EURUSD Weekly Outlook: Has The Big Reversal Started? Here’s What To Watch

FX Traders’ weekly EURUSD fundamental & technical picture, this week’s market drivers that could change it- the bullish, the bearish and likely EURUSD direction

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we cover outlooks for the major pairs for the coming week and beyond.

Summary

- Technical Outlook: Medium term per weekly EURUSD charts neutral, short term bearish. Deeper tests of support likely this week but need close below 1.35 before calling this a topping out

- Fundamental Outlook: Neutral near and medium term, as bullish, bearish forces remain in equilibrium. Bearish longer term due to expected divergence in direction of Fed and ECB policy, economic performance

- Last week’s only meaningful price mover was the ECB’s hint of June easing. Yellen’s dovish remarks were ignored as the pair actually fell that day

- Longer Term Game Changer 1: A spike in US 30 year T-bond rates bears watching. If it becomes a trend, that would be a game changer as the USD has been undermined by persistent low rates

- Longer Term Game Changer 2: Markets stop seeing European stocks, bonds as better value than those of US, undermining EUR demand

TECHNICAL OUTLOOK

First we look at overall risk appetite as portrayed by our sample of global indexes, because the EURUSD has been tracking these fairly well recently.

Overall Risk Appetite Per Weekly Charts Of Leading Global Stock Indexes

This week we minimize our usual discussion of overall risk appetite per our sample of leading global stock indexes, because the EURUSD has not been tracking these indexes and overall risk appetite for the past weeks, and it is likely to continue to do so this week, for reasons we’ll discuss below.

We’ll just note that the medium term technical outlook for the US and European indexes per their weekly charts remains bullish, and thus supportive for the pair. The near term outlook per their daily charts is neutral. For the near term that’s irrelevant, as the pair is now moving mostly on its own fundamentals, discussed below.

EURUSD Weekly Technical Outlook: Short Term Bearish, Medium Term Neutral

EURUSD Weekly Chart July 2012 – Present

KEY: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

01 May. 10 22.10

Key Take-Aways Weekly Chart: Deeper Tests Of Support Likely This Week

–Momentum has shifted from bullish to neutral as price is now firmly in the neutral zone of its double Bollinger®bands

–The failed test of 1.40 resistance and key reversal to close near the bottom of its weekly trading range (its lowest in 4 weeks) suggests that the coming week should see a test of deeper support to the 1.37 -1.365 area

–Note how the pair closed back under former support of its long term downtrend line (green) dating back to mid-2008 and 2011, as one can see on a EURUSD monthly chart. We watch for further weekly closes under this new resistance line over the coming weeks to to confirm the long term downtrend.

The weekly EURUSD charts’ picture of medium and long term price action shows weakening upward momentum and resistance holding in the 1.39 area, buttressed by Draghi’s dovish comments from last Thursday’s press conference. Yellen’s remarks Wednesday about recent poor US housing data also had a dovish tinge, but it’s only the ECB that is moving towards further easing.

While the pair remains in its 13 week trading range, the technical bias is towards tests of deeper support around 1.365. If that breaks, the next big support is around 1.36 -1.355, buttressed by triple layers of support

–The green uptrend line dating from mid-2012

–Two Fibonacci retracements:

—-The 50% Fibonacci retracement of the downtrend from mid-2011 to mid-2012.

—-The 38.2% Fibonacci retracement of the bigger downtrend from July 2008 to June 2010

See the EURUSD monthly chart below for context.

.

KEY: 10 Month EMA Dark Blue, 20 Month EMA Yellow, 50 Month EMA Red, 100 MonthEMA Light Blue, 200 Month EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange. Gold Fib retracement lines of downtrend from May 2011- July 2012, White Fib retracement lines of downtrend from July 2008-June 2010.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

02 May. 10 22.36

Although the EURUSD uptrend has flattened out, given that we still have and uptrend (green line) from July 2012, we would not sound the alarm of a forming topping pattern until that line is decisively breached around the 1.35 area.

EURUSD Daily Technical Outlook

For the sake of brevity, we just note that momentum indicators on the daily chart suggest more downtrend ahead. For example, the pair is now firmly in its double Bollinger band sell zone.

FUNDAMENTAL OUTLOOK: THE BALANCE OF BULLISH VS. BEARISH

Summary

Despite the drama and volatility of last week, the equilibrium of the longer term fundamental drivers remains undisturbed by last week’s events. Continued inflows into GIIPS bonds and continued low rates for the USD have supported the pair despite the belief that ultimately the Fed is moving to tighten while the ECB is moving to ease and bring an eventual USD rate advantage.

Looking at the EURUSD’s daily chart, the big news for the pair this past week was Thursday’s ECB rate statement and press conference, where Draghi’s hint of some kind of easing coming at the June meeting, which sent the pair down for its biggest single day loss in over a month.

The pair continued to test lower the rest of the week, added by weak German data that added fuel to ECB easing speculation, as German export weakness should ease German objections to a weaker EUR.

Note however, that Draghi is clearly saying that a decision depends on EU economic data, leaving open the very real chance of no action in June. Therefore anyone seeking to buy Euros should be doing so only to play a short term bounce somewhere in the 1.375-1.355 area, depending on the time frame.

See below for further details of the near term bullish and bearish forces at play.

Bullish

Federal Reserve Board Chair Janet Yellen presented her quarterly economic outlook to the Joint Economic Committee in Washington last Wednesday. Although she generally noted the same emphases on weakness in the labor market and the need to keep rates long for a long time, she added a concern that housing data has been disappointing this year and bears watching.

Markets seized on this change as an excuse to label the remarks dovish and sent stocks higher and benchmark 10 year bonds lower.

In theory this was bullish because it suggests continued long term low rates that keep the USD from gaining ground on the EUR despite the ECB’s expected easing. Although stocks jumped on the news, currency markets ignored it. The pair actually closed lower on the day, and the week, and for good reasons.

In essence, Yellen’s remarks, and recent US housing data, are just short term noise. US housing data in 2014 has been mixed but not bad, and of course much of the recent bad data has been blamed on the temporary effects of harsh winter weather, as well as tight mortgage credit. Both headwinds could become tailwinds as suppressed demand snaps back in coming quarters. Economist Bill McBride of Calculated Risk recently wrote about the positives in housing market data. These include: declines in sales of distressed homes, the percent of homeowners in negative equity, and mortgage delinquencies. Also, mortgage credit is so tight it can only get looser (rates have eased a bit of late).

Although the US jobs market is healing and housing data setbacks have been temporary, ECB easing is a longer term headwind.

Bearish

ECB Press Conference: Ready To Ease?

This was the only real market moving event for the pair, though weak German trade data helped as it suggested the strong EUR is hurting German exports too.

Key points included:

1. ECB Comfortable with Easing in June if Staff Forecasts Continue Same Themes

2. Stronger EUR combined with low inflation is a “serious concern,” the ECB wants weaker EUR IF the deflationary threat remains. (Our note: Does that mean if inflation figures hold steady the ECB does nothing?)

3. Strong EUR caused by inflows

5. In a break with past procedure, the ECB now willing to commit to policy changes in advance

6. Sees Downside Risks to economic outlook from financial, emerging market and geopolitical risks

7. ECB ready to act fast, considering lower rates and also unconventional measures.

8. The longer the period of low inflation, the longer the risk of expectations for more of it that reinforce deflation.

9. Inflation expected to rise in 2015.

11. Data shows moderate recovery proceeding as expected. Prolonged period of low inflation, then prices to rise gradually

If the ECB eases next month, we suspect it does so via a refi rate cut or move to a mildly negative deposit rate, or a combination of these.

Earning Season To Undermine Demand For EU Stocks, EUR?

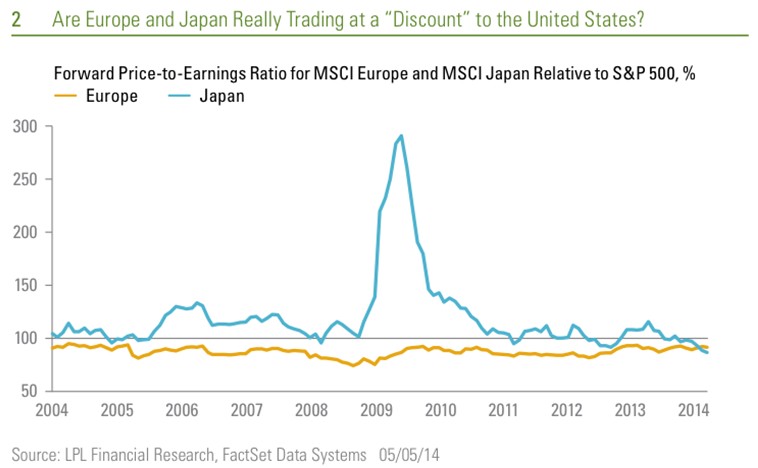

The primary fundamental support for the EUR has been strong demand for EU stocks and bonds, based on the theory that these have been oversold and so are a better value and so offer higher returns, given Europe’s anticipated recovery and the perceived receding risk of a new EU crisis.

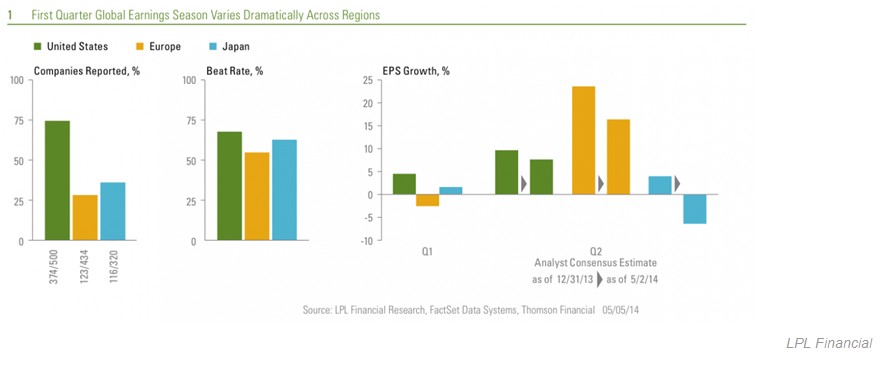

However Jeff Kleintop of LPL Financial wrote last week that although Q2 earnings season will only reach the halfway point this week for Europe and Japan, results thus far show US stocks outperforming in terms of:

The percentage of firms beating analyst expectations: 68% for Q2 2014 versus 66% of the past four quarters and their long term average beat rate of 63%

EPS Growth Rates: 4.5% annualized for the US versus 1.6% for Japan and declining earnings from a year ago for Europe.

Forward Guidance: Analysts have cut y/y earnings growth estimates for US firms for Q2 2014 2% since the start of the year versus 7% to 10% for Europe and Japan, with more cuts expected, and sharp reductions from the 17% earnings growth estimates for 2014.If earnings expectations do in fact continue to decline, those forward valuations must rise because the price is then divided by lower earnings.

In other words, as valuations rise, the supposed “discount” of European and Japanese markets to the US falls or disappears, as would a primary source of EUR and JPY demand.

01 May. 09 16.38

02 May. 09 16.39

France To Push For Weaker EUR

French PM Hollande wants to broaden the ECB’s focus from inflation fighting to lowering the Euro. His motives include:

- Economic weakness has helped bring recent defeats of his Socialist party in local elections.

- His efforts to generate genuine growth like actually lowering taxes and public spending have angered his own Socialist party supporters, who want France’s economy to be more competitive without the pain of actually making it more productive.

- France’s big exporters(Airbus, Sanofi, Lafarge, etc) blame EUR strength for their weak performance, rather than slowdowns in China and Russia, even as Germany and Spain continue to show stronger export performance than France with the same Euro (as noted by France’s own Finance Minister Pierre Moscovici). Germany has also seen its exports suffer of late, but has not advocated a debased EUR as the solution.

Thus after this month’s EU parliamentary elections France intends to push for EU policies to weaken the EUR. Whether or not this is the correct solution, the political pressure alone may well contribute to an ECB decision to announce new easing at its June rate statement and press conference.

Thursday’s 30 Year T-Bond Auction Show Rate Spike

The US Treasury sold $16 billion of 30 year bonds at a yield of 3.440%, which was much higher than the 3.392% forecasted by analysts. The bid-to-cover ratio, a measure of demand, was low at 2.09, the lowest level since August 2011. Analysts were looking for a ratio of closer to 2.36. The USD has been undermined by continued low rates, so if this is the start of the trend, the pair could be topping out.

Biggest Questions And What To Watch

EU Inflation Indicators: Will EU Inflation Improve Enough To Keep ECB Easing On Hold?

Draghi seemed to suggest that if inflation holds steady the ECB could yet again hold off easing. Depending on how much of a rate cut markets price in, an ECB decision to do nothing could send the EUR higher, as similar expectations did just before Draghi mentioned he was comfortable with lowering rates in June.

Consensus On Whether ECB Will Ease, How, And By How Much

At this stage, at least one survey of analysts at major banks shows disagreement about:

- Whether there will be new easing in June, or perhaps a bit later.

- The type of easing the ECB will eventually choose if inflation remains too far below the ECB’s 2% per year target.

We believe that the key variables include:

- Whether or not EU inflation measures show signs of improving before June

- Whether or not the EUR moves drops before then, either due to continued ECB attempts to jawbone the currency lower, or from other causes.

- Whether or not the ECB makes clear that whatever steps it takes are not part of a slow, incremental series of one-time steps followed by months of inaction like the last rate cut in November 2013. If it shows by its actions or concrete promises that it’s committed to a sustained series of steps to raise inflation, then market speculation could help drive the EUR lower.

One thing is clear, whatever steps the ECB takes need to make credit more available to businesses and households in order to speed up the velocity of money. Thus far banks have been reluctant to lend as they hoard capital in advance of coming ECB stress tests.

TOP CALENDAR EVENTS FOR BOTH OVERALL RISK APPETITE AND SPECIFIC TO THE EURUSD

We’ve a medium-to-low level of event risk that’s common for the third week of the month, which is usually a bit of a let-down after the more packed first 2 weeks. Key events most likely to move the EURUSD include:

- China industrial production – because top tier China data can move the pair by moving overall risk appetite

- US retail sales

- Inflation and GDP data in Europe, as these directly influence how ECB easing decisions in June.

Here’s a full detail of key EURUSD events this week.

Monday: Nothing big scheduled, so we expect preliminary reactions to the Ukraine separatists’ vote and various reactions to grab attention, though it’s unclear if markets will actually pay much attention.

Tuesday

China

Industrial production y/y, fixed asset investment ytd/y, Retails sales: Only industrial production is a top tier event, but taken together these could boost or batter risk appetite depending on whether they all surprise to the upside or downside.

EU

German ZEW survey, EU ZEW survey, Italian 10 year bond auction

US

Retail sales, import prices, business inventory

Wednesday

EU

German, French final CPI

US

PPI, mortgage delinquencies

Thursday

EU

French, German preliminary GDP q/q, EU CPI y/y, EU flash GDP q/q: Together give us a major update on growth in the EU core, EU inflation (so important for gauging the chances and extent of ECB easing in June)

US

CPI, empire state manufacturing, TIC long term purchases, capacity utilization rates, industrial production, Philly Fed manufacturing index

Friday

US- Yellen speaks, building permits, housing starts. Preliminary UoM consumer sentiment: No surprises expected from Yellen, but a big day for housing data, about which she expressed concern in last week’s congressional testimony on the US economic outlook. Therefore if housing beats or misses expectations, it could influence market sentiment about Fed tightening, the thing that really matters.

Sample Retail Traders Positioning

Source: Forexfactory.com

03 May. 10 23.13

As the above real time sample of retail traders positioning shows, our group still hasn’t bought the idea of playing the 5 and 12 week trading ranges. From Tuesday on, when the pair was at resistance and thus likely to fall if resistance held, traders did not build up short positions to play the bounce lower.

Instead, they built up long positions all last week, perhaps aided by both dovish Yellen comments and anticipated inaction from the ECB press conference, as well as the rising EURUSD (before Draghi dropped his “ready to ease in June bomb) that looked set to finally break out over resistance.

Even after Draghi’s bombshell announcement, as the pair moved against them, the group continued building long positions in hopes of anticipating the bounce before it happened. As usual, that proved to be a bad idea. It’s better to wait for some kind of trend confirmation before jumping in.

CONCLUSIONS

The upper end (1.40 area) of the 13 week trading range held, so now the question is how deeply will support be tested, with the lower end around 1.365. If we get a decisive sustained move into the 1.365 area, we need to be ready for a test of the deeper support around 1.355, which is buttressed by the uptrend line that began in July 2012 as well as two long term Fibonacci retracements of two long term EURUSD downtrends.

Unless we get some major risk off event, like another Ukraine crisis escalation, we doubt the pair leaves the 1.39 – 1.365 area.

Despite the near term tests of support likely this week, we remind readers that the longer term fundamentals that have kept the pair locked in a trading range remain intact:

Bullish

–Demand for Euros as long as European stocks and bonds continue to be viewed as a better value.

–The stubborn persistence of low US interest rates that prevents the long anticipated USD rate advantage

–Persistent low US inflation that removes any pressure on the Fed to accelerate its tightening

Bearish

–Slow but steady divergence of ECB (easing) and Fed (tightening) limits EURUSD upside, as does

–Continued US outperformance of the EU in economic data and earnings

–The Euro-zone’s “forgotten but not gone” vulnerability to yet another crisis, particularly given its exposure to Russia. Stay tuned for our coming special report on that here later this week.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts. For information on a free intro to currencies video course based on my award winning book, see here.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.