The Coming Week’s Top Market Movers, Lessons: The Drivers, Questions That Actually Matter

How bullish and bearish forces align for stock indexes, forex and other global markets, both technical and fundamental outlooks, likely top market movers. Why the hyped events could disappoint, problems with anticipating US jobs reports outcomes & more

Summary

–TECHNICAL OUTLOOK: Lack of new fundamental drivers & entrenched resistance cap upside, tempt tests of support, & what could change that.

–FUNDAMENTAL OUTLOOK: Calendar, earnings are not the likely real market drivers, how US jobs reports could influence markets, the latest on EU threats, etc.

–CONCLUSIONS: What US data needs to show us, updates on the EU threat-board.

The following is a partial summary of conclusions from fxempire.com’s analysts about the coming week’s likely market movers and the most important lessons learned from recent weeks to consider for this week.

TECHNICAL OUTLOOK: Long Term Resistance Holds As Indexes Lack Fundamental Motive To Rise

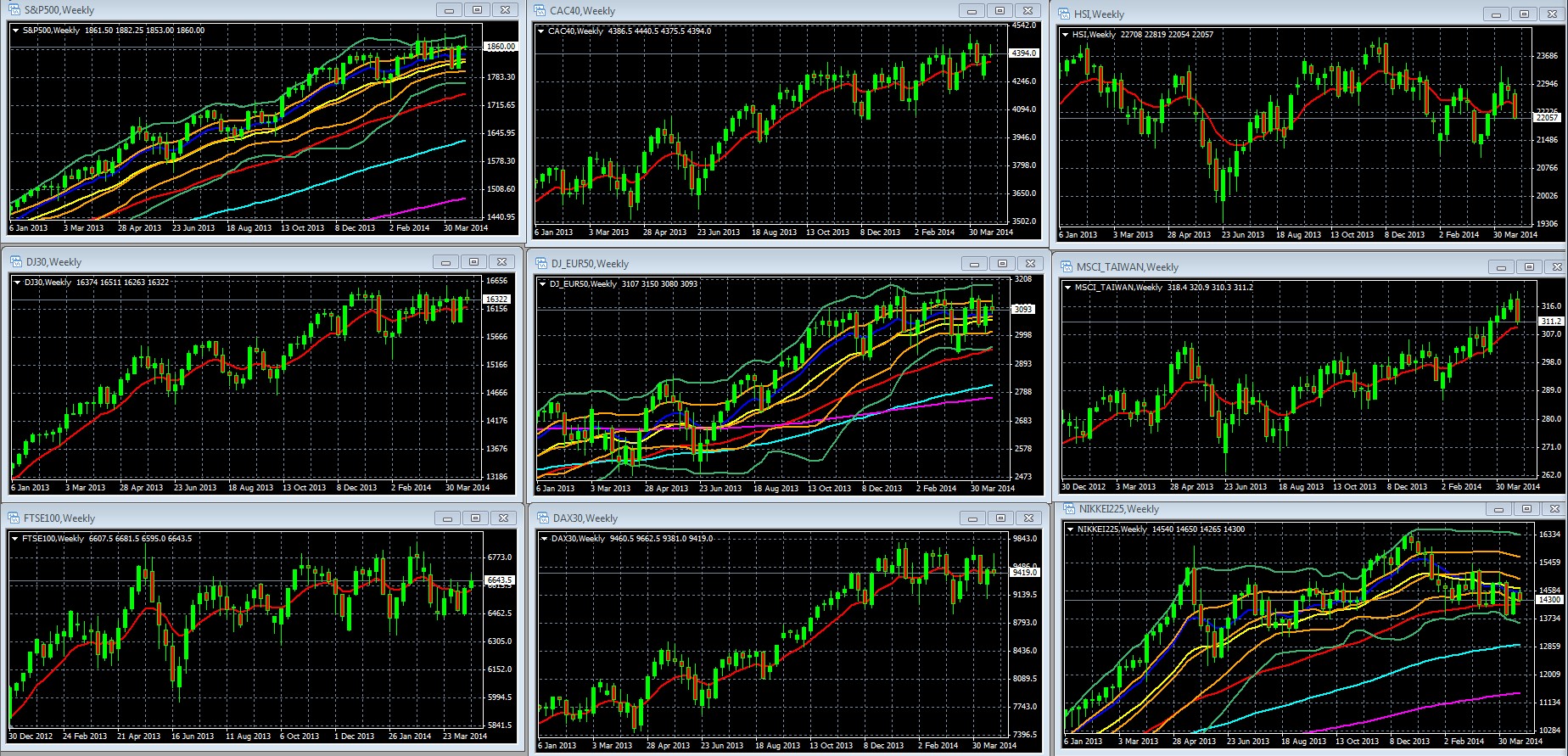

First we look at overall risk appetite as portrayed by our sample of weekly charts of leading global stock indexes. In times such as the past 11 weeks, when there have been no major surprises from fundamentals like the top tier economic reports, technical support and resistance themselves can become prime market drivers, serving as excuses to buy at support and sell at resistance.

Overall risk appetite per sample of weekly charts for leading global stock indexes shows virtually no change from the prior week. US and Western Europe stock indexes remain near all-time or multi-year highs, unable to break through long term resistance levels such as 1860 on the S&P 500.

For the past 11 weeks this nearby entrenched resistance has mattered a lot, because the absence of significant upside or downside surprises from the top-tier economic reports has left the multi-year uptrend without the needed justification to move higher.

Weekly Charts Of Large Cap Global Indexes With 10 Week/200 Day EMA [DATES] In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

Key For S&P 500, DJ EUR 50, Nikkei 225 Weekly Chart: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER® BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

03 Apr. 26 22.44

Key Take-Aways Weekly Chart: Another Flat, Indecisive Week Weakens Upward Momentum

- US indexes are barely holding onto their weakening upward momentum

- The 10 and 20 week EMAs are flattening out

- The indexes remain at the border of their double Bollinger band buy zone

- Once again we clocked yet another indecisive ‘doji’ candle this week on the S&P 500 (the third in 5 weeks) and also in most of our other US and European indexes.

- European indexes have lost their upward momentum, closing again in the double Bollinger®band neutral zone, and also showing flat 10 and 20 week EMAs.

- While US and Western European indexes continue to behave similarly, Asian indexes (on the right of the below chart samples) remain a mixed bag. Arguably they’re more sensitive to from China’s ongoing slowdown and background risk of China-Japan tensions, even though China is the biggest customer for much of the West as well.

Still Some Upside Left For 2014?

The S&P 500, as good a bellwether index as any for the West, currently sits at 1863.40. The average forecast for the S&P 500 for 2014 was around 1950, suggesting another 4.66% of upside. We suspect that even the most confident analysts would admit their predictions’ margin of error is at least 5%.

Therefore without a sustained period of better than expected data and earnings, awareness that we’ve hit the consensus target for stocks in 2014 may itself be a major barrier to further gains.

FUNDAMENTAL PICTURE

Here’s the lineup of potential market movers to watch this week.

1. US Monthly Jobs Report: Strong Consensus On The Result –Market Reaction The Big Question

- The US jobs reports are expected to continue to show slow but steady improvement, which would be in line with the general theme of recent US data. Given the FOMC’s dovish bias, it would need to see a major surprise from the jobs data (like beating forecasts by ~15 %or more) to stir any speculation of faster growth that may send markets higher.

- Indeed, even if that happened, stocks won’t necessarily rise – that would require a “Goldilocks” result – not too hot, not too cold- enough growth for optimism but not enough to raise fears of (gasp!) an increase in the scope or pace of Fed tightening that could bring (double gasp!!) a sooner than expected hike in the benchmark “r-word”. The big question is, how much jobs growth is enough, but not too much?

- As noted here, there’s a high degree of consensus on the likely outcome of the NFP report, with 43 out of 50 analysts surveyed by Bloomberg predicting results ranging from 190k to 230k new jobs. The bad news is that this range is wide enough to limit the potential for an upside surprise. The good news is that anything in that range might not contradict the “slow but steady” recovery story and provide the bullish “Goldilocks” result.

- Our take however, is that data needs to show a bit of extra strength, so anything under ~207k could well be taken as bearish, because the bad weather excuse is gone and we should see some additional new jobs from those that were supposedly deferred due to the harsh winter weather.

If the above sounds inconclusive – frankly, it is. That said, as noted above in the Technical Outlook section, US indexes remain in long term uptrends with continued upward (albeit weakening) momentum, so that trend gets the benefit of the doubt until proven otherwise.

One final thought: Even if job figures disappoints, the Fed is unlikely to slow the taper’s pace. Indeed, as we discuss in our coming special report here, there’s growing evidence that the Fed should accelerate its move to tighten.

—There’s considerable evidence that the Fed’s ability to support jobs growth is largely exhausted, and that remaining labor market slack is mostly from the longer term structural unemployed who are unlikely to benefit from more QE. If Fed claims that continued dovishness was for the sake of improved employment, then why not accelerate tightening?

—Raising a bit of rate hike fears could also raise emerging market interest rates and further tighten credit for EM nations, particularly America’s current big headache, Russia. While not generally desirable, (indeed painful for many US allies) that WOULD also conveniently provide help with Washington’s most pressing foreign policy concern – continued Russian aggression against Ukraine.

—-With no military option and Europe’s support for serious sanctions questionable, Washington’s only effective weapon is its ability to cut off Russia’s access to credit.

—-Russia’s economy is already in trouble from a US directed credit squeeze, as the Telegraph’s Ambrose Evans Pritchard discusses in detail in his post Russia’s bond market is Achilles Heel.

For details, see our coming special report on why the Fed could tighten sooner than markets think.

2. The Economic Calendar: Market Movers’ Potential Likely To Be Unfulfilled

This week, most of the likely big fundamental drivers come from the bevy of top tier US data releases, led by Q1 GDP, an FOMC rate decision, and US jobs reports on Friday, along with the earlier reports like the ADP non-farms payrolls that serve as leading indicators for the big Friday result.

This week, most of the big fundamental drivers come from the bevy of top tier US data releases, led by Q1 GDP, an FOMC rate decision, and US jobs reports on Friday, along with the earlier reports like the ADP non-farms payrolls that serve as leading indicators for the big Friday result.

Despite the potential drama and certain headlines, it will take a significant positive surprise in one of the following to get stocks breaking higher. We don’t see that happening.

- GDP is a lagging indicator that’s usually well anticipated and already priced in.

- There’s nothing in the coming week’s data to suggest a change in Fed policy and thus a hawkish Fed policy revision that would support the USD. The Fed is widely expected to continue its modest taper of $10 bln/mo.

- There’s no press conference scheduled after this month’s FOMC meeting.

- US Monthly Jobs Reports & Earlier Leading Indicator Reports: See the above section for details

See our weekly EURUSD outlook for details of the top calendar events.

The only other scheduled events of note are the coming week’s earnings announcements for Q1. As noted before, however, earnings season tends to lose most of its ability to assert sustained influence on global markets after its third week, which just ended.

3. Russia-Ukraine Tensions The Big Wildcard

As we discussed in some depth here, the current balance of evidence suggests that the global economy does not take sustained damage from this conflict, given the related risks and costs of serious sanctions and deep aversion in the West to any military involvement.

That said, there’s enough real uncertainty about the motives, commitment, and tools that are available to each side to make the near and longer term outcome deeply unpredictable. An escalating deployment of weapons, be they economic, cyber-warfare-related, or military, is a genuine risk. See here, here and here for just some of the complex details and considerations that could drive short and longer term outcomes.

They key point here is that markets have remained calm on the assumption that both sides will do what’s needed to avoid significant economic damage, AND that both sides understand the other well enough to avoid provocations that could escalate things out of control.

The past weeks’ events have done nothing to confirm that sentiment, but instead brought new violence and threatened sanctions.

LESSONS FOR THE COMING WEEK

US

Data Needs To Show Extra Strength To Support The Bad Winter Weather Excuse

With the winter weather excuse gone, it’s time for US data to prove the “weather hypothesis” for weak performance in winter data. It needs to show sustained strength that includes evidence of added strength from spending and hiring that was supposedly deferred due to bad weather. Otherwise the slow but steady US recovery story is undermined.

EU Bullish

Strong PMI’s Support EUR

These eased concerns that the ECB easing might come sooner or harder than expected. These figures also show that the strong EUR has not hurt the EU thus far, and so they help explain why markets have ignored ECB attempts to jawbone the EUR lower.

Continued Strong Demand For GIIPS Bonds Reinforces EU Calm, Aids GIIPS Recovery

Portugal and Spain both had successful bond auctions last week with borrowing costs hitting 8 and 9 year lows, respectively. This was Portugal’s first bond sale since entering its bailout program, following Greece’s return to the bond markets earlier this month. Only Italy’s sale of 2 year notes on Thursday came at a higher rate. Clearly there are enough lenders who actually believe the ECB would backstop these bonds, despite the “voluntary” private sector bail-in of Greek bonds in 2012. As long as demand remains it’s very EUR supportive both for supporting EUR demand and maintaining confidence that this dysfunctional currency union continues to function, despite its recent failure to agree on a substantive banking union. See here and here for details.

Fears Of Systemic Risks Of EU Bank Stress Test Failures Overdone?

However, perhaps the whole stress test thing is yet again just another PR exercise?

Buried in the above article was a significant qualification to any threatened systemic risks.

However, he also said that an exemption to the new resolution rules could apply if necessary to avoid a “serious disturbance” in a member state’s economy and preserve financial stability.

Given that such risk could exist with almost any large GIIPS bank, considering the lack of funding and deployment speed of the current bank resolution plan, this rule seems conveniently applicable to almost any GIIPS bank trouble.

My search for the specific clause to which Constâncio refers came up empty (anyone else find it?). That said, given the lack of support the future bank union deal provides, it makes sense that the EU should have some clause allowing it to prevent a systemic risk. Recent GIIPS bond sales certainly suggest that markets believe this clause exists.

If anyone can locate this clause, please let me know.

EU Bearish

ECB VP To EU Banks: Raise Capital Before 2015 Means Continued EUR Demand

FT.com reported Thursday that Vítor Constâncio, the European Central Bank ’s vice-president, has been pushing EU banks to raise capital (issue shares) while confidence and share prices remain high, in order to avoid failing the coming bank stress tests. He warned that such failures, given the coming rules requiring bail-ins from the banks’ depositors, lenders, and investors, could spark a systemic crisis, as these same parties at other EU banks might flee at the slightest hint that their bank could be affected.

In fact EU banks have been busily building up capital for a while, as we reported here this was good for the EUR but bad for the EU economy as banks limited lending. The point is that banks will be trying to vacuum up more EUR-denominated investment, supporting the EURUSD as it has throughout much of the rally that began in mid-2012, as the new rules and bank stress tests appeared on the horizon. Note that the feared capital requirements and how they’re reported have already been eased considerably in January, see here for details. The point here is that even those banks that pass the stress tests are not necessarily prepared to handle another EU crisis.

GIIPS Debt Service Bill Continues Rising

Interest payments alone for the EZ periphery nations will exceed €130bn in 2014 almost three times higher than the rest of the single currency area, according to calculations of the Financial Times based on the IMF World Economic Outlook database. In other words, debt service consumes ~10% of GIIPS nations’ revenues, compared to 3.5% of the other 13 EZ areas. This added burden limits the GIIPS ability to recover. For example, Portugal’s €7.3bn 2014 debt service expense alone exceeds its education budget and nearly equals its health budget. Obviously that’s not only a loss of jobs, it also impacts current and future productivity, contributing towards a less educated and healthy population.

Continued Complacency On EU Deflation, EU Crisis Potential

Even if the EU dodges outright deflation, experts are warning that even “lowflation” (0.5% to 1% y/y inflation) could be enough to exacerbate debt troubles not only for the GIIPS, but key core nations like France. At minimum, that risks hindering their recoveries. The bigger threat is if it drives their debt/GDP ratios higher and sends them back into recession or new bailouts. See here and here for more.

Meanwhile, last week top economists warned that the EU crisis remains as potent a threat as ever, despite the past years’ calm and new bull market in GIIPS stocks and bonds. Debt/GDP ratios still stratospheric for many in the periphery make these nations vulnerable if the current weak recovery reverses.

As Ft.com reported last week:

“Debts above 130pc of GDP for Italy and 170pc for Greece are a recipe for disaster once we go into the next downturn,” said Professor Charles Wyplosz, from Geneva University.

“Today’s politicians believe the crisis is over and don’t want to hear any more about it, but they have not tackled the core issues of fiscal union and public debt,” he said, speaking at Euromoney’s annual Germany conference.

As we’ve noted repeatedly, the EU has made little progress towards becoming a functioning currency union. It couldn’t even come up with a credible banking union to backstop the troubled banks that coming ECB stress tests are expected to reveal. This is just one symptom of the EU’s unwillingness to form enough of a political union that’s needed to make a currency union work.

CONCLUSIONS

Despite a week full of top-tier events, strong resistance and unlikely bullish surprises suggest that stocks are unlikely to break higher any time soon. If Wall Street’s 2014 forecasts are correct, global indexes have tapped their upward potential for the year, putting the odds in favor of flat, range bound trading.

That said, there’s plenty to watch.

–US data needs to prove that prior weakness was due to weather

— Russian backed separatists haven’t backed down, even as the West readies to announce more economic sanctions.

— Meanwhile the EU remains as vulnerable as ever to shocks that must eventually come.

Given the multi-year bull market, 11 weeks of flat trading alone could tempt markets to test deeper support, even if just as a normal phase in a longer term bull market.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.