The Coming Week’s Must-Know Lessons: State Of Markets, US Jobs, Ukraine, Etc.

What we can & can’t tell about the state of global markets, US employment, & how EU’s failed banking deal is already doing damage

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we cover the key lessons learned for the coming week and beyond.

Summary

–Technical & Fundamental Drivers In Near Term Equilibrium & What’s Likely Sources Of New Trends

–Lessons From The US: State Of US Markets, Employment, & What The Fed Doesn’t Mention About US Jobs

–State Of The Bull Market: Warning On Using Historical Indicators To Time Markets & Examples of Their Use & Misuse

–Lessons From Europe: How The Failed Bank Union Deal Already Coming Back To Haunt EU

Global Markets: Waiting For The Next Big Thing

Both our technical and fundamental analysis of global market drivers shows that bullish and bearish considerations remain in equilibrium.

Technical Outlook: Virtually every global risk asset market we see, be it a major global stock index or currency, remains within a 12 week trading range. Longer term uptrends are intact but can’t get past nearby long term resistance, be it 1890 on the S&P 500, or 1.39 for the EURUSD

Fundamental Outlook: Similarly, each week’s top tier economic data continues to present mixed results that do nothing to change the prevailing consensus about the various big economies that drive global growth. For example:

–In the US, slow recovery.

–In the EU, a patchwork ranging from slow recovery to stagnation

–In China, slowing growth

It’s a “two steps forward 1 step back” theme.

See our posts on the coming week’s market movers and the EURUSD weekly outlook for details.

The short version: Without a material, sustained bullish or bearish change in data from the leading economies, markets are likely to range trade until they get at least one of the following:

- A policy shift from the Fed or ECB

- A sudden geopolitical threat like a real escalation in the exchange of economic sanctions between Russia and the West

- A new bout of EU crisis or other contagion threat

Next, we look at specific lessons learned for the coming week and beyond.

US

Latest On The State Of The Market

Here’s a summary of what we’ve read over the past week

Reasons To Be Bullish: Valuations Can Stay High Longer Than The Current Bull Market

Even if traditional measures say stocks are overvalued, or if stocks have had a huge run higher, that doesn’t mean they’ll go down anytime soon.

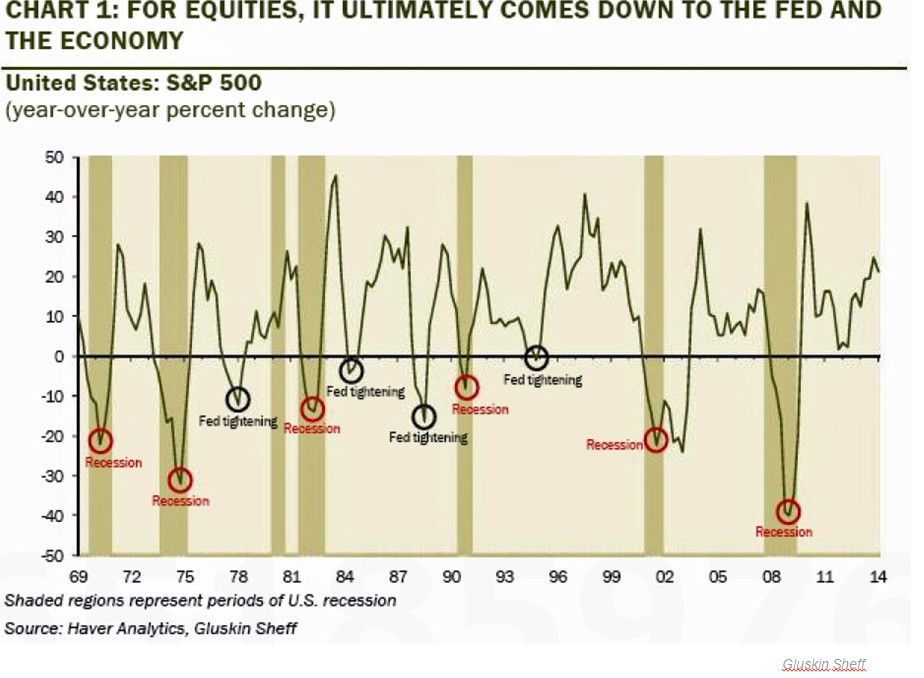

Per a recent research note from Gluskin Sheff’s David Rosenberg, bear markets don’t happen unless we get one or both of the following:

- the Fed over-tightens

- the economy heads into recession

Rosenberg offered this chart showing 12-month returns in the S&P 500 since 1969, showing that market downturns usually come due to recessions (shaded area).

(via Business Insider here)

01 May. 04 18.41

Note also that that 30%-plus rallies over a given 12-months like that seen in 2013, are not uncommon.

The Key To Using Historical Market Timing Indicators: Check Historical Context

The below are two recent bearish indicators. However their bigger lesson is that whenever you see charts of alleged historic stock market crash indicators you (really) need to check the fundamental/historical context.

The indicators themselves are rarely the actual cause of a pullback. Rather, their value is that they provide signal that you may be missing a more logical reason for a coming pullback, and that you need to do some fast investigation to uncover what’s behind these signals and whether it’s a legitimate threat.

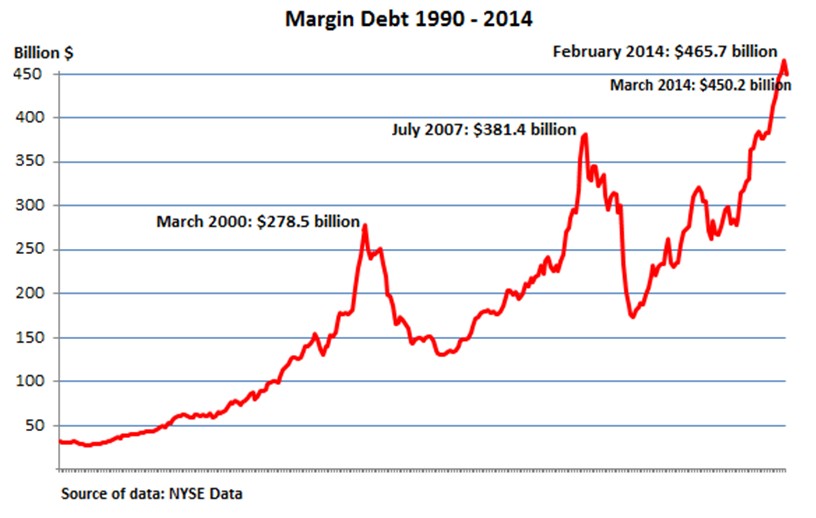

Example 1: Stock Market Margin Debt Reversing Off Record Peak

Wolf Richter points out that the recent reversal of the multi-year all time high in margin debt that began in August 2012, peaked in February 2014, and reversed by $15 bln in March, is a particularly ominous sign. The last 2 times it happened, markets crashed (simultaneously in 2000, after a few months in 2007).

Source: testosteronepit.com here

02 May. 04 18.50

He suggests this reversal in margin debt after a record move higher is the reason for the dive we’ve already seen in momentum stocks, which in the past two crashes were also the first to go in 2000 and 2007. Similarly, he notes another momentum asset class is looking troubled. Six housing markets where prices were soaring mere months ago are showing plunging sales and soaring inventories. See here for details.

Just looking at March 2007, this was a worthwhile indicator because if you weren’t aware of what was happening with the US sub-prime crisis (it was just starting in earnest) this one might have tipped you off. The Fed could have used the hint. Note how it kept the Fed Funds rate at 5.25% steady through the summer even as the subprime mess was unfolding.

Here’s an excerpt from the St. Louis Fed’s excellent Financial Crisis timeline .

February 27, 2007 | Freddie Mac Press Release

The Federal Home Loan Mortgage Corporation (Freddie Mac) announces that it will no longer buy the most risky subprime mortgages and mortgage-related securities.

April 2007

April 2, 2007 | SEC Filing

New Century Financial Corporation, a leading subprime mortgage lender, files for Chapter 11 bankruptcy protection.

June 2007

June 1, 2007 | Congressional Testimony

Standard and Poor’s and Moody’s Investor Services downgrade over 100 bonds backed by second-lien subprime mortgages.

June 7, 2007

Bear Stearns informs investors that it is suspending redemptions from its High-Grade Structured Credit Strategies Enhanced Leverage Fund.

June 28, 2007 | Federal Reserve Press Release

The Federal Open Market Committee (FOMC) votes to maintain its target for the federal funds rate at 5.25 percent.

July 2007

July 11, 2007 | Standard and Poor’s Ratings Direct

Standard and Poor’s places 612 securities backed by subprime residential mortgages on a credit watch.

July 24, 2007 | SEC Filing

Countrywide Financial Corporation warns of “difficult conditions.”

July 31, 2007 | U.S. Bankruptcy Filing

Bear Stearns liquidates two hedge funds that invested in various types of mortgage-backed securities.

August 2007

August 6, 2007 | SEC Filing

American Home Mortgage Investment Corporation files for Chapter 11 bankruptcy protection.

August 7, 2007 | Federal Reserve Press Release

The FOMC votes to maintain its target for the federal funds rate at 5.25 percent.

August 9, 2007 | BNP Paribas Press Release

BNP Paribas, France’s largest bank, halts redemptions on three investment funds.

August 10, 2007 | Federal Reserve Press Release

The Federal Reserve Board announces that it “will provide reserves as necessary…to promote trading in the federal funds market at rates close to the FOMC’s target rate of 5.25 percent. In current circumstances, depository institutions may experience unusual funding needs because of dislocations in money and credit markets. As always, the discount window is available as a source of funding.”

Example 2: S&P 500 Topping When It’s 20% Above Its 150 Week Moving

Richard Ross, global technical strategist at Auerbach Grayson notes that the last time this happened, in 2011, stocks fell over 20% back to the 150% weekly moving average.

Why I like This: Occurred During Fed Historical Easing

I include this tidbit because unlike other bearish signals, this one last occurred during the recent era of ultra-easy Fed policy and historically low rates. Thus it appears to counter the claim that as long as benchmark rates stay near zero, cash keeps stocks supported.

Why I Don’t: Massive Context Omission

That said, a 20% pullback is not a crash, and the last one didn’t last long.

Most importantly, and this is the thing that most undermines Ross’s argument; the drop was rather clearly driven by a second round of EU crisis fears. Highlights from the period of that pullback from May to September 2011 include:

- Last minute bailouts for Portugal and Greece (after the usual default and contagion threats, political unrest and threats of governments falling before debt deals could be reached, Germany refusing to pay for more bailouts etc.)

- The Greek bailout that included “voluntary” losses inflicted on bondholders yet wasn’t a default. This unprecedented theft deal shook bondholder and stock markets, sending shares and credit ratings of other GIIPS nations and banks tanking, like those of too big to bail/fail Italy, and soon after, Spain.

- Things got so bad that on September 26, US President Obama publicly lost patience with EU inaction and said the EU debt crisis was “scaring the world.” Three days later Germany approved an expanded EU bailout fund, easing market fears enough to stop the downturn.

Worth Noting

Given that nasty bout of EU crisis, and general inexperience with how to handle it, this particular overbought indicator can’t be taken that seriously as it fails to consider the very exceptional fundamental context.

What we can say is that when markets are topping and are 20% over their 150 week EMA, they are especially vulnerable. However in time of historically low rates, even a threatened contagion risk was well contained.

Key Point

Again, view these timing indicators as mere warnings that something may be developing. We don’t time our entries and exits based on them; however we would use them as signals to investigate the underlying problem that may be causing the smart money to exit.

US Jobs Picture & What The Fed Should Emphasize But Doesn’t

As we discussed in some depth here, an otherwise very bullish set of April US jobs reports was undermined by 2 things.

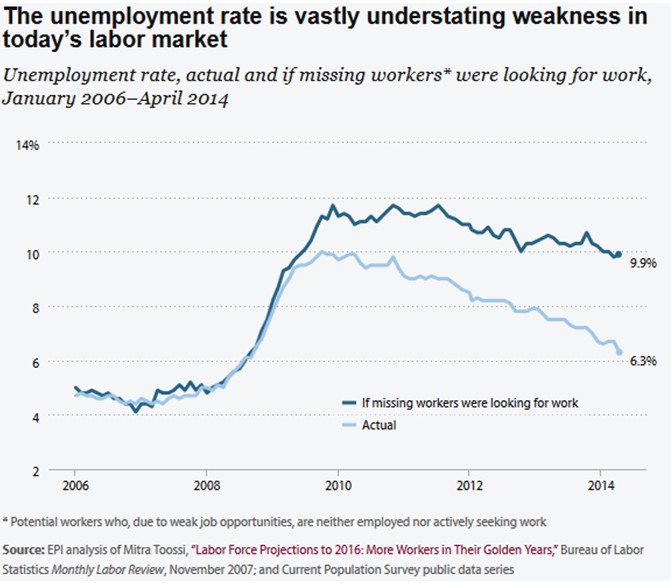

- The labor force participation rate (LFPR), which fell to its lowest level since 1978, suggesting that the drop in the unemployment rate was due mostly to longer term unemployed no longer looking and thus no longer counted in the unemployment rate calculation.

Per Dan Crawford of the Economic Policy Institute , the headline unemployment rate heavily understates true unemployment, saying if the LFPR were more stable, the unemployment rate would be much higher, closer to 9.9%. Still, the U-6 rate (more inclusive of those discouraged dropouts) also fell along with all other alternative measures of labor underutilization.

Source: Dan Crawford (via Business Insider)

06 May. 02 17.02

- Wages remained stagnant. Although the Fed is believed to be focused on the numbers of jobs and percentage of job seekers employed, we have not heard much about how the fed weighs wages and income in its policy planning. That doesn’t make sense considering that consumer spending is about 70% of GDP. For growth to recover, spending has to recover. For spending to recover, incomes have to recover.

However it’s well known that a key feature of the current recovery is that most of the new jobs don’t pay as well as old ones did. The employed are making as much as they did before the financial crisis. For example:

The National Employment Law Project (NELP), via George Magnus, reports that from February 2010 to 2014, most of the job growth is in lower-wage industries.

There are 1.85 million more jobs in lower-wage industries now than before the recession, and two million fewer jobs in the mid and higher-wage industries than before the recession. See here for the details of the report. Highlights include:

- “Lower-wage industries constituted 22 percent of recession losses, but 44 percent of recovery growth.

- Mid-wage industries constituted 37 percent of recession losses, but only 26 percent of recovery growth.

- Higher-wage industries constituted 41 percent of recession losses, and 30 percent of recovery growth.”

See here for further details.

Key Points About US Employment

–It’s still unclear:

—- How much slack remains in the labor force, see here for details

—- Whether Fed policy can do anything about it, see our special report here for details

–Even if the number of jobs and real employment rates recover, the recovery will be limited to the extent that real wages don’t recover too. If wages and incomes stay flat, the recovery is likely to remain weak due to lack of domestic spending.

EU

Failed Bank Union Deal Undermining Coming Stress Tests, EU Banking’s Credibility, Stability

In our past posts we’ve repeatedly warned readers of the dangers of the EU’s failure to agree on a credible banking union. Chief among these is that they would make planned rigorous ECB bank stress tests impossible because if the EU has no credible way of closing or healing undercapitalized banks. That leaves the ECB with yet another set of bad choices (we already discussed its limited options for fighting deflation in our weekly EURUSD outlook):

- Keep standards rigorous and avoid a bigger problem later, at a cost of risking a market panic now because the EU has no bank safety net in place.

- Lower standards yet again, maintaining calm at the cost of undermining EU banking’s credibility from yet another set of unrealistically light stress tests, and of risking a bigger banking blowup if a downturn destabilizes enough banks to again scare markets into a new EU crisis.

Last week the European Banking Authority (EBA) released its stress test methodology. As expected they chose #2. As ft.com reported here (We’d prefer to be compared with our previous attempts, thanks very much), Citi mocked the EBA’s standards compared to those of the US. Morgan Stanley also found the EBA’s tests wanting compared to those of the UK.

In short, EU banking remains a ticking bomb strapped to the EU’s chest, and keeps the threat of another EU banking crisis and contagion threat very much alive and well.

Of course that day of reckoning could be years away, or perhaps never arrive, if the ECB is allowed to print Euros as needed.

However this continued failure to provide meaningful guarantees for EU banks, (and thus to prevent a potential crisis from becoming reality as bank depositors, lenders, and shareholders from flee at the first signs of trouble), has more immediate ramifications.

Ukraine Crisis Unlikely To Threaten Markets

As we discussed in our special report: Fools Russian: 1 Chart Shows How To Play Russia Tension-Related Selloffs, Europe’s dependence on Russian energy and trade virtually assures that it will offer Ukraine little support beyond acts that are mere symbols and sympathy. Otherwise, it’s business as usual.

If you weren’t convinced, consider the combination of EU banking’s

- Lack of a credible safety net to preserve bank system stability (or at least confidence in it)

- Unknown number of weak banks that “passed” the stress tests and are now the ECB’s official responsibility in 2015

- Exposure to Russia, which means any serious sanctions risk a Russian counter move aimed at EU banks.

Stay tuned for a coming update to the above “Fools Russian” post for more on the range of Ukraine sanction risks and ramifications for investors.

Conclusions

—Technical & Fundamental Drivers In Near Term Equilibrium & What’s Likely Sources Of New Trends. Meanwhile, global equities, currency, and other markets are range bound within support and resistance of the past 12 weeks. This levels are useful for those with relatively short holding periods.

—Lessons From The US: State Of US Markets, Employment, & What The Fed Doesn’t Mention About US Jobs. We hear little mention of how it weighs income growth, and that is disturbing for a consumer spending-based economy

—State Of The Bull Market: A Warning On Using Historical Indicators To Time Markets & Examples of Their Use & Misuse. Don’t view these as signals to open or close positions, but rather to investigate the underlying real change. If you can’t find it, at least take precautions in case the signal still proves correct.

—Lessons From Europe: How The Failed Bank Union Deal Already Coming Back To Haunt EU, & Ramifications for Ukraine

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts. For information on a free intro to currencies video course based on my award winning book, see here.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.