The Biggest Market Threat Of All? Does QE Trap Means Taper Is Tightening

Analogy Test: Taper Is To Tightening, As Foreplay is To…Or, QE Taper Equals QE Trap Which Equals Tightening

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we share thoughts about key developments worth a special report – this one on ramifications of the taper and whether it really is tightening, regardless of theoretical distinctions.

Forget about the theoretical debate over whether QE is in fact tightening. The behavior of global markets since the start of the taper suggests the Fed and other central banks that seek to cut back stimulus are confronting a QE trap.

In other words, tapering may not be the same thing as tightening; it’s just having the same effects.

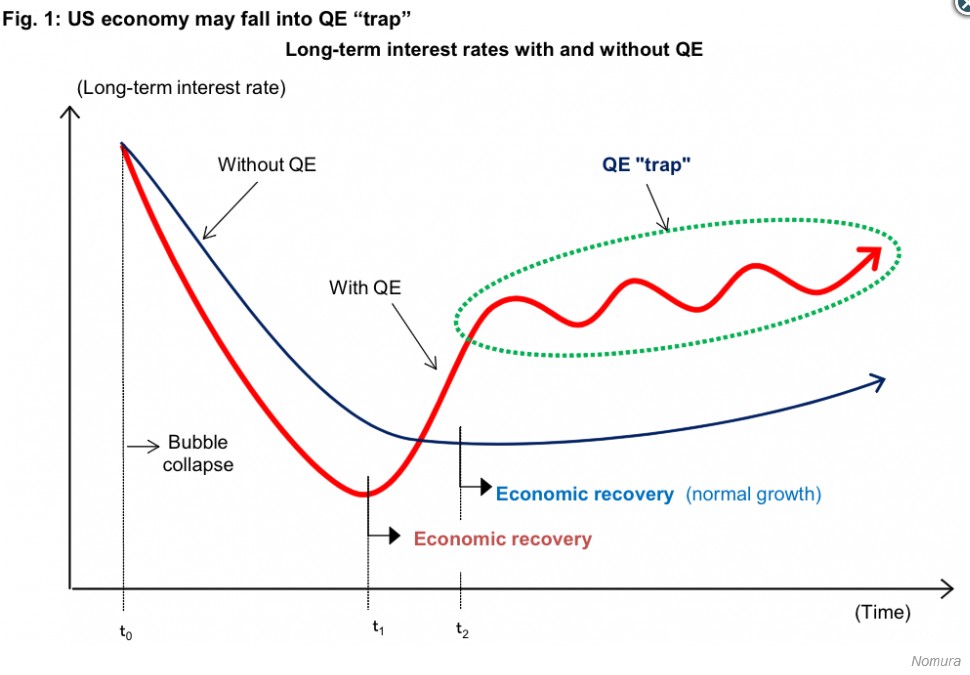

Back in an October article, we mentioned warnings from Nomura’s Richard Koo that central banks’ QE programs risked a nasty payback he called a “QE Trap.” In essence, Koo warned that the benefits of QE – faster recovery due to faster cuts in interest rates, came at a cost of a slower recovery and more volatile rates once the QE taper starts, as illustrated in the chart below.

Source: Nomura (via businessinsider.com here)

02 Feb. 23 15.19

In essence he argued that although QE may bring lower rates and initial recovery faster, the payback is that QE withdrawal causes a faster increase in rates and slower, more hesitant recovery as each attempt to taper brings a rate spike as markets fear a sudden liquidity shortage and rapidly rising rates that becomes a self-fulfilling prophecy that slows the nascent recovery. In the end, nations that don’t use QE recover faster.

Specifically:

Initially, long-term interest rates fall faster, which means the subsequent economic recovery, comes sooner as shown in Figure 1 above (t1). However as the economy recovers, long-term rates rise sharply as local bond markets fear a coming interest rate spike as the central bank may suddenly drain all the excess reserves by unloading its holdings of long-term bonds. Bond prices drop, and so rates rise. Speculators try to front run the central bank by selling their bonds in anticipation of a big central bank bond sell-off, and thus a rate spike becomes a self-fulfilling prophecy.

Demand then falls in interest rate sensitive sectors such as automobiles and housing, causing the economy to slow and forcing the central bank to relax its policy stance. The economy heads towards recovery again, but as market participants refocus on the possibility of another taper, long-term rates surge in a repetitive cycle. It’s this cycle that Koo labels the QE “trap.”

In contrast, countries that avoid QE, the decline in long-term rates, and the recovery, is more gradual, as shown in Figure 1 above (t2). However because there is no need for the central bank to drain huge quantities of funds from the economy, there’s no huge fear of the central bank causing rate spikes once the recovery starts, and the rise in long-term rates is far more gradual because there is no speculative rush to dump bonds. Once the economy starts to turn around, the pace of recovery is actually faster because interest rates are lower and their rise is more predictable and thus more gradual because there isn’t the same intense fear of a sudden rate spike that alone can cause a bond selloff and rising rates.

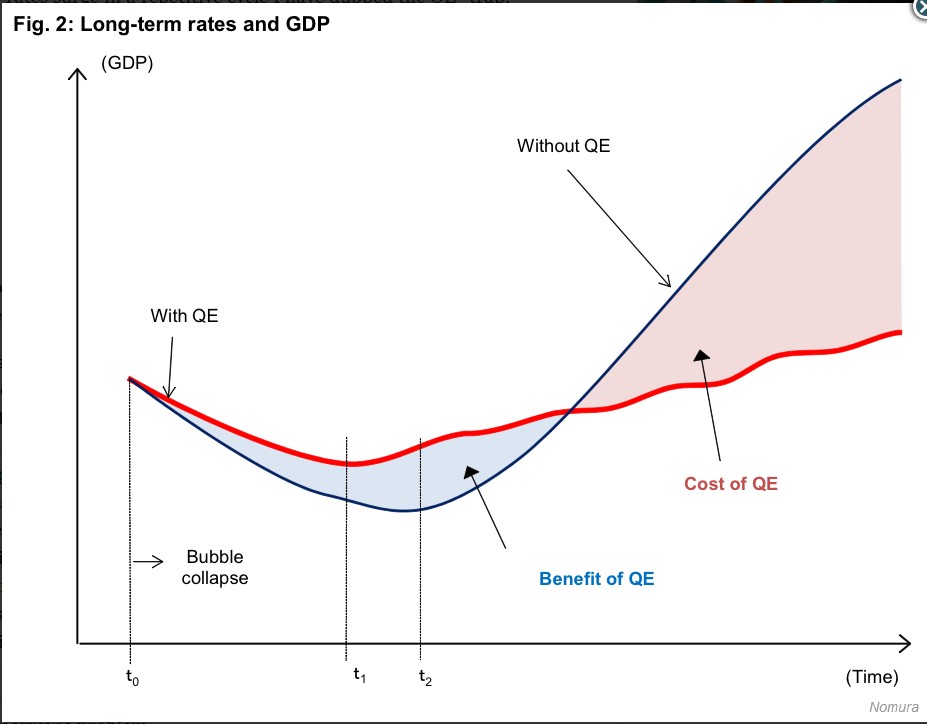

This is the point illustrated in Figure 2 below:

Source: Nomura (via businessinsider.com here)

03 Feb. 23 15.43

Now, we’re a few months into a Fed and PBOC taper. As long as you believe that a taper does not bring the feared speculation about higher rates that actually causes them by the self-fulfilling prophecy mechanism, you can argue that QE isn’t tightening.

However, market history since the first taper hints in May 2013 suggest otherwise. It suggests that markets DO in fact view tapering as a signal of at least possible coming tightening.

The analogy is: taper is to tightening as foreplay is to sex. One may not necessarily follow from the other, but the probability is higher as everyone anticipates it and gets a lot more, uh, prepared and speculative.

As noted in Barnejek’s Blog here, since Fed began the taper, look what’s happened:

- Emerging market currencies sold off hard, rates were forced higher as central banks fought to stem foreign capital flight as yield seekers from the developed world started to repatriate cash in anticipation of similar yields with lower risk, causing liquidity/credit troubles and higher borrowing costs, especially for those with foreign currency denominated debt. Even emerging market economies that had none of the unrest issues of the others, like Russia, also saw their money market rates jump on sheer guilt-by-association.

- Euonia (European benchmark overnight lending rates) rose, so did money market rates, and inflation rates dove so that there’s a deflation threat in the EU

- The PBOC decided the time had come to restrain excessively risky lending as rate pressure from the US could expose a lot of weak lenders and default risks. Here too, that mere anticipation of rising global rates became a self-fulfilling prophecy in China, which now may be facing its own version of a sub-prime crisis, as we’ve discussed in depth repeatedly (for example, here and here).

- The BoE’s forward guidance sparked an unintended rate hike speculation

As Barnejek correctly notes, the Fed’s indifference to the fate of EM’s will shift to passionate obsession if those troubles start to hit the US, as they likely will. Remember that the EM’s (especially the BRICs) comprise a much larger share of global demand for everything than they did in the last crisis in the late 90s. China is the single largest export customer for the US and many other leading economies that are already struggling with slow growth.

The Big Threat

The big threat here is that even if the Fed can control domestic interest rates, it’s much less likely to be able to stop a global rate shock, or at least some recurring minor shocks and volatility that could become something worse if they hit at a time when a key piece of the global economy is too vulnerable, and the dominos begin to fall.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.