Coming Week Lessons Part 2: The Common Driver Of EU, Japan, China, EM Developments

Lessons for the coming market week from the US for traders and investors in stocks, indexes, forex and other global markets, plus idea on profiting from EM crisis

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we cover the key lessons learned for the coming week and beyond.

EU

More Signs of Tight Liquidity

No One Buying ECB’s Sovereign Bond Inventory

For the second time this year, last week the ECB failed to sterilize a sovereign bond purchase. It holds over €170 Billion in government bonds it holds from its rescue efforts over the past few years.

That is the second time in January, and the fifth time in the past two months that the ECB was unable to find buyers for that growing inventory of sovereign bonds – another in a series of nagging concerns that liquidity troubles are bubbling to the surface once again. As we discussed in greater detail here, this means banks would rather hold cash and earn essentially nothing than hold those higher yielding EU sovereign bonds.

In other words, EU banks are both hording cash and don’t believe the yield offered on these bonds is adequate compensation for the risk of default. Note that for the purposes of bank stress tests those bonds are considered risk free. It’s a European version of the US no longer requiring mark-to-market for bank assets. When reality doesn’t work, they just shift to fantasy.

Bank Troubles Lurking

A study by the OECD suggesting EZ banks face a total capital shortfall of €84 billion. Supposedly there will be serious bank stress tests this year, and as we’ve noted repeatedly, the new single resolution mechanism provides leaves member nations and bank depositors, lenders, and shareholders on their own if a bank is insolvent.

Also…

Also, while the overnight market rate (EONIA) was reduced 50% from the prior week, but remains elevated. Meanwhile, economic data for the Eurozone remains weak, standoffs with Greece continue and bailed EZ members are casting off support lines.

The Lessons

Liquidity problems persist

The ECB is buying bonds it can’t resell to banks, which means it is buying bonds with newly created cash, aka debt monetization. No huge thing for now, given that inflation is not a threat.

We still can’t figure out how the EU is going to clean up its banks and where it will get the funds to do so.

As we discussed in depth here, it’s a matter of time before the ECB has no choice but to simply print money and hope the EUR doesn’t collapse. Abenomics, Draghinomics, etc.

JAPAN TRADE DEFICIT & YEN COLLAPSE DANGER: ANOTHER DEFLATION RAMIFICATION

On Monday we learned that the Japanese trade deficit nearly doubled to hit record high of ¥11.5T ($113B) in 2013, due to a combination of two longer term trends, a falling yen (due to Abenomics policy being used to fight deflation) and rising energy imports after a shutdown of the nuclear industry after the 2011 Fukushima meltdown. Until then, Japan had always had trade surpluses for three decades.

Monday’s news was a reminder that Japan’s trade deficit and the challenges of preventing a collapse in the JPY’s value haven’t gone away.

Japan’s trade surplus was a key support for the Yen despite Japan’s over 200% debt/GDP ratio. Rising energy costs could exacerbate that trade deficit, and risks of a Yen collapse, if they get high enough to discourage domestic industrial production and exports. Why build a factory in Japan when you can service the American market and its neighbors with US plants that have lower energy costs and no overseas shipping expense?

CHINA DEBT SENTENCE ANNULED

Last Monday China avoided a default with enough systemic risk to become a “Chinese Lehman moment.”

As we wrote last week in Contagion Risk Chinese Style: The Week’s Real Main Event, one of its largest financial institutions was due to default on nearly a half-billion dollar wealth management product (WMP) debt instrument on January 31st and cast doubt on an asset class with a total value of about 60% of China’s GDP.

China has found a solution to this and numerous other lurking default risks – it simply orders creditors to rollover the debt. At least in the EU they pretend creditors ‘voluntarily’ accept losses. See here for details.

Lesson: the big question is whether this imposition of losses on lenders won’t have the same effect it had in the EU after the second Greek crisis was similarly resolved with unofficial defaults – tighten credit conditions as private lenders flee and leave the government provide needed liquidity?

As we note above, that approach is failing in the EU as the ECB has had 5 failed attempts to sell part of its huge inventory of bonds to investors, leaving the ECB’s new bond purchases unsterilized and thus they’re a straight debt monetization, with all the risks that entails.

China has an advantage that should allow it to play that game longer – it can simply continue to order local governments or banks to buy unwanted debt.

See here and here for background, and here for additional developments late last week.

Emerging Market (EM) Selloff Key Lessons

Here’s a rundown of the key lessons of the EM asset selloff, as well as few ideas on how to profit.

The Selloff Is In Its Early Stages

The first lesson to understand is that the fundamental forces driving the EM asset selloff are likely to persist over the coming year, so the selloff is likely just starting, though of course like any trend, it will fluctuate with short term news and technical overbought/undersold conditions. That means the EM selloff has opportunities for patient, long term investors.

Background

In fact began in May 2013 with the Taper Tantrum and has continued ever since.

(via businessinsider.com here)

01 feb 03 15 59

As highlighted in the chart above, recent weeks saw the trend accelerate due to a convergence of factors. These include:

- The slow but steady tightening from the Fed, and also the PBOC, which run policy for the EMs two biggest customers. That means rising rates that undermine the prime driver for the EM asset rally, EM assets relatively higher yield.

- Local political and labor unrest that has further exacerbated the risk premium and thus yield shock in these nations.

- The China slowdown and particularly the bad news that came out Thursday January 23-4 (see here for details) was the likely catalyst for the big initial short-squeeze selloff that got the media’s attention on January 23-4.

Most of these are long term macro trends and thus the selloff and downtrend in many EM risk assets is likely to be a long term affair. The whole EM rally was based on a search for higher returns, as these areas were expected to grow faster than the developed world. Now that the above and other factors are reversing that yield differential and/or raising the risk for the coming year or more, the EM outflows should continue.

Here’s another, longer term look at how fund inflows from the US began reversing out once the first hints of the coming fed QE taper came out in May 2013.

Source: FT.com Here

01 JAN 31 0923

How To Profit: The General Principles

First, kudos to FT.com’s John Authers for pointing this particular idea, which I’ll summarize and at times expand upon, and also add some possible specific suggestions.

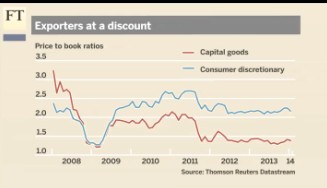

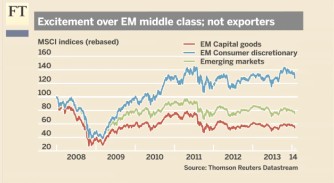

In the charts below, Authers uses the MSCI capital goods indexes as rough but still useful proxy for EM exporters, and the MSCI EM consumer discretionary index to represent that sector.

In the pre-Great Financial Crisis (GFC) years, before Fed policy drove yields down and helped fuel the search for yield and fund flows into EM markets and currencies, EM capital goods companies sold at a strong premium relative to consumer discretionary stocks. Their cheap currency and low labor costs made them competitive and beneficiaries of strong developed world currencies, and thus more attractive compared to those trying to sell consumer discretionary goods to struggling EM consumers.

Note how in the chart below, the EM capital goods exporters had higher valuations relative to EM consumer discretionary stocks, and how that suddenly changed with the start of the GFC.

Source: FT.com Here

08 JAN 31 1013 02 feb 03 1707

As shown in the charts above and below, in the years of the rally in EM market stocks and currencies, consumer discretionary stocks were bid up as likely beneficiaries of the growing EM middle class. In contrast, EM capital good exporter stocks did not rally nearly as much, as they were burdened by a rising currency and rising labor costs.

Source: FT.com Here

07 JAN 31 1001 03 feb 03 1710

Most of the differences in valuations between the over bid (and still expensive) consumer discretionary EM stocks and the far cheaper EM capital goods stocks were due to this sentiment, although there could be some contribution from actual performance differences.

The key lesson is that EM consumer discretionary firms are still selling at a much higher premium. As the developed world continues its recovery, and rates rise, that recovery should bring a reversion back to higher valuations for the EM capital goods exporter companies.

The logic here is that the EM exporters benefit from the cheaper EM currencies more than they are hurt by rising local interest rates and inflation, at least compared to the EM consumer discretionary goods sellers, whose customer base of new middle class could shrink and have less disposable income.

That’s the basic principle to guide our search for undervalued EM stocks: long the better EM exporters, short the weaker EM consumer discretionary stocks.

I’ll leave specific recommendations for a separate post, though recent news of China continuing bid up prices on high-quality iron ore has led JP Morgan to recommend Vale (VALE). That should also generate interest in other leading high-grade iron ore suppliers like BHP Billiton (BHP) and Rio Tinto (RIO).

Conclusions

Note how all of the above developments are tied to liquidity and deflation issues.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.