The Coming Week: Top Market Movers, Lessons, & Ramifications, Biggest Threat

True Or False: Taper is to tightening as Foreplay is to….Technical and Fundamental Market Drivers And Lessons For The Coming Week And Beyond

GENERAL

Technical Picture: Global Indexes Hit Resistance, Indecision

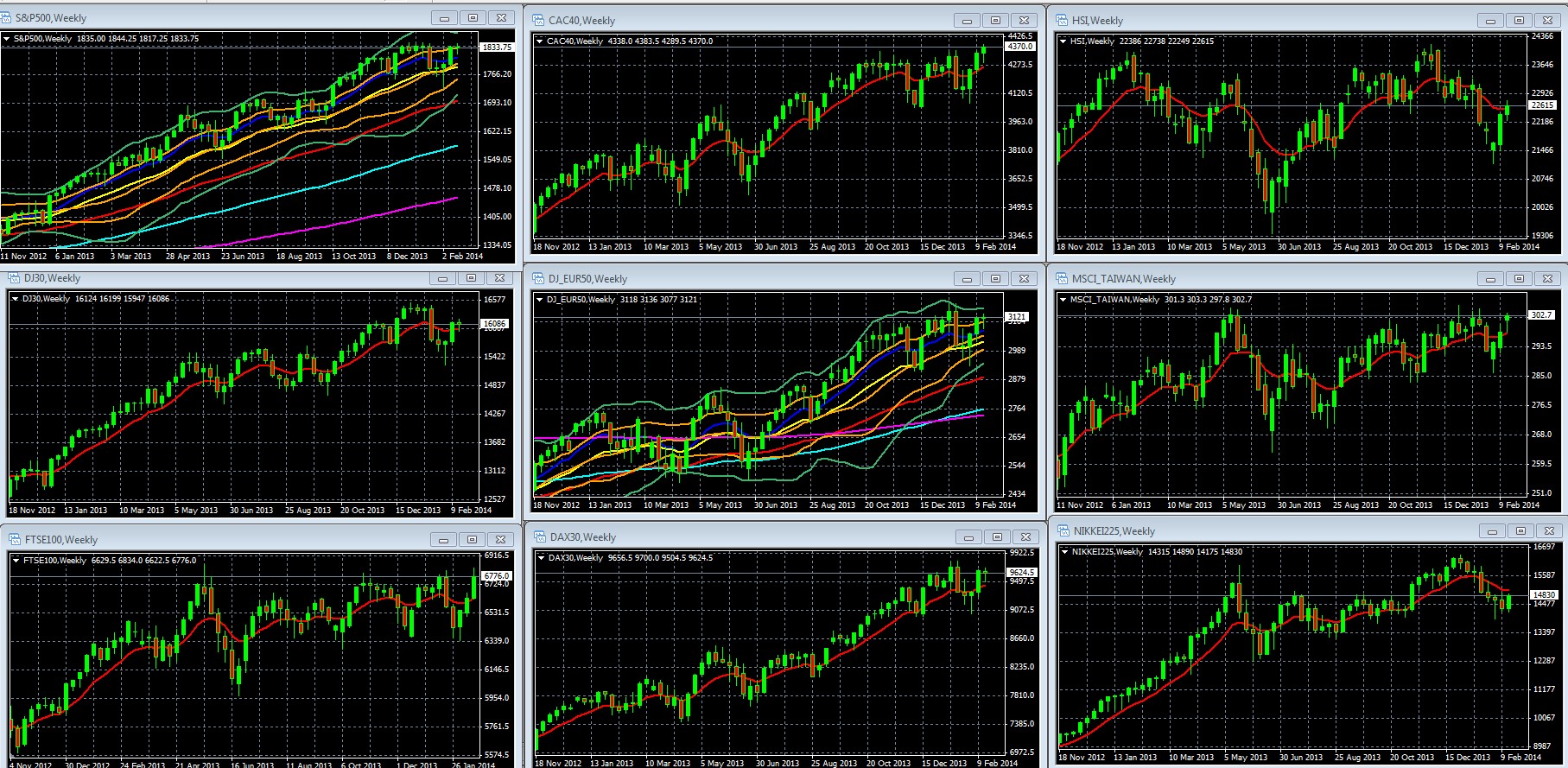

A snapshot of our sample weekly charts of leading global stock indexes as of the week’s end (below) reveals a major issue for the week ahead.

Weekly Charts Of Large Cap Global Indexes With 10 Week/200 Day EMA IN RED: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

FOR S&P 500 AND DJ EUR 50 WEEKLY CHART OCTOBER 2012 – PRESENT:10 WEEK EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, Double Bollinger Bands: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

02 Feb. 22 20.43

In short, markets have recovered their pre-EM crisis losses, are back near their multi-year or all time highs, and are waiting for a bullish or bearish catalyst to spark a breakout higher or another selloff (likely modest, similar to what we saw at the height of EM fears). In particular:

Note how US and European indexes mostly went nowhere, as indicated by frequent “doji star” weekly candles (shaped like “+) signs. This candle shape generally indicates indecision, and is especially significant when a trend hits major support or resistance, because it shows markets are respecting that resistance and are unlikely to break past it until they get a reason to do so.

Note also in the two charts in which we show double Bollinger bands, the S&P 500 and DJ STOXX50, both bellwethers of US and Europe respectively, not only do both display these dojis as they approach strong resistance of multi-year or all-time highs, they also rest at the edge of their double Bollinger band buy zones.

In sum, we’ve a double-indication that risk appetite is hitting its limits given the current outlook for the fundamentals that have fueled the rally: global growth, earnings, and central bank policy. This price level (the 1850 area on the S&P 500) has been repeatedly tested since December and has held firm, so until we get some material new fundamental drivers (better growth data, new easing?) the odds favor a period of flat range trading within the horizontal channel of the past month or so. On the S&P 500, that would be between the 1750-1850 area.

LIKELY CATALYSTS FOR THE NEXT MOVE?

The above begs the question of what will provide the next catalyst for either a decisive breakout above that strong resistance (like the 1850 zone on the S&P 500).

Here’s a brief rundown of potential big market movers this week.

Updates On Ukraine Default Prospects And Ramifications

On Friday Standard & Poor’s downgraded Ukraine’s credit rating from ‘CCC+’ to ‘CCC’, and warned that the nation is at risk of default. The current turmoil makes previously promised Russian aid uncertain, given that the Russian government’s support for Ukraine is tied to the ousted President Yanukovich’s political orientation away from the EU and toward Russia. While the EU and other Western sources of aid may yet be offered, details and conditions are unknown, leaving a real possibility of default on upcoming debt service payments.

The danger here is in the contagion risk if a default or even imminent risk of one undermines confidence and starts another EM crisis or interbank lending freeze to banks believed to have heavy Ukraine exposure. See here and here for further details.

Part Two of Fed Chair Testimony

Janet Yellen’s semi-annual monetary policy testimony before the Senate Banking Committee, which was rescheduled from last Thursday to this Thursday, could provide answers and new insights to such questions as:

- Fed taper plans and what it would take to change them.

- How much we can really blame the weather for the recent weak US data.

See below for more on the Fed

The Debate Over Connection Between US Slowdown and Weather

The US recovery story is under pressure as top-tier U.S. economic data points like employment, housing, and retail sales have been deteriorating in the U.S. over the past two or three months.

The big question is how much of that weakness has been due to unusually harsh winter weather, and thus how much deferred demand will be returned to these data points once the weather abates.

The stakes are high – if in fact the weakness is due to more longer term problems, the outlook for the US, and thus the global economy, would suffer a downgrade.

Goldman Sachs was out with a report last week claiming that the weather was to blame for a bit more than half of the slowdown, and thus that there is more long-term weakness in the US economy.

Even more ominously, it noted a rising frequency of such weather, implying that this degree of weather-related damage may not be such an aberration in the years ahead.

See here for further details.

Retail Earnings To Provide More Clarity on Weather Damage?

Earnings season is winding down, however coming earnings reports from retailers will be in focus as the weather has added to the sector’s many woes.

Retail earnings set for release next week include Home Depot Inc. (HD), Lowe’s Companies Inc. (LOW), Target Corp (TGT), Macy’s Inc. (M), TJX Companies (TJX), JC Penney Company Inc. (JCP), Best Buy Co Inc. (BBY) and Gap Inc. (GPS). Given that markets have proven willing to blame the weather for weak data, we doubt these reports have much downside potential. Earnings usually have little impact at this time, but if these surprise to the upside they might provide an excuse to rally, especially if the prior days were selloffs and markets are ready for at least a short technical bounce on any excuse.

Q4 Earnings: Good But Not Great, Nor Likely To Be Relevant

Per Reuters here, out of the 441 companies in the S&P 500 that have reported earnings through Friday, 65.3% of earnings were above analysts’ expectations, slightly below the 67% rate for the past four quarters, but above the 63 percent average since 1994.

Fed Groping For Direction & Bearish Implications

Last week, in parts 1 and 2 of our Lessons For The Coming Week series, we reported studies that contradict prevailing Fed and ECB policy, and by implication reminded readers that our leading central banks have much less knowledge than power. They are improvising as they go.

This is a lesson to remember so that you don’t take the current complacency at face value.

- The current situation of global stock markets does not present an especially compelling value story:

- Most leading global stock indexes near all-time highs

- The global economy is at best in “slow recovery”

- A real chance of a crisis in the EU, Japan, or EMs

Here’s a new reminder central bank policy failure risk from the past week.

Art Cashin, the veteran NYSE trader from UBS Financial Services warned here that the past years’ accumulated cash in banks from global stimulus presented a:

“…very dangerous situation. If that money were suddenly to get velocity, inflation could break out.

Conversely, by pushing on a string and not getting anything done, they may wind up being in a spot where, if the economy moves to stall-speed, we’ll get deflationary pressure. Yes, they’ve begun treating the patient with very, very drastic remedies, and my concern is: Is it ultimately damaging the body in a way that will bring back some of the horrors they tried to avoid?”

FOMC Minutes Key Take-Aways

The FOMC wants to ditch the 6.5% unemployment rate threshold to raise interest rates given that its rapid fall despite ongoing labor market weakness suggests it isn’t an accurate gauge of labor market strength needed to justify starting rate hikes. It’s just proving to be inconvenient as it implies coming rate hikes when the Fed doesn’t want to send that message yet.

The FOMC is uncertain how to change forward guidance, but main idea is that barring a sudden material change in the “slow but steady” US recovery story, taper continues but no rate hikes until mid-2015. Note that when anyone predicts a change 18 months ahead without some attempt to back it up with hard data, we suspect they’re really just guessing, as no one will remember what they said 18 months ago anyway.

The mere fact that interest rate hikes even entered the discussion was mildly bearish, as suggested by the WSJ’s chief Fed-watcher Jon Hilsenwrath

The Fed expressed more concern about low inflation, with some members wanting explicit language saying that it’s equally undesirable to have inflation persistently above or below the Fed’s 2% target.

In sum, don’t expect any changes to the pace of the QE taper or to interest rates from the Fed. There was nothing in the statement to suggest any change in the Fed’s taper policy, so we expect another $10 bln reduction to $65 bln/ month to be announced at the March meeting. However the Fed does appear to be groping for a change in how it communicates its message of continued taper and low rates. The 6.5% unemployment threshold by itself no longer signals coming rate increases because that level does not indicate enough labor market strength to justify wage increases.

Stocks were already completed half of their pullback for the day after the weak housing data, and only fell a bit more afterwards. So this potentially market moving event was not a big market mover given the lack of any material surprises.

As noted in our weekly review here, the modest drop in US stocks Wednesday was due to a combination of weaker housing data and the mildly bearish FOMC minutes, neither of these was a big market mover by itself.

Fed, PBOC QE

QE Giveth, Taper Taketh Away?

QE Taper May Not Be Tightening, But It Sure Feels That Way

Forget about the theoretical debate over whether QE is in fact tightening. The behavior of global markets since the start of the taper suggests the Fed and other central banks that seek to cut back stimulus are confronting a QE trap.

In other words, tapering may not be the same thing as tightening, it’s just having the same effects.

Back in an October article, we mentioned warnings from Nomura’s Richard Koo that central banks’ QE programs risked a nasty payback he called a “QE Trap.” In essence, Koo warned that the benefits of QE – faster recovery due to faster cuts in interest rates, came at a cost of a slower recovery and more volatile rates once the QE taper starts. See here for details.

Key Calendar Events

Overall there isn’t a lot of top tier EU data, and that leaves the pair to move more on two big US data points and overall risk appetite-driving events: The big events for the week are German inflation data, and US durable goods and preliminary CPI, as detailed below.

Monday

Germany: IFO business sentiment

EU: CPI – any surprisingly strong deflation signs increase the odds for some kind of ECB easing attempt, though as noted below about Friday, the odds of actual ECB action are much better if Germany is also feeling that pain.

Wednesday

US new home sales: a positive surprise could counteract the uniformly negative picture from last week’s housing data, though we’re more likely to see more of the same disappointment.

Thursday

US: Durable goods, weekly unemployment – durable goods is the more important of the two but either could help reverse the string of disappointing US economic data.

Friday

EU Flash CPI: Although EU CPI figures will also be reported, the one that matters is German CPI for February. Note well that the ECB has only actually acted against deflation threats when German inflation figures implied deflation: both the November 2013 rate cut and the July 2012 promise by ECB President Mario Draghi to do “whatever it takes” to save the Euro only came after Germany saw monthly deflation readings. This isn’t so surprising given that Germany is the chief obstacle to easing measures.

US: Preliminary GDP (expected to fall from 3.2% to 2.6%), pending home sales.

Saturday: China mfg PMI – is significant because it could move risk appetite up (bullish for the pair) or down.

For more on the coming market week and the biggest threat, see here.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.