EURUSD WEEKLY OUTLOOK: Clarifying The Mixed Technical & Fundamental Picture

FX Traders’ weekly EURUSD fundamental & technical picture, this week’s market drivers that could change it- the bullish, the bearish and likely EURUSD direction, Impact of Ukranian Crisis, US Jobs, Other EURUSD drivers

The following is a partial summary of the conclusions from the fxempire.comweekly analysts‘ meeting in which we share thoughts about what’s driving major global asset markets. The focus here is on the EURUSD’s weekly outlook for forex traders, from both a fundamental and technical perspective.

Key Points

- Short term technical picture, fundamental drivers, and entry/exit points

- What Could Reverse The EURUSD Up Trend

- Calendar Events: Crimea Succession Vote Dominates

- Conclusions

Technical Picture

Overall Risk Appetite Steady-To-Higher: Bullish For The EURUSD

Given that overall risk appetite, as reflected in the major stock indexes (especially for the US and Europe) is a primary EURUSD driver, we start by noting that our sample of weekly US and European index charts shown below continue to trend higher or are holding recent gains and remain in narrow trading ranges.

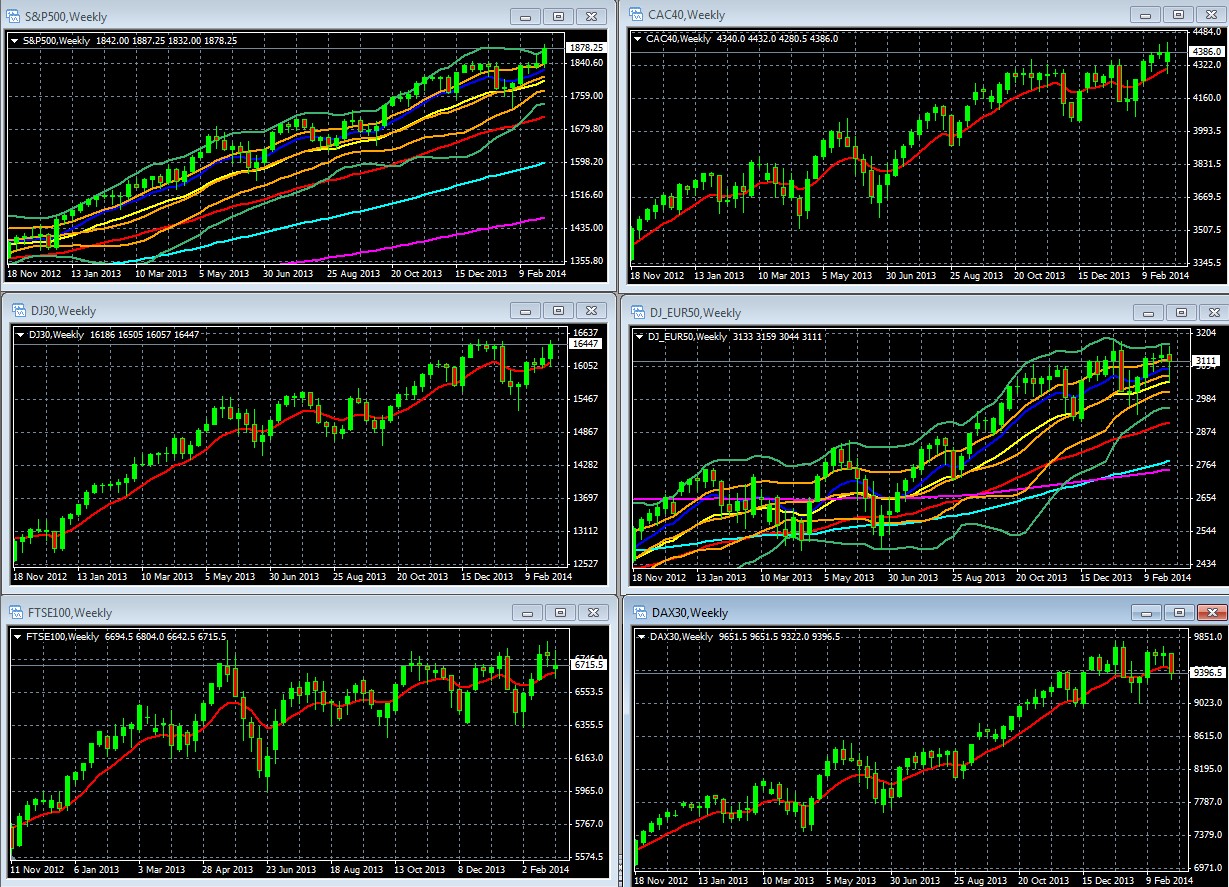

Weekly Charts Of Large Cap Global Indexes With 10 Week/200 Day EMA In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, RIGHT: CAC 40, DJ EUR 50, DAX 30

FOR S&P 500 AND DJ EUR 50 Weekly Chart October 2012 – Present: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

02 Mar. 08 22.33

Key Points To Note

Crimea Situation Not Yet A Major Market Driver: The only index to see a material pullback was Germany’s DAX (lower right). Looking at a daily chart, it’s clear that about half of the weekly pullback came Friday on signs of escalating tensions, which we detail in our weekly review of global indexes and daily market drivers article (Friday section) here. German stocks are the most sensitive to the crisis (for reasons we discuss in our coming in depth look at investor ramifications of the crisis here)

Risk Appetite Remains Sound: As exemplified by the SP 500 for the US and DJ EUR50 for Europe, the major indexes are overall within their upper double Bollinger band ‘buy zone,’ indicating that upward momentum remains sound.

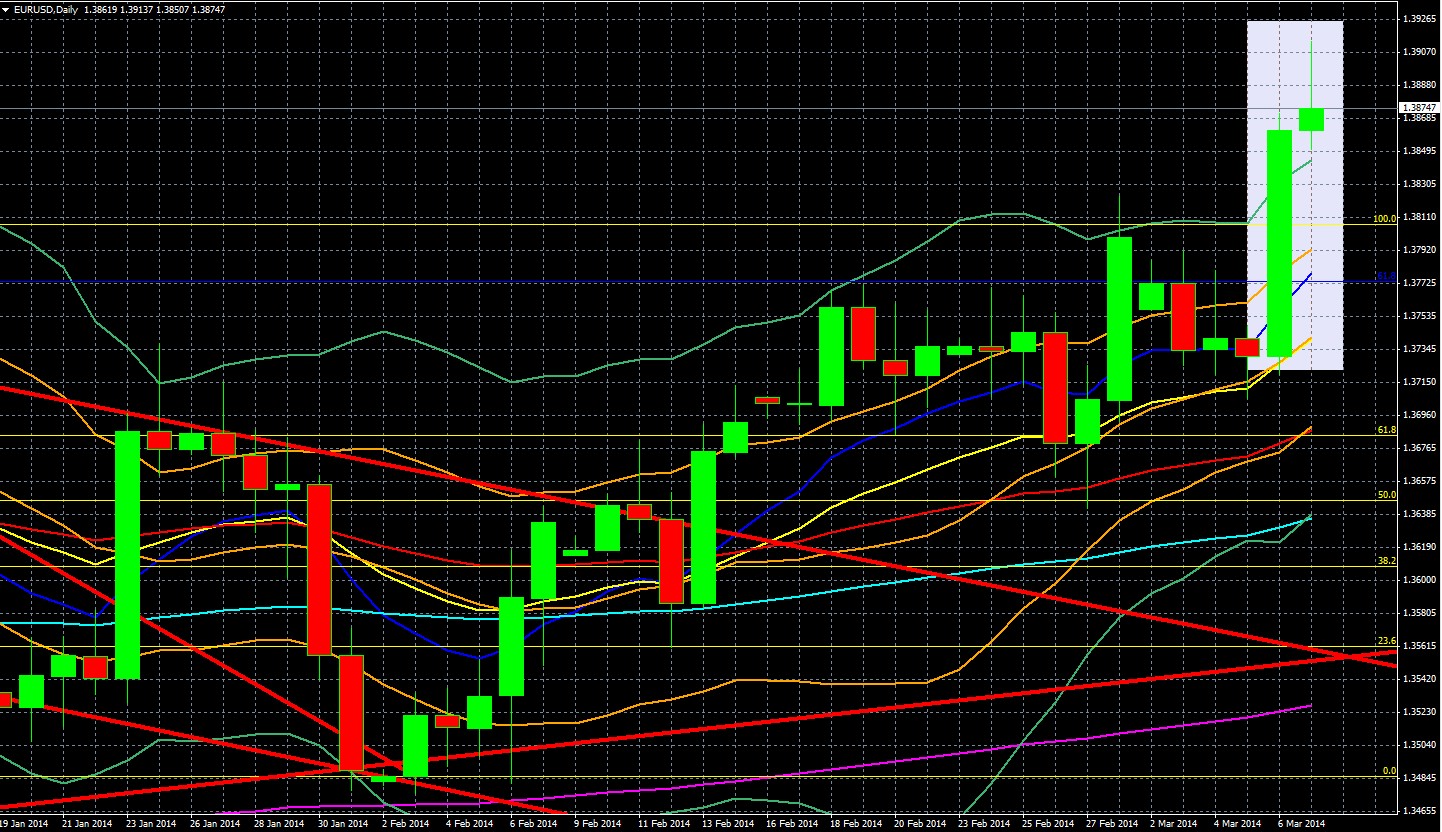

Indeed, the pair seems to be most closely tracking the SP 500 and DJIA, showing a surge higher this week of similar magnitude, and like these indexes, it advanced deeper into its upper double Bollinger band ‘buy zone,’ (indicating that momentum is strong enough for a move higher) as shown by the EURUSD weekly chart below.

EURUSD Weekly chart May 2013 – Present

KEY: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

03 Mar. 08 22.57

In sum, we’ve another case of bullish momentum bumping up against strong long term resistance. Last week decisively broke the 1.3800 level. As noted below, the calendar has some top tier events that could prompt a test higher to 1.3900 or a test of the new 1.3800 support level, depending on how the data plays out.

Note however, that caution ahead of the March 16 Crimea referendum to join Russia (likely to succeed) and the likely Western sanctions that follow, could override even bullish outcomes from the scheduled events, especially given the elevated prices for stocks and the EURUSD. More on that below. That leaves both of these vulnerable to at least a pause, if not pullback, as investors may be sorely tempted to cut their exposure ahead of likely further escalations.

We suspect Crimea escalation concerns win out and bring at least a pause if not retracement to last week’s open around the 1.3770 zone.

So what was driving this action last week?

Short Term Fundamental Drivers: Lessons From Last Week

The fundamental drivers are easy to see when we consider the EURUSD’s daily chart, and note that almost all of the pair’s gains for the week came on Thursday. Friday’s events netted out to be less influential.

EURUSD Weekly chart January 19, 2014 – Present

KEY: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

04 Mar. 08 23.09

The big EURUSD news Thursday was the ECB’s decision to do nothing, easing concerns that it might ease further and undermine the EUR. Although that move was the most important news item for the pair, it was also largely expected. So we could suspect that the positive results from Spanish and French bond auctions, German factory orders, weekly jobless claims and revised non-farm productivity also helped as all were bullish and thus boosted the EUR vs. the USD.

In contrast, the pair’s move Friday was much smaller, and most of that was surrendered, with the pair closing near its lows for the day. Again, this behavior mimics that of the major US and European stock indexes, which had either minimal gains or losses Friday, because escalating Crimea tensions were a bearish counterweight to the bullish US jobs reports.

Granted, one could argue (as does dailyfx.com’s Christopher Vecchio here) that it was the jobs report that prevented more of a follow through gain on Friday for the EURUSD. However given how well the pair has been tracking the leading US and European stock indexes on a daily and weekly basis, we believe the same drivers are working on both the indexes and the EURUSD.

In sum, the ECB rate decision was the big bullish news item, while overall rising risk appetite remains the pair’s prime driver. That said, the Crimea situation has proven itself a potential bearish force if tensions continue to escalate, as shown on both Monday and Friday in the performance of both global stock indexes and the EURUSD.

The big question for the coming weeks is which driver last longer: Crimea tensions or improving US jobs reports (and other data that suggest that the long anticipated interest rate advantage for the USD finally arrives).

Although it’s in no one’s economic interest to escalate tensions, there are longer term considerations that could easily override those interests.

The Crimea referendum on March 16 is likely to bring Russian annexation and some kind of Western counter-escalation, though we doubt the US and Britain are prepared to honor their treaties to preserve Ukraine’s territory given the lack of popular support for a new Crimean war.

What Could Reverse The EURUSD Up Trend?

- Crimea Referendum Brings Safe-Haven Demand For USD? Further Crimea escalations and a prolonged crisis serve no one’s economic or geopolitical interests, which is why market behave as though they expect a peaceful resolution or at least stabilization without an official agreement. Crimea is currently the only near term source of a flight to safety that benefits the USD. The March 16 Crimea referendum is likely to succeed and thus provoke some kind of additional Western sanctions, with unknown consequences of further rounds of tit-for-tat responses. Barring a radical improvement in US data that moves up USD rate hike expectations, a Crimea escalation looks like the most likely source of USD demand. So keep an eye on the situation.

- USD’s Anticipated Rate Advantage? This bearish driver for the pair appears to be receding into the more distant future.

- Taper Priced In: While the Fed’s QE taper looks even more likely to continue after Friday’s jobs report, whatever USD support it can provide seems priced in already given the pair’s steady ascent since July 2013.

- USD Rate Increases Not Imminent: Still not expected until some point in 2015 barring a radical improvement in US the US jobs, income, and spending picture.

- ECB Easing Not Imminent:

- ECB President Mario Draghi made clear in Thursday’s press conference that the ECB currently sees no need to inject more liquidity into the Euro-Zone banking system.

- Interbank lending rates (EONIA) have remained below the ECB’s reference rate of 0.25%, indicating that there is no big credit crunch.

- Sovereign yields are at multi-year lows and if anything falling further (and so bond prices are at highs). As shown above EU stocks continue to hit or remain close to multi-year highs.

- The recent PMI surveys show continued modest growth and Euro-Zone inflation inching higher, and economic data has been overall steady-to-improving.

- Sovereign or banking system contagion risks seem like a distant memory (though we’ve repeatedly warned (for example here and here) that the single resolution mechanism’s (SRM) profound inadequacies means that the EU remains as vulnerable as ever to a material bank failure threat, which is likely to come if in fact the ECB’s coming stress tests are truly rigorous.

- Yet announcing liquidity injections before the results come out might signal that the ECB has already discovered significant problems before it has even finished its review banks’ balance sheets.

- So in order to prevent spooking markets about bank troubles for which there is no real SRM solution, the ECB feels compelled to do nothing until a crisis is apparent (the better to coerce persuade Germany to accept a much quicker formation of a bigger common bank bailout fund and less control over its use).

Thus while the ECB stands ready to act if necessary, it doesn’t believe the time has come. This is not passive inaction, but rather a deliberate decision to refrain from action until a crisis provides the needed agreement from funding nations like Germany that it’s time to ease further.

That easing could assume a number of forms, though we suspect the ECB wants to avoid another program that allows banks to earn ECB-subsidized returns without actually increasing lending to businesses.

For example a BoE-type Funding for Lending Scheme (FLS) could ease credit conditions at the consumer and small business level without risking a EUR-dilutive huge ECB balance sheet expansion that another LTRO or a US-type QE would create, and which would risk German opposition.

Calendar Events

As noted above, caution ahead of the March 16th Crimea referendum and the new round of Western sanctions it could impose is the biggest potential market mover. Neither the US nor EU have more than a few top tier data releases, so the EURUSD is more likely moving with overall risk appetite, which in turn will most likely be influenced by the following:

Monday:

China: inflation data from Sunday.

Eurogroup meetings: Use of the ESM as a fund for bank recapitalizations will be discussed. Remember that this was supposed to be used to aid insolvent governments, not banks, and that Germany is thus far opposed to turning it into an all-purpose common fund.

Tuesday:

EU: ECOFIN Meetings: Discuss the SRM and EU parliament amendments of the current draft from December 2013. German trade balance

US: JOLTs job openings – it’s important to the Fed as a measure of the US job market. Given that the taper is unlikely to be paused or delayed, the bigger potential is for good news to raise the odds for an earlier than expected rate hike which would be USD bullish. This is unlikely given the Fed’s cautious approach to tightening as long as inflation remains subdued.

Thursday

China data dump-industrial production, fixed asset investment, retail sales

US retail sales – useful if it’s good and confirms Friday’s jobs number. If negative, that just muddies the picture with conflicting data. Also, weekly new jobless claims, which could confirm the Friday jobs improvement theme.

Friday: US inflation data and preliminary UoM consumer sentiment.

Sunday

Crimea popular vote on whether to secede from Ukraine and become part of Russia. Given the Russian majority, and perhaps presence of Russian troops it is expected to pass, even if there is a free and fair election

Real Time Retail Trader Positioning Sample

The chart below of real time sample of nearly 500 retail traders, average holding period 7 weeks, remains little changed from last week, still heavily short the EURUSD, despite the entrenched EURUSD uptrend and mixed short term technical and fundamental picture.

EURUSD Sample Retail Trader Positioning Dec 30 2013 To Present

Source: Forexfactory.com

05 Mar. 09 03.19

To these patient, long suffering souls shorting the EURUSD before the trend shows signs of turning (which we discourage in our book) we dedicate this song from reggae immortal Bob Marley. Before clicking, can you guess which song it is?

Conclusion: Direction of EURUSD This Week

The Bearish: Technical resistance around 1.3900 plus uncertainties about further escalation from the Crimea referendum.

The Bullish: Technical Momentum

We suspect the pair could test resistance at 1.3900, but that it’s unlikely to stay above that level until the Crimea situation becomes clearer, and is more likely to remain within its range of the past 2 weeks.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.