Fools Russian: 1 Chart Shows Why Russia Tension-Related Selloffs A Buying Opportunity

There are many reasons to be bearish. Fear of a protracted economic sanctions war between Russian and the West isn’t one of them. Here’s why and what to do if markets sell off on related fears

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we cover the top real and imagined market movers worthy of a special report.

Summary

—Russia’s position as a primary energy supplier alone minimizes chances of sustained Western economic sanctions

—Russia’s economy would also suffer from an economic sanctions war, but Putin has far more political support for this conflict than Western leaders

—Control over its neighbors is far more important to Russia than for the West

—Guidelines on how to play a Russia vs. West escalation-driven market selloff

Fools rush in

Where angels fear to tread…

…Fools rush in

Where wise men never go

(Song: “Fools Rush In (Where Angels Fear to Tread)” -Lyrics By Johnny Mercer)

Buy when there’s blood in the streets – Baron Rothschild

Be greedy when others are fearful – Warren Buffet

Via: Business Insider/Matthew Boesler here

06 Apr. 20 04.37

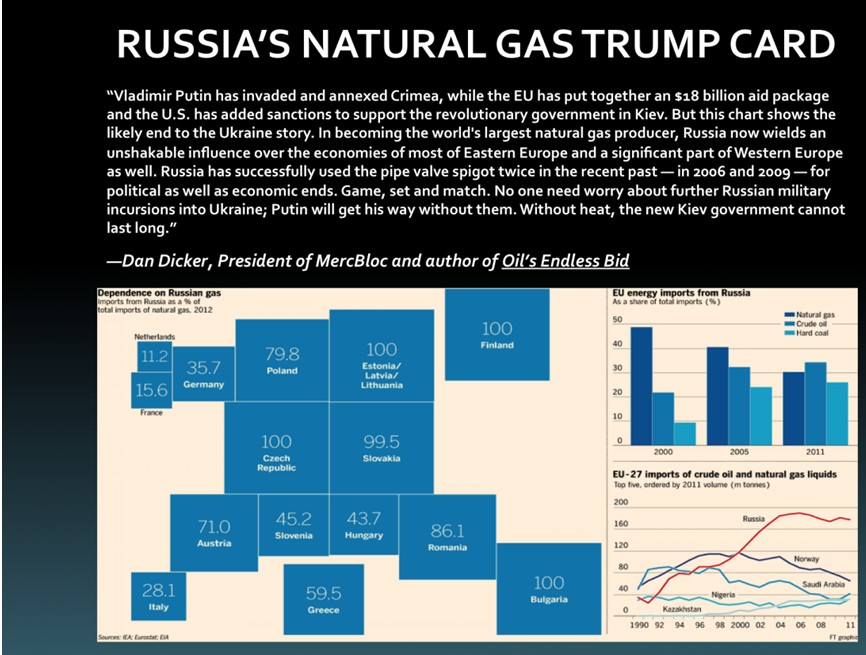

Given the facts in just this one graphic, Europe has every motivation to avoid a sanctions war with Russia.

If the above isn’t enough proof for you, the EU’s real leaders have little enthusiasm for curtailing trade with Russia.

First, consider Germany’s position. Wolf Richter had a great piece on that back in March, German Exporters Fire Warning Shot About Russia “Sanction-Spiral,” Banks At Risk. Highlights include:

German Exporters Oppose Tough Sanction

Anton Börner, president of the German Association of Exporters (BGA), which represents 120,000 companies, the lifeblood of the economy, warned at a press conference in Berlin that further escalation of the crisis in the Ukraine could hit exporters very hard. He said that the BGA expected exports to rise 3% to €1.13 trillion and imports 2% to €914 billion for a trade surplus of €215.6 billion – the highest in history. But “if the crisis in the Crimea escalates further,” these wondrous forecasts of endlessly growing exports and surpluses “could turn very quickly into a mal-calculation.

So Too Do German Bankers

It isn’t just German exporters that are fretting, and lobbying with all their might. Russia, with an economy that is already stagnating, and dogged by vicious bouts of capital flight, has$732 billion in foreign debt. Relatively little of it is sovereign debt, but nearly $700 billion is owed by banks and corporations – most of them owned or controlled by the Kremlin. Oil major Rosneft and gas mastodon Gazprom owe $90 billion combined to foreign entities; the four state banks Sberbank, VTB, VEB, and Rosselkhozbank owe $60 billion. Some of this debt matures this year and next year.

European banks and insurance companies are up to their dirty ears in this suddenly iffy and potentially toxic Russian debt.

When it comes due, it will have to be rolled over, and some of the companies will need to borrow more, simply to stay afloat. Alas, the current sanction regime of visa bans for the elite, asset freezes, and trade restrictions could make that difficult. Then there’s the threat, now more broadly but still unofficially bandied about, that Russian companies should simply default on this $700 billion in debt in retaliation for the sanctions.

Some European banks, including some German banks, might crater. Even the possibility of a major loss would further rattle the confidence in these banks with their over-leveraged and inscrutable balance sheets and their assets that are still exuding whiffs of putrefaction. And this sort of fiasco, as the financial crisis has made clear, has an unpleasant way of snowballing – and taking down the already shaky global economy with it.

During the financial crisis, German exports collapsed, banks toppled and got bailed out, and the economy experienced its two worst quarters in the history of the Federal Republic. No politician in Germany has any appetite to re-experience that. And the banking industry, with its powerful and long tentacles winding their way through the hallways and doors of the German government, has been assiduously at work, quietly and behind the scenes, to whittle any sanctions down to irrelevance. (emphasis mine)

Remember that EU banking remains as vulnerable as ever, given the EU’s recent failure to agree on a serious banking union with the means to prevent future banking crises.

I could quote similar views from French industrial groups, or from British bankers.

Of course, as is often pointed out, Russia’s economy is a mess, and it too would suffer greatly. Thus Putin has every reason to minimize the kind of blatant provocations that would force Western hands.

All of the above is well known to all sides and to investors as a whole. Thus it’s no surprise that investors remain sanguine about the crisis.

That said, so too does Putin, and the spreading rise of Russian separatism beyond the Ukraine suggests that he’ll continue to encourage apparent ‘grass roots secessionist movements’ as long as the West is unable to produce a credible disincentive.

Putin’s Political Advantage

However, Putin has broad political support for his aggressive policy, whereas the West has little appetite for economic, never mind military conflict.

Conclusion

Therefore the potential for a sustained Russia-West crisis, and sell-off, remains. If that happens, see it as a buying opportunity.

Whatever tensions flare up won’t last. In the end the West will grudgingly yield. Diplomatic relations may suffer, but otherwise it will be business as usual.

The West won’t make serious economic or military sacrifices for the sake of Ukraine or other front-line states. Russia will.

End of story.

What To Do

The short version: assets that sell off on these tensions (stocks of firms with heavy Russian exposure) should be bought. Those that rise on them (alternative energy suppliers for Russian gas customers, etc.) should be sold or shorted.

See here, here, and here for related posts on current market movers to watch. Some focus on the EURUSD, but the market drivers discussed apply to most other asset classes.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.