The Coming Week’s Likely Must-Know Top Market Movers

Technical and fundamental outlooks, likely top market movers for global stock indexes and most other global asset markets for long term investors, short term traders

The following is a partial summary of conclusions from fxempire.com’s analysts about the coming week’s likely market movers and the most important lessons learned from recent weeks to consider for this week.

Summary

–Technical Picture: Neutral-Standoff Between Weakening Momentum, Resistance Continues, Short & Long Term Trend Outlooks

–Fundamental Outlook: We Had Top Tier Data Surprises, Drama, But In Aggregate Nothing To Change Expectations. Now What?

–Coming Week Likely Market Movers: With Fundamentals Like This, Technical Considerations Could Rule

The following is a partial summary of conclusions from fxempire.com’s analysts about the coming week’s likely market movers and the most important lessons learned from recent weeks to consider for this week.

TECHNICAL PICTURE

We look at the technical picture first for a number of reasons, including:

Chart Don’t Lie: Dramatic headlines and dominant news themes don’t necessarily move markets. Price action is critical for understanding what events and developments are, and are not, actually driving markets. There’s nothing like flat or trendless price action to tell you to discount seemingly dramatic headlines – or to get you thinking about why a given risk is not being priced in

Support, resistance, and momentum indicators also move markets, especially in the absence of surprises from top tier news and economic reports.

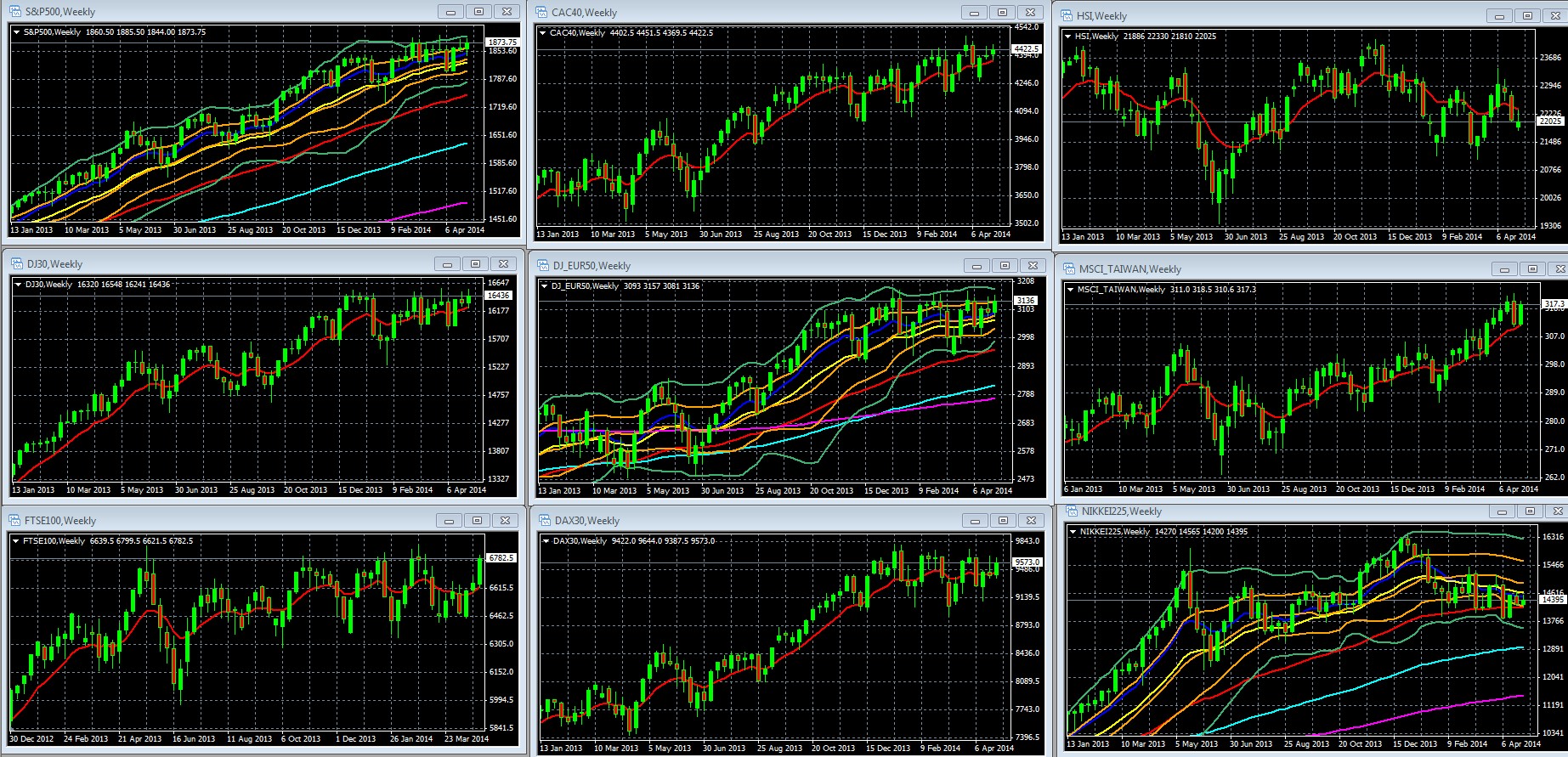

Overall Risk Appetite Per Weekly Charts Of Leading Global Stock Indexes

Weekly Charts Of Large Cap Global Indexes With 10 Week/200 Day EMA [DATES] In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

Key For S&P 500, DJ EUR 50, Nikkei 225 Weekly Chart: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

01 May. 03 21.41

Key Take-Aways: Bullish Momentum Versus Bearish Resistance

US And Europe: Long Term Upward Momentum Intact But Weakening From 12 Weeks’ Flat Range-Trading

- Overall risk appetite per US and European sample indexes show a 3 week uptrend, a 12 week flat trading range, and long term uptrend since at least mid-2012. In other words, short term and long term trends favor more upside.

- This bullishness is confirmed by the S&P 500 and DJ EUR50 weekly charts both closing within their double Bollinger® band buy zones. That suggests that their medium-long term momentum is strong enough for the odds to favor more upside.

- That said, 12 weeks of going nowhere is undermining the long term health of the bull market for the US and Europe

Asian indexes remain a more mixed bag, making it hard to discuss these markets as a whole. Longer term the continued struggles of the two biggest economies, China and Japan, weigh on the rest of Asia, as does the eventual rise in US rates that pressures emerging market currencies and asset markets.

Daily Charts

Looking at the above charts on a daily time frame doesn’t add much insight. Again, we’ve a short term uptrend banging up against resistance that has rebuffed repeated tests, such as the 1890 area for the S&P 500 index.

FUNDAMENTAL PICTURE: Ambivalent Data, Events Driving Ambivalent Trends

State of The Markets

The above technical picture sums up a similar ambivalence in events. It’s not that the past week lacked for top tier data, geopolitical developments, or for surprises in that data. For example:

–US GDP missed badly

–US monthly jobs figures strongly beat expectations – albeit with falling labor participation undermining an otherwise bullish report.

Indeed, as we discuss below, the US jobs report was a microcosm of last week’s results – too mixed to change sentiment and thus driving more range bound horizontal price action.

In sum, we’re still in slow recovery mode in the US, and a slower, uneven recovery at best in the Europe, especially if you pull out Germany. Similarly in Asia, the leading economies of China and Japan continue to struggle, but within expectations.

COMING WEEK LIKELY MARKET MOVERS

Here’s a quick rundown of the likely market movers for the coming week.

12 Week Support & Resistance Levels

Compared to this week’s economic calendar, last week’s calendar had more top-tier events and probably more surprises from them, and it did little to move most global asset markets. We have no right to expect more from this week’s top events, detailed below. The big Fed and ECB events (see below) are also expected to make good watching if you’re an insomniac.

So without fundamental drivers, and the key central banks keeping policy steady, the ACTUAL market movers will likely be recent support and resistance levels. For example, 1890-1800 12 week highs and lows on the S&P 500 would be a decent guide for when US stocks look more likely to bounce or drop. Sadly, that’s only a 5% difference.

Russia-Ukraine Tensions

We continue to believe that in the end, to be blunt, Ukraine just doesn’t matter enough to the West to take serious economic (never mind military) risks, for reasons we discussed in some depth here. Stay tuned for our planned update on that, which we hope to have up this week here, as it’s worth knowing:

–why Ukraine can expect little but symbols and sympathy from the West

–what could yet make this conflict a catalyst for some kind of real war, economic or military, despite all the seemingly rational evidence against that happening

–Guidelines and implications for investors

Top Calendar Events

Here are the events most likely to move most global asset markets. Consult any decent economic calendar for details. Here’s one I like.

Monday

China: HSBC final manufacturing PMI – could be relevant as top tier China data can move overall risk appetite.

US ISM non-manufacturing PMI: Consensus is 54.3 versus March’s 53.1 read, but 4 out the past 5 readings have come in below forecasts.

Tuesday

EU: Spain employment change, services PMI, Italian services PMI, EU retail sales. None are top tier by themselves, but collectively these could be market moving if they all surprise in the same direction.

US: trade balance

Wednesday: Has Potential To Be Big, Probably Won’t

US: Fed Chain Yellin testifies before the Joint Economic Committee of Congress. As noted above, we don’t expect her to say anything that changes market perceptions of Fed policy, given that recent data has not provided a reason to do so, as noted above.

Thursday

China: trade balance

EU: ECB meeting and press conference – more likely than Yellin’s testimony to produce market moving comments, but still expected to be a non-event without surprises. Draghi whining about how the EUR is too high is not news, so we’d be surprised if markets move on his warnings about weakening the EUR unless he actually announces significant new policy moves to do that NOW. Markets don’t expect these until the June statement at earliest.

Friday

China: CPI, PPI (both y/y) – Consensus is for a drop to 2.1% from 2.4% in March. A lower reading would be bearish, suggesting more slowdown than expected.

US: JOLTS jobs openings – has assumed new importance because Yellin believes it’s a key US jobs metric, and after Friday’s confusing report the Fed will be seeking added clarity on US employment and thus whether any policy changes are warranted.

CONCLUSIONS

As noted above in our section on likely market movers, 12 week support and resistance levels are likely to hold, and on the S&P 500 (SPY) they’re only about 5% apart. This is a short term range trader’s market, so if you must buy or sell something, you probably need not wait long until we get near either end of these ranges.

Meanwhile the ongoing debate on whether risk assets like stocks are overpriced remains inconclusive, to the point where even sophisticated investors like those running the California State Teachers’ Retirement System (CalSTRS) struggle to find a place to park funds. See here for more on this rather tepid endorsement of US equities.

For insights on longer term market movers, see our coming post on lessons for the coming week here.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts. For information on a free intro to currencies video course based on my award winning book, see here.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.