Global Markets Weekly Quick Wrap: Daily Recap, Market Drivers, & The 1 Big Question

A summary of global stock market price action & what caused it in Asia, Europe and the US- to help investors and traders of forex, stocks, indexes etc. Get back into context for the week ahead in global financial markets

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we share thoughts about what’s driving major global asset markets. The focus is on global stock indexes as these are the best barometer of overall risk appetite and what drives it, and thus of what’s moving forex, commodities, and bond markets.

It’s a quick summary of last week’s international stock market action and what drove it. It’s our starting point for our follow up articles on:

- Lessons For The Coming Week And Beyond

- Coming Week Top Market Movers

- EURUSD Outlook

- Related Special Features: These vary each week depending on what’s happening. You’ll find them here.

OVERVIEW

Note that most leading indexes inched higher this week, continuing their recovery from the recent EM-scare pullback.

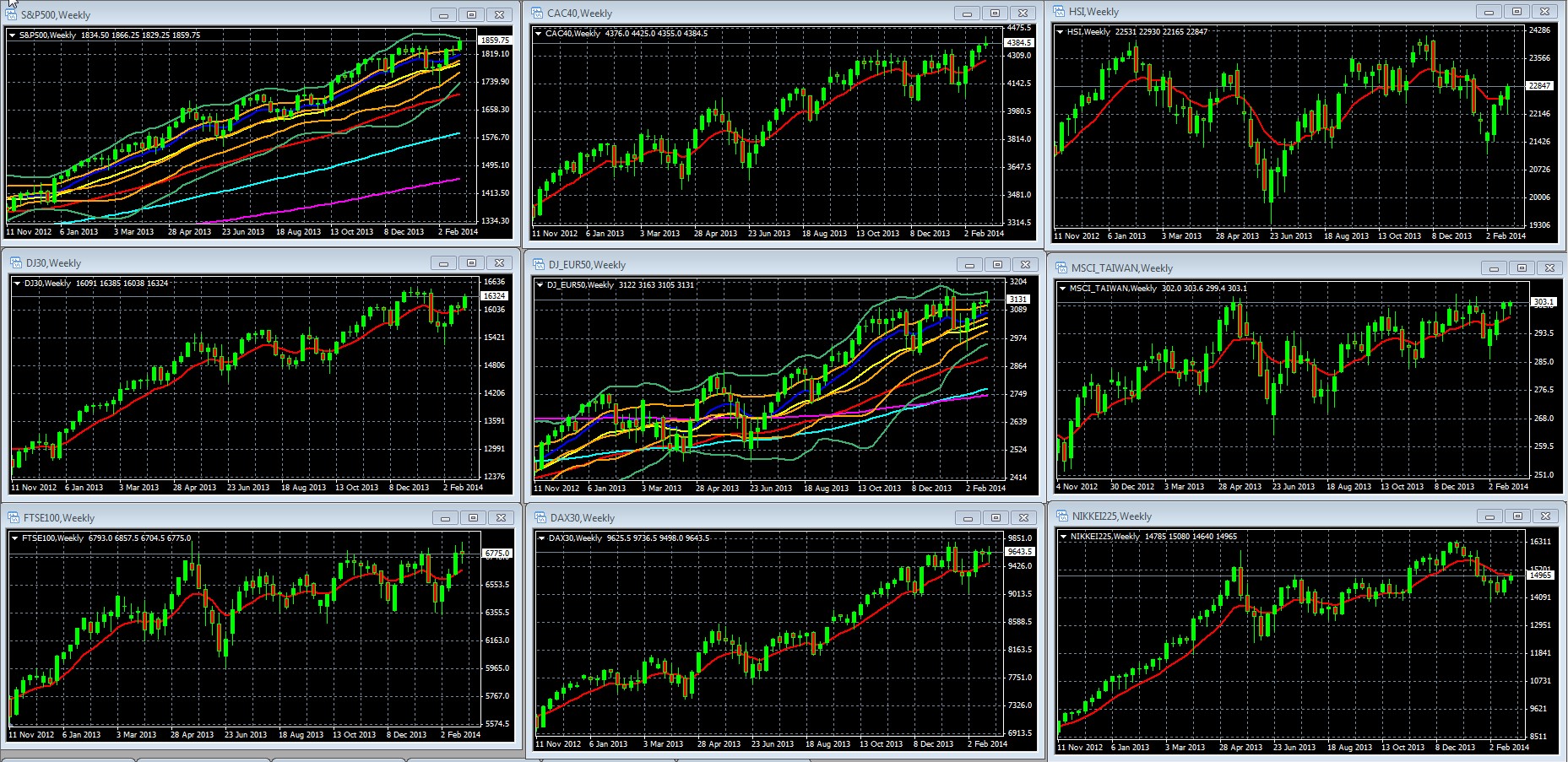

Weekly Charts Of Large Cap Global Indexes With 10 Week/200 Day EMA In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

FOR S&P 500 AND DJ EUR 50 Weekly Chart October 2012 – Present: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

01 Mar. 01 20.34

The near term direction of global stocks remains a battle between entrenched upward momentum fueled by hopes of continued recovery and low rates that keep driving yield seekers into equities, and bearish vulnerability to profit taking on bad news that threatens the slow but steady recovery theme in the West, and the China soft landing theme in the East.

That said, as long as fixed income yields remain subdued, equities continue to benefit from a lack of competition for new cash from yield seekers.

The US and Europe are back to their December levels, but with a bit less momentum given their early 2014 range bound trading. Still, indexes of both regions have risen back into their double Bollinger band buy zones and so the upward momentum looks set to continue until we have evidence to the contrary.

So, what was behind the price action? Here’s a daily breakdown of it and what was driving it.

DAILY PRICE ACTION & MARKET MOVERS

MONDAY: East Down, West Up, No Particular Reason

Asian indexes closed mostly lower [Japan -0.2%, Hong Kong -0.8%, China -1.75%, India +0.53%, Australia +0.01%, Korea -0.45% Singapore +0.19%] on a light news day lacking any new market moving news.

In contrast, European indexes were overall higher [UK/FTSE +0.41%, Germany +0.54%, France +0.87%, Spain +1.24%, STOXX50 +0.53%], as the bullish factors (strong gains in Spain, a positive German Ifo reading, and continued inflows into European equities in general) outweighed the bearish ones:

- Weak earnings and outlook from HSBC and Volkswagen

- Strong nearby technical resistance noted above. For example last Friday the French CAC index hit a 5.5 year high on hopes for continued recovery.

- Rising deflation threat: On Monday Euro-zone CPI showed a 1.1% drop in January (the highest monthly decline on record) after rising 0.3% in December. This was much worse than the forecasted 0.4% decline. Although the ECB has so far been sanguine, as we wrote in our January 4th article, Coming 2014 Explosion: EU Money Supply or EU Itself?, some kind of official money printing/QE program is just a matter of time. Unofficially it has begun in small steps via periodic failures to sterilize ECB purchases of GIIPS bonds since December.

Don’t believe me? BNP Paribas bank joined me last Wednesday, saying that new stimulus measures are in the pipeline. See our post on lessons for the coming week (Europe section) here for details.

All major US indexes finished solidly higher[Dow +0.64%, S&P +0.62%, Nasdaq +0.69] and were once again near all-time highs as investors continue to ignore weakening data, blaming it on temporary weather conditions that mask greater strength.

- The Dallas Fed’s general business activity index fell to 0.3 in February from 3.8 in January.

- Markit’s Flash (or preliminary) U.S. services PMI slipped to 52.7 in February from 56.7 in January.

Both negative results were blamed on the weather, with Markit saying: “Moreover, a robust increase in new business volumes and continued job hiring suggested that underlying demand remained resilient. February data meanwhile indicated one of the fastest increases in backlogs of work since the survey began in late 2009, which added to the signs that weaker activity growth reflected temporary weather disruptions.”

Some attributed the bullishness to the resilience of the S&P 500 futures despite some weak economic data and market performance in China. In other words, another bearish catalyst was again ignored. Once the U.S. stock market started with a bullish bias, a fear of missing out on further upside helped fuel some renewed buying interest, though some might be just short covering, following Friday’s lackluster session.

TUESDAY: Monday Giveth, Tuesday Taketh Away – Minor Technical Reversals

Asian indexes closed with divergent results [Japan +1.4%, Hong Kong -0.3%, China -2%, India +0.2%, Australia -0.11, Korea +0.81%, Singapore -0.07%], although non-Chinese related indexes fared better on follow through from the prior night’s US close

Europe closed modestly lower [UK FTSE 100 -0.52%, Germany -0.10%, France -0.10%, Spain +0.51%, STOXX50 -0.09%] on another light news day. Lacking any real excuse to climb, and after yesterday’s gains, they were vulnerable to this kind of minor reversal, with materials stocks dragged lower by an accelerating depreciation of the Chinese Yuan. See our article on lessons for the coming week here for details on that.

US indexes closed only slightly lower [Dow -0.16%, S&P -0.13%, Nasdaq -0.13%] as weakness in Europe and weak consumer confidence (again blamed on bad weather) were somewhat balanced by Home Depot’s earnings beat. As with Europe, the price action seems as much as anything else a technically driven selloff reaction to stocks being at long term highs and after a prior day’s higher close near strong resistance tend to pull back unless there’s and excuse to move up.

WEDNESDAY: Caution Ahead of Yellen Testimony, US GDP

Asian indexes closed mixed, mostly higher [Japan -0.5%, Hong Kong +0.5%, China +0.35%, India +0.65%, Australia +0.05%, Korea +0.30%, Singapore -0.50%]. China shares close higher to end a four-day slide as property sector concerns ease.

European indexes pulled back again [UK/FTSE 100 -0.45%, Germany -0.39% France -0.40%, Spain -0.20%, STOXX50 -0.06%] as long term resistance levels continue to hold

The big 3 indexes [Dow +0.15%, S&P +0.01%, Nasdaq +0.10%] inched higher as resistance historical highs remains bent but not decisively broken. In particular, the S&P 500 failed to close above 1,850 for the third straight day, with light volume suggesting little conviction one way or the other as markets await a real reason to justify new buying at these elevated levels. New home sales came in much stronger than forecasts, a welcomed sign of housing sector strength. However experts remain divided about whether it is indicative of anything:

- Morgan Stanley’s Ted Wieseman cautioned that: “Any consideration of new home sales has to keep in mind that these data are badly measured, with the standard error on the monthly percent change having reached an astronomical +/- 17.9%,” he said. In other words, the Census Bureau is 90% sure the actual change was somewhere between -8.3% and +27.5%.

- Per the Mortgage Bankers Association, mortgage purchase applications fell 8.5% for the week ending Feb. 21, showing accelerating decline in applications from the 4.1% drop the week before.

The modest moves of the past two days can be at least partly attributed to caution ahead of the week’s biggest scheduled events on Thursday and Friday, as noted below.

THURSDAY: Bearish Ukraine Turmoil vs. Bullish US Data, Yellen Testimony

Asian indexes closed mixed [Japan -0.3% , Hong Kong +1.7%, China +0.3%, India +0.65%, Australia -0.48%, Korea +0.39%, Singapore +0.27%] with mostly modest up or down moves on caution ahead of the day’s big events which included:

- A big data dump from the EU, which included German inflation data. As we noted last week, Germany’s support for inflationary policy increases if Germany too sees a deflation threat.

- From the US, Yellen’s Senate testimony and durable goods.

- Friday also includes serious market movers, such as

- EU: CPI (if too low it would feed deflationary fears and make the ECB more likely to ease sooner)

- US: Chicago PMI (adds some new evidence about the effects of weather on recent US manufacturing data), preliminary US GDP for Q1 2014, monthly pending home sales, and a few FOMC members speaking.

European stocks recouped most of their early losses near the close[UK/FTSE 100 +0.16%, Germany -0.76%, France -0.01%, Spain -0.57%, STOXX50 -0.21%], as concerns over Ukraine turmoil were balanced somewhat with better-than-expected U.S. durable goods data and comments from Federal Reserve Chair Janet Yellen that were both dovish in tone and lacking in negative surprises, prompting some investors to return to the market.

US Stocks closed higher with a late push [Dow +0.43%, S&P +0.50%, Nasdaq +0.63%], and the S&P 500 finally closed above 1,850 to a record high after three days failed attempts to do so, aided by solid durable goods orders data and congressional testimony from Janet Yellen that eased uncertainty and balanced the bearish geopolitical concerns from Ukraine.

- Yellen said the Fed likely would continue tapering its asset purchases while tracking data to figure how much recent softness in the economy is due to the weather. Her admission of soft data was seen as supportive of dovish policy.

- As with much of the week, activity was influenced by short-term traders waiting to see if the S&P could hold above 1,850 before buying or selling. When the index broke through and appeared to be holding above 1850 into the close, a burst of buying to close out short position gave it an added boost. The close above 1850 increases the odds that this former resistance level becomes at least near term support, however we believe a close on Friday above that level is needed for some confirmation.

FRIDAY

Asian shares closed mixed [Japan -0.6%, Hong Kong flat, China +0.4%, India +0.6%, Australia -0.10%, Korea +0.08%, Singapore +0.45%] with little overall movement reflecting the light news and caution in light of Ukraine tensions, and major European and US data later in the day. Yen strength was an additional headwind for Japanese exporters.

European shares closed mixed [UK/FTSE100 -0.01%, Germany +1.08%, France +0.27%, Spain -0.42%, STOXX50 +0.05%] with mostly minor moves (ex-Germany which was lifted by strong gains from drug and chemicals maker Bayer and decent data this week). A slight rise in inflation data, suggesting a lower chance of new ECB stimulus any time soon, may have also pressured shares, along with the Russian invasion of Ukraine’s Crimea region.

US shares closed mixed [Dow +0.31%, S&P +0.26%, Nasdaq -0.25%] with minor up or down moves as earlier gains faded in the last two hours as Ukraine uncertainty may have provided the excuse to take profits into the weekend at the close of a strong month.

Although there were a number of important US data releases (Q4 2013 preliminary, Chicago PMI, UoM consumer confidence, none provided enough of a surprise to be market moving.

| Index | % Change | YTD % |

| DJIA | 1.4 | -1.5 |

| Nasdaq | 1.0 | 3.1 |

| S&P 500 | 1.3 | 0.6 |

| Russell 2000 | 1.6 | 1.7 |

The One Big Question: New Highs Ahead?

Given the regained momentum of most leading global indexes despite mixed data that hardly justifies all-time highs, we conclude that as long as rates remain low despite stimulus cutbacks, the uptrend in stocks and other risk assets can continue to drift higher as yield seekers have few options. Prior long term resistance hasn’t held back the uptrend since mid-2012.

That said, we’ve a typically packed beginning of the month calendar this week. That has enough top tier events to move markets if these provide a major surprise. See our post on the EURUSD weekly outlook here for a quick rundown of the major events this week.

The big pullback threat is if any of the optimistic assumptions given below are discredited.

- Thus far weakness in US data has been shrugged off as a temporary manifestation of temporary bad weather.

- Chinese weakness is not a huge concern, just part of the soft landing expected as China cuts back on the reckless lending and drains liquidity to do so.

- The EM crisis is not seen as a systemic risk to global markets

- Even though nothing has been fixed in the EU and there’s a looming banking stress test that’s supposed to reveal $50-100 bln in under-capitalizations.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.