Global Markets Review 2 Minute Drill: Daily Recap, Market Movers

A daily summary of global stock market price action & what caused it in Asia, Europe and the US- to help investors and traders of forex, stocks, indexes etc., get back into context for the week ahead in global financial markets

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we share thoughts about what’s driving major global asset markets. The focus is on global stock indexes as these are the best barometer of overall risk appetite and what drives it, and thus of what’s moving forex, commodities, and bond markets.

It’s a quick summary of last week’s international stock market action and what drove it. It’s our starting point for our follow up articles on:

- Lessons For The Coming Week And Beyond

- Coming Week Top Market Movers

- EURUSD Outlook

- Related Special Features: These vary each week depending on what’s happening. You’ll find them here.

The exact mix of articles varies somewhat from week to week, depending on what’s likely to be most important for the coming week and beyond. You can find all of these here as they come out over the weekend. You can skim it in about 2 minutes, or take a bit more time to study it. A useful weekly summary of what’s driving global asset markets, very useful for putting you into context for the coming week.

That’s why I write it as part of my own research and analysis.

MONDAY: Modest Follow Up To US Close Friday

Asian indexes closed solidly higher overall [Japan +0.6%, Hong Kong +0.6%, China+0.8%, India +0.9%, Australia +0.52%, Korea +0.31% Singapore +1%] despite negative Asian data, primarily on follow up to US gains Friday after Asia had closed.

European indexes were overall up about 0.4% on thin volume.

US stock markets were closed for the Presidents Day holiday.

TUESDAY: Asia’s Big Divergent Moves From Divergent Central Bank Moves

Asian indexes were mostly mixed with minor up or down moves. There were two big exceptions. Japan soared on news of new central bank easing, and China sank on news of central bank tightening. Specifically:

- Japanese stocks jumped 3.1% after the BOJ announced that it would extend three special loan facilities by a year from their scheduled expiry at the end of March. It also kept monetary policy steady, and maintained its upbeat assessment on Japan’s economy. The move was probably in response to very disappointing Q4 GDP figures reported Monday (-0.3% vs. +0.7% forecasted), as many had expected consumers to move purchases forward ahead of a value-added tax (VAT) coming in April.

- The PBOC drained $7.9B from the country’s liquidity by selling 48 bln yuan in repurchase contracts, the first such move in 8 months, after weekend data showed that aggregate financing had climbed to a record 2.58 trln yuan ($425 bln) in January from 1.23 trln yuan in December, despite the bank’s attempts to reduce lending.

European indexes were mixed, with mostly minor up or down moves, as a poor ZEW sentiment reading and weak retail sector (in the wake of a few stock downgrades) weighed on the indexes.

US indexes were mixed [Dow -0.15%, S&P +0.11%, Nasdaq +0.68%] and mostly flat, with poor readings from the NY Fed’s Empire State manufacturing index and the NAHB’s housing market index. Weak earnings from Coca-Cola (KO) also weighed specifically on the Dow. In contrast, the tech-heavy Nasdaq was lifted to a 13 year high by its healthcare sector components on M&A activity as Actavis bought Forest Labs for $25 bln.

WEDNESDAY

Asian indexes were mixed, with a diverse variety of up or down moves [Japan -0.5%, Hong Kong +0.3%, China +1.1%, India +0.4%, Australia +0.25, Korea -0.20 Singapore +0.59]. In sum another day of drifting or technically inspired moves, following the overnight close in the US. The only material moves came from local issues. For example, the Nikkei had hit resistance on daily charts and there was no news to support further gains, so after the prior day’s big 3.1% gain profit taking was tempting.

The same comments apply to the similarly flat performance of European indexes [UK FTSE 100 +0.01% Germany -0.07%, France +0.24% Spain +0.11% STOXX50 0.01%].

In contrast, US indexes were all down solidly [Dow -0.55%, S&P -0.65%, Nasdaq -0.82%] and that result bears some logical connection to the events of the day, particularly:

- Weak housing data, with both building permits and housing starts missing expectations. Housing starts power-dived 16% month-over-month in January to an annualized rate of 880,000. Building permits fell 5.4% to 937,000. Both figures were below expectations by a wide margin. See our post on lessons for the coming week here for the details and implications.

- The FOMC meeting minutes release: Fed officials agreed unanimously to continue the taper program but revealed little consensus over short-term rates – a mildly bearish result that was not unexpected but adds uncertainty about the real matter of concern – when the Fed will start raising benchmark interest rates. The WSJ’s chief Fed-watcher found the mere re-entry of rate hikes into the FOMC’s discussions somewhat hawkish and thus bearish for stocks.

- Before the release of minutes:

- Atlanta Fed President Dennis Lockhart said he expects the first rate hike in mid-2015

- The IMF warned of a still-weak economic recovery with significant risks remaining.

THURSDAY

Asia closed mixed but mostly lower on data showing that China’s factory activity is slowing at a faster pace.

European indexes closed mixed with generally modest gains or losses on the day. These reflected the muddled nature of the recent data, bearish China mfg data and FOMC minutes versus bullish US mfg data and the prevailing resilience of developed world stocks

In contrast, US stocks closed solidly higher [Dow +0.57%, S&P +0.60%, Nasdaq +0.70%], shrugging off a batch of top tier potentially market moving reports that missed expectations. Why? The likely answer is in the daily chart of the S&P 500 or Dow, as both began the day firm support on the daily charts, so we call this your basic technical bounce within an overall uptrend on both daily and longer term charts.

FRIDAY

Asian indexes closed higher overall [Japan +2.9%, Hong Kong +0.8%, China -1.2%, India +0.8%, Australia, +0.52%, Korea +1.41%, Singapore +0.43%], following up on the higher US close during the night. China was the big laggard, as continued credit market turmoil expected, plus Thursday’s weak recent manufacturing data tempted weekend profit takers.

European indexes were mostly solidly higher [UK FTSE 100 +0.37% Germany +0.40%, France +0.59% Spain +0.06% STOXX50 +0.42%] on no particular news other than some analyst upgrades for a few French stocks. So we call today’s result random market noise.

Earnings results continue to be good enough to prevent a selloff. Per Thomson Reuters Starmine data, out of the 60% of the STOXX 600 companies that have reported results roughly 59% have met or beaten expectations, with net profits rising 1.2 percent year-over-year on average.

US indexes inched lower [Dow -0.19%, S&P -0.19%, Nasdaq -0.10%] as news was mixed at best.

Dallas Fed’s Richard Fisher said he would continue to promote the rolling back of the Fed’s monthly asset purchases- mildly bullish

Existing home sales fell more than expected in January, providing confirmation of the weak housing data earlier in the week, and providing yet another sign that the housing market is being hurt by higher mortgage rates and harsh winter cold.

|

Index |

% Change This Week |

YTD % |

| DJIA |

-0.3 |

-2.9 |

| Nasdaq |

0.5 |

2.1 |

| S&P 500 |

-0.1 |

-0.7 |

| Russell 2000 |

1.3 |

0.1 |

CONCLUSIONS

In conclusion, here’s a snapshot of global stock indexes as of the week’s end and a few observations.

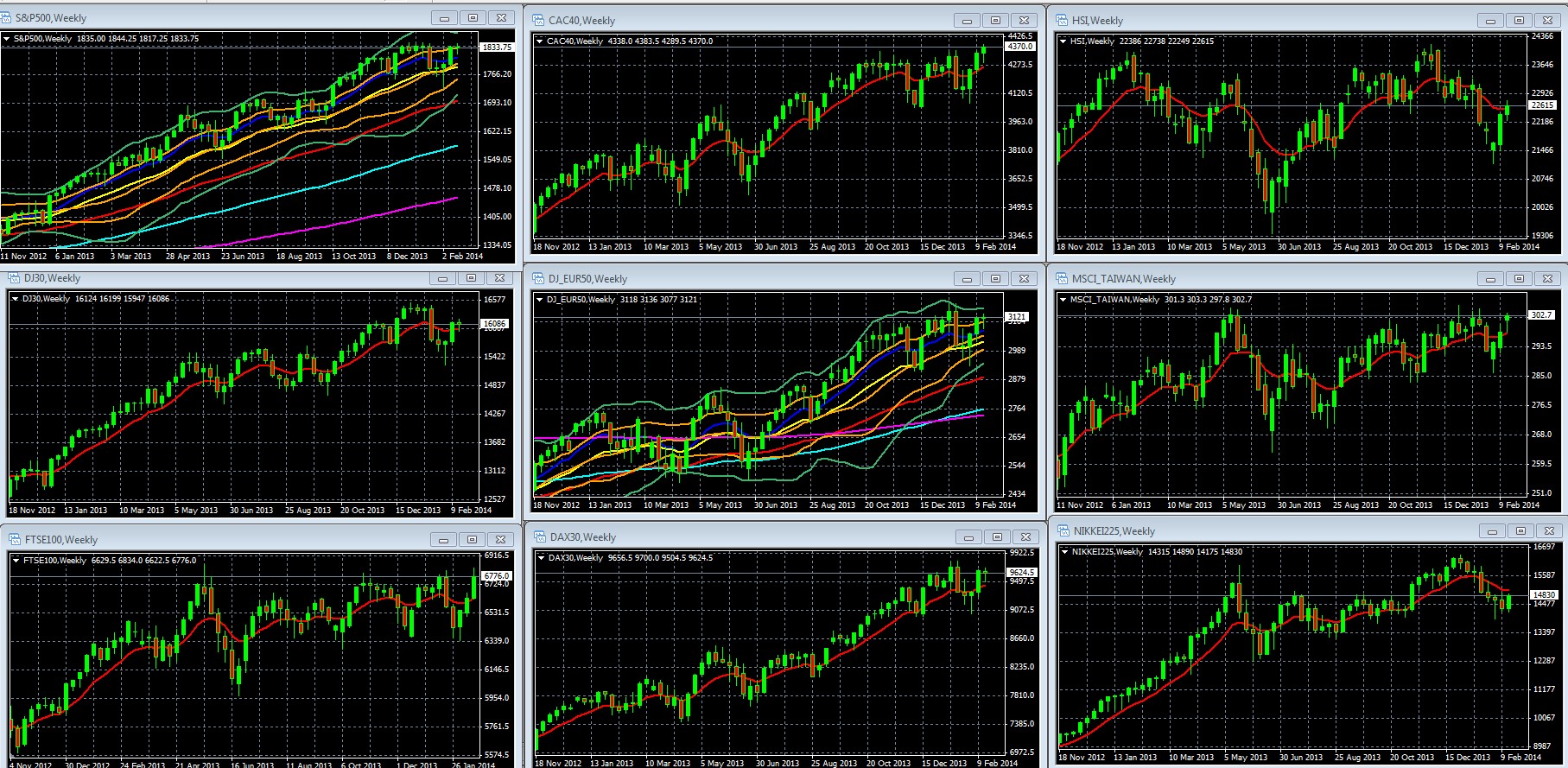

Weekly Charts Of Large Cap Global Indexes With 10 Week/200 Day EMA IN RED: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

FOR S&P 500 AND DJ EUR 50 WEEKLY CHART OCTOBER 2012 – PRESENT:10 WEEK EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, Double Bollinger Bands: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

02 Feb. 22 20.43

Note how US and European indexes mostly went nowhere, as indicated by frequent “doji star” weekly candles (shaped like “+) signs. This candle shape generally indicates indecision, and is especially significant when a trend hits major support or resistance, because it shows markets are respecting that resistance and are unlikely to break past it until they get a reason to do so.

Note also in the two charts in which we show double Bollinger bands, the S&P 500 and DJ STOXX50, both bellwethers of US and Europe respectively, not only do both display these dojis as they approach strong resistance of multi-year or all-time highs, they also rest at the edge of their double Bollinger band buy zones.

In sum, we’ve a double-indication that risk appetite is hitting its limits given the current outlook for the fundamentals that have fueled the rally: global growth, earnings, and central bank policy. This price level (the 1850 area on the S&P 500) has been repeatedly tested since December hand has held firm, so until we get some material new fundamental drivers (better growth data, new easing?) the odds favor a period of flat range trading.

Growth remains at best slow and steady, and the next likely moves in interest rates from most major central banks are likely to be steady or higher. The two central banks most likely to consider further easing at this stage are the ECB and BoJ. If either did ease, that would benefit the USD versus the EUR.

For more on the coming market week and the biggest threat, see here.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.