The Coming Week’s Top Lessons, Drivers, Things To Watch

How bullish and bearish forces align for stock indexes, forex and other global markets, both technical and fundamental outlooks, likely top market movers

Summary

–TECHNICAL OUTLOOK: Bullish But Weakening Momentum Versus Entrenched resistance cap upside, tempt tests of support

–FUNDAMENTAL OUTLOOK: Likely to see more of the same and what might actually change prevailing trends

–BIGGEST QUESTIONS: Geopolitical dramas threaten short term volatility, but not more

–WHAT TO WATCH: moderate calendar risk, two similar geopolitical tensions, etc.

TECHNICAL PICTURE

We look at the technical picture first for a number of reasons, including:

Chart Don’t Lie: Dramatic headlines and dominant news themes don’t necessarily move markets. Price action is critical for understanding what events and developments are and are not actually driving markets. There’s nothing like flat or trendless price action to tell you to discount seemingly dramatic headlines – or to get you thinking about why a given risk is not being priced in

Support, resistance, and momentum indicators also move markets, especially in the absence of surprises from top tier news and economic reports. For example, repeated failures to break through resistance tempt profit taking and so make markets more vulnerable to sell-offs.

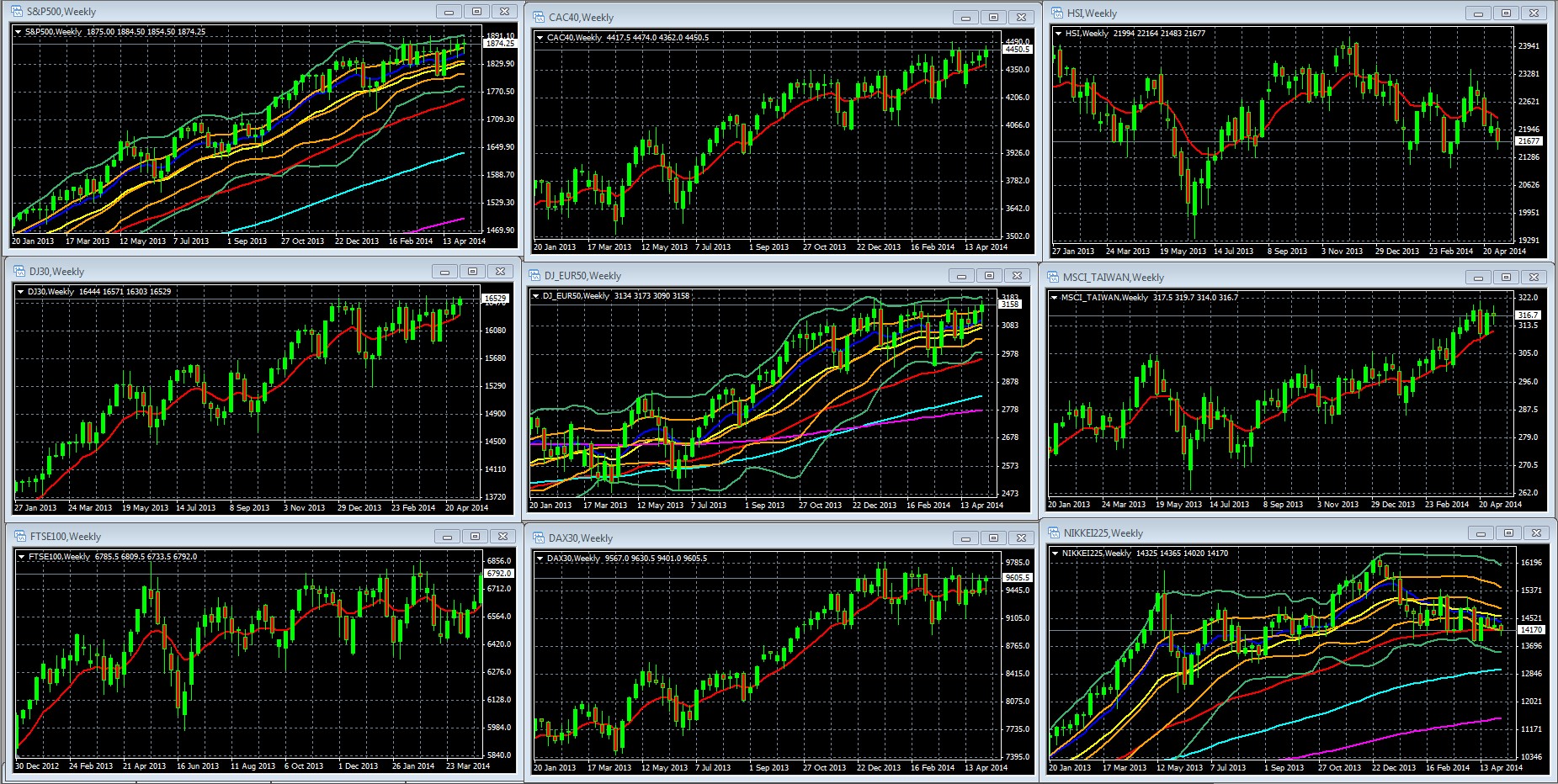

Overall Risk Appetite Medium Term Per Weekly Charts Of Leading Global Stock Indexes

Weekly Charts Of Large Cap Global Indexes With 10 Week/200 Day EMA [DATES] In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

Key For S&P 500, DJ EUR 50, Nikkei 225 Weekly Charts: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

01 May. 11 11.06

Key Take-Aways: Continued Bullish But Weakening Momentum Versus Bearish Resistance

US And Europe: Long Term Upward Momentum Intact But Weakening From 13 Weeks’ Flat Range-Trading

- Overall risk appetite per US and European sample indexes show a 4 week uptrend, a 13 week flat trading range, and long term uptrend since at least mid-2012. In other words, short term and long term trends favor more upside.

- This bullishness is confirmed by the S&P 500 and DJ EUR50 weekly charts both closing within their double Bollinger® band buy zones. That suggests that their medium-long term momentum is strong enough for the odds to favor more upside.

- That said, signs of weakening in the long term uptrend continue to build

o 13 weeks of going nowhere is undermining upward momentum for the US and Europe.

o Virtually our entire sample US and European charts show bearish doji or “hanging man” candlestick patterns, suggesting indecision. Granted, these are not decisive by themselves, as we’ve seen a lot of those in recent months without any serious pullbacks.

Asian indexes remain a more mixed bag, making it hard to discuss these markets as a whole. Longer term the continued struggles of the two biggest economies, China and Japan, weigh on the rest of Asia, as does the eventual rise in US rates that pressures emerging market currencies and asset markets.

Daily Charts: Short Term Neutral Outlook

As those weekly charts’ indecisive doji and hanging man candles suggest, the daily charts show our sample US and European indexes in flat trading ranges.

FUNDAMENTAL PICTURE

Here’s a rundown of the bullish and bearish lessons that actually matter for the coming week. There’s nothing all that dramatic here, but enough that’s worth watching.

Bullish

Despite Weak GDP, Other Data Backs Fed Optimism On US Recovery

As Jeff Reeves wrote this past week here, recent data on US jobs, consumer spending, durable goods, consumer sentiment, manufacturing, capital spending, and merger activity all confirm the slow but steady recovery in the US, and support the Fed’s optimism behind its continued unwinding of QE.

Slow Growth With Low Interest Rates Continues

While a slow recovery isn’t as encouraging as a robust one, as recent years have shown, stocks and other risk assets can rise with only tepid growth as long as rates stay low. That recipe appears set to continue for the coming year if not longer. Fed Chair Yellen’s testimony to Congress last week revealed that until the US sees a much stronger recovery, interest rates will remain low.

Indeed this “goldilocks” data, not too hot to raise fears of rising rates, not too slow to raise fears of recession, along with continued low rates, has been the key to the bull market that began in March of 2009. The other key ingredient has of course been calm on the EU crisis. Like the specter of rising rates, that too is due to come eventually, but it’s nowhere on the horizon for now.

Bullish Thoughts From The Smart Money

Here are some bullish tidbits taken from 19th annual Sohn Investment Conference, one of the leading hedge fund gatherings where the supposedly smartest (OK, at least best paid – also an achievement) money managers share their biggest investing ideas.

- Tiger Cub Fund’s Phillipe Laffont’s big idea is that households will soon need to upgrade their broadband, which makes him bullish on Liberty Global (LBTYA) over the next 5 years.

- Larry Robbins (84% return in 2013) likes sees America’s aging as a big plus for HMOs, particularly Humana (HUM), Wellpoint (WLP) and, pressure on global food supplies as a boon for chemical/agricultural biotech giant Monsanto, given the need to get more production out of limited land and water resources.

- Bill Ackerman of Pershing Square Capital Management likes Fannie Mae and Freddie Mac because banks unlikely to provide meaningful mortgage investments, leaving small competition and large opportunity for the two big government mortgage providers to benefit from most new mortgages.

Bearish

Bearish Thoughts From The Smart Money

Here are some bearish morsels from the above mentioned 19th annual Sohn Investment Conference.

- We’ve mediocre growth globally, in Europe, and slowing in China, with real GDP, industrial investments, and exports all falling. China has a large portfolio of non-performing loans of unknown magnitude but possibly large enough to further threaten its economy, a currency devaluation, and a new round of government stimulus (hey, that’s usually bullish in the short-medium term at least).

- Jeff Gundlach is down on the US housing recovery.

o Housing starts still low

o Last year’s minor rise in mortgage rates killed home sales, suggesting housing affordability still a problem, as stagnant incomes, high unemployment for recent college grads, who are burdened with student loan debt, delays new household formation and first time home purchases.

Fed Chair Yellin Optimistic But Concerned About Housing

Mr. Gundlach isn’t alone on his bearish view of US housing. When presenting her economic outlook to the Joint Economic Committee, the big news was her concern about the housing recovery.

One cautionary note, though, is that readings on housing activity—a sector that has been recovering since 2011—have remained disappointing so far this year and will bear watching … the recent flattening out in housing activity could prove more protracted than currently expected rather than resuming its earlier pace of recovery …

These indicate that she thinks housing sector weakness was not primarily weather related.

Neutral – Bullish Or Bearish Depending On Your Position

US Stocks Offering Better Risk Adjusted Return?

Jeff Kleintop of LPL Financial wrote last week that although Q2 earnings season will only reach the halfway point this week for Europe and Japan, results thus far show US stocks outperforming in terms of:

- The percentage of firms beating analyst expectations: 68% for Q2 2014 versus 66% of the past four quarters and their long term average beat rate of 63%

- EPS Growth Rates: 4.5% annualized for the US versus 1.6% for Japan and declining earnings from a year ago for Europe.

- Forward Guidance: Analysts have cut y/y earnings growth estimates for US firms for Q2 2014 2% since the start of the year versus 7% to 10% for Europe and Japan, with more cuts expected, and sharp reductions from the 17% earnings growth estimates for 2014.If earnings expectations do in fact continue to decline, those forward valuations must rise because the price is then divided by lower earnings.

In other words, as valuations rise, the supposed discount of European and Japanese markets to the US falls or disappears.

This matters not only for stocks, but for currency markets, as the supposed valuation advantage for European and Japanese stocks has been a primary source of EUR and JPY demand.

See our EURUSD weekly outlook for further details. We note that not only is the ECB expected to take new easing steps that should lower the EUR, but also that France has indicated it would like to see longer term steps to drive the EUR lower.

We would add that US equities and bonds offer another significant advantage that stock analysts don’t mention. Over the longer term, US assets are likely to benefit from a rising US dollar, at least relative to European and Japanese assets.

- The Japanese government is openly trying to devalue the Yen far below its current value.

- The EU remains a deeply flawed currency union that lacks most of the basic characteristics of a successful currency union, such as a reliable mechanism to transfer funds to weaker areas, as well as a smoothly functioning central bank authority that can guarantee confidence in its banking system. Its recent attempt at a banking union is a failure. Recognizing this, the ECB has been lowering standards for its coming bank stress tests.As ft.com reported here (We’d prefer to be compared with our previous attempts, thanks very much), Citi mocked the EBA’s standards compared to those of the US. Morgan Stanley also found the EBA’s tests wanting compared to those of the UK.

As our regular readers know, we believe it’s unwise for US investors to have all of their wealth in USD denominated assets. That said, it is a far graver error for Euro-zone and Japanese investors to not have substantial portions of their wealth insulated from EUR and JPY weakness. We discuss a variety of simple ways investors can hedge currency risk here, even if they never trade currency markets.

Biggest Questions And What To Watch

Results And Market Reaction To Pro-Russian Ukraine Secession Vote

Even Putin wanted the voting postponed, but separatist rebels refused. It remains unclear how this specific event will play out, though we’re skeptical about whether it will have any enduring effects on global markets, despite the potential for near term volatility and headlines this week and in coming weeks. We’ll give our take in our coming update on the Ukraine crisis and its implications for markets here. Stay tuned.

South China Sea: China Versus Everyone Else

This is an Asian version of the Ukraine crisis, good for some headlines but unlikely to move markets much, and for the same reasons.

No one wants to risk trade with the bully, including the bullied nations.

The areas in dispute are not vital strategic assets to anybody.

ECB Easing Watch

With ECB President Draghi’s indicating the ECB could ease in June, top tier EU data, particularly regarding inflation, will take on added importance in the coming weeks.

Top Calendar Events To Watch

We’ve a medium-to-low level of event risk that’s common for the third week of the month, which is usually a bit of a let-down after the more packed first 2 weeks. Key events most likely to move the EURUSD include:

- China industrial production – because top tier China data can move the pair by moving overall risk appetite

- US retail sales

- Inflation and GDP data in Europe, as these directly influence how ECB easing decisions in June.

Here’s a full detail of key EURUSD events this week.

Monday: Nothing big scheduled, so we expect preliminary reactions to the Ukraine separatists’ vote and various reactions to grab attention, though it’s unclear if markets will actually pay much attention.

Tuesday

China

Industrial production y/y, fixed asset investment ytd/y, Retails sales: Only industrial production is a top tier event, but taken together these could boost or batter risk appetite depending on whether they all surprise to the upside or downside.

EU

German ZEW survey, EU ZEW survey, Italian 10 year bond auction

US

Retail sales, import prices, business inventory

Wednesday

EU

German, French final CPI

US

PPI, mortgage delinquencies

Thursday

EU

French, German preliminary GDP q/q, EU CPI y/y, EU flash GDP q/q: Together give us a major update on growth in the EU core, EU inflation (so important for gauging the chances and extent of ECB easing in June)

US

CPI, empire state manufacturing, TIC long term purchases, capacity utilization rates, industrial production, Philly Fed manufacturing index

Friday

US- Yellen speaks, building permits, housing starts. Preliminary UoM consumer sentiment: No surprises expected from Yellen, but a big day for housing data, about which she expressed concern in last week’s congressional testimony on the US economic outlook. Therefore if housing beats or misses expectations, it could influence market sentiment about Fed tightening, the thing that really matters.

CONCLUSIONS

On the surface, little reason to expect stocks and other risk assets to move higher. Growth is mixed, resistance looks strong. That said, interest rates remain low, so yield seekers still have few options. Thus downward potential looks limited to normal bull market pullbacks.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts. For information on a free intro to currencies video course based on my award winning book, see here.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.