EU: April’s preliminary set of EZ PMIs are expected to show further slowing in manufacturing and service sector activity growth. That may feed speculation about an earlier and/or larger ECB stimulus package.

US: Home Sales, Durable Goods Orders and Consumer Confidence figures are in the spotlight. US economic showed a notable improvement relative to expectations over the past two weeks (according to data compiled by Citigroup). If that trend continues, ebbing doubt about the continued withdrawal of Fed stimulus may offer yield-based support for the US Dollar. Continued solid data should go a long way to restoring confidence in the US recovery because it would confirm that winter weakness was indeed a temporary aberration from the harsh weather.

Here’s The Daily Breakdown

Monday: Europe, Hong Kong closed, US open

Tuesday: US existing home sales

Wednesday

China: HSBC flash Mfg PMIs: The health of the Chinese economy has a dual importance for the EUR, as discussed above. The HSBC report emphasizes the private, mid-size and small firms as opposed to the official version that focuses on big state owned firms. These smaller firms are more likely to suffer from tight credit conditions, so a bad read would suggest higher odds of new China stimulus

EU: Flash French, German, EU services and Mfg PMIs – offer the latest check of EU economic health and thus will update sentiment on the likelihood of ECB easing sooner rather than the currently expected June meeting.

US: Flash Mfg PMIs, new home sales. As we’ll discuss in our post on the coming week, there are ominous signs for a slowdown in US housing data, a key coincident and leading indicator of consumer spending.

Thursday

EU: German Ifo sentiment survey, Draghi speech

US: Durable goods, weekly new jobless claims

Friday: nothing that important.

Earnings

So far these have helped lift stocks (but only to the upper end of recent trading ranges) as they’ve been overall positive, albeit after the usual downside revisions making it easier to exceed expectations. The coming third week of earnings season is usually the last one that has any potential to drive markets. After this, the picture tends to be set.

The big names this week include leaders from virtually all sectors of the US and global economy, including:

- Monday: Haliburton (HAL), Netflix (NFLX)

- Tuesday: AT&T (T), McDonalds (MCD), Yum! Brands Inc (YUM), VMware Inc. (VMW)

- Wednesday: Apple (AAPL), Delta Airlines (DAL), Boeing (BA), Dow Chemical (DOW), Facebook (FB), General Dynamics (GD), Northrop Grumman (NOP), Proctor and Gamble (PG), TD Ameritrade (AMTD), Zynga (ZNGA)

- Thursday: 3M Co. (MMM), Altria (MO), Amazon (AMZN), Baidu (BIDU), American Airlines (AAL), Eli Lilly (LLY), General Motors (GM), KLA-Tencor (CLAC), Lorillard (LO), Microsoft (MSFT), United Airlines (UAL), Verizon (VZ), Visa Inc. (V), Waste Management (WM)

- Friday: AON Plc (AON), Ford Motor Corp. (F), Moody’s Corp. (MCO), Weyerhauser, (WY)

Yum Brands, (YUM), Qualcomm (QCOM), Caterpillar (CAT)and Apple (AAPL) all have heavy China exposure and so should provide some insight into China’s health.

CONCLUSIONS

As we concluded here last week, there was no compelling evidence that the selloff was anything more than a normal temporary pullback. The past week’s bounce in most global indexes suggests that most felt likewise.

I’m not saying stocks couldn’t sell off, they could. I just don’t see any new reason why that would happen now. There’s no compelling reason for a new leg higher, but there also isn’t a reason for a selloff either. Sure, with stocks so high any number of factors could spark a normal 10%-15% pullback. But beyond that? What?

With so many global stock markets at decade or all-time highs despite tepid growth prospects, these rallies have been fueled by little more than central banks’ financial repression/accommodative policy.

These conditions remain, therefore so too should the current trading range for equities and other risk assets.

What would it take to for stocks to break out, up or down?

- A major central bank policy shift to tightening and higher rates. Not happening

- A sudden consensus that stocks are too expensive AND the rise of an alternative place to park cash.

- A new, sustained risk-off event like a new systemic risk from the EU or China. For more on the state of the EU and how it may affect other markets, see here and here.

Meanwhile, expect more range trading.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.