10 REASONS WHY RUSSIA-WEST TRADE CONTINUES AS USUAL & HOW TO PROFIT

An update on why it’s unlikely there will be long term economic impact from the Ukraine crisis and what to do about it

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we share thoughts about key developments worth a special report

There will blood. There will be drama, headlines and some sanctions, mostly diplomatic and symbolic. Business however, will continue as usual for the most part. Here’s why, and some guidelines on profit.

SUMMARY

Asymmetry of Will: Ukraine matters more to Russia than it does to the West, and Putin has more support from the elite, and the street

Even though Russia wants it more, economic costs are unaffordable for both sides

Russia need not invade to win, can avoid provoking serious sanctions that the West doesn’t want to impose anyway

Guidelines for profiting from excessive market fear

1. ASYMMETRY OF POLITICAL WILL AND INTERESTS: Ukraine More Important To Russia Than To West

Putin’s goal of a “Eurasian Union,” that combines ethnic nationalism and the restoration of the FSU’s former territorial hegemony, is both a deeply held ideology and practical political move. Putin has the support of both elites and the street. A late April survey by the independent Levada pollster put his support at 82%, its highest since late 2010. As of May 7th another survey showed similar results, with Putin’s confidence rating at 78.3%. The crisis has reversed his regime’s decline in popularity and sent it surging on hopes of new “Eurasian Union” to restore former Russian power, despite the political and economic risks.

As one of, if not the most important FSU breakaway republics now on Russia’s border, Ukraine is a key strategic asset for Russia. A pro-Western Ukraine represents a tangible potential military threat for Russia, as was a pro-Russian Cuba was for the US.

Putin suspects that the West is behind the protests that toppled former pro-Russian President Yanukovich, and apparently so do his supporters and much of the Russian polity. If so, that belief would justify Russia’s own “counter-meddling.”

In contrast, the West is far less committed to Ukraine.

Politically, the West has no strong ideological commitment to Ukraine to match Putin’s drive to control and expand his borders. Ukraine is not a key strategic asset for the West, as it clearly is for Russia.

Militarily, neither the US nor Europe is willing to go to war over Ukraine, and Ukraine alone cannot win a conventional war against a committed Russian invasion.

Economically, although a sanctions war would be mutually damaging, Europe has shown no serious willingness, to bear the potential pain of such a confrontation.

As we discussed in our first post Fools Russian: 1 Chart Shows How To Play Russia Tension-Related Selloffs, none of Europe’s political or business elites have expressed any appetite for material economic sanctions that would disrupt business as usual.

There are compelling arguments that the West could cripple Russia’s economy, but they’re irrelevant the West’s far lower economic pain threshold.

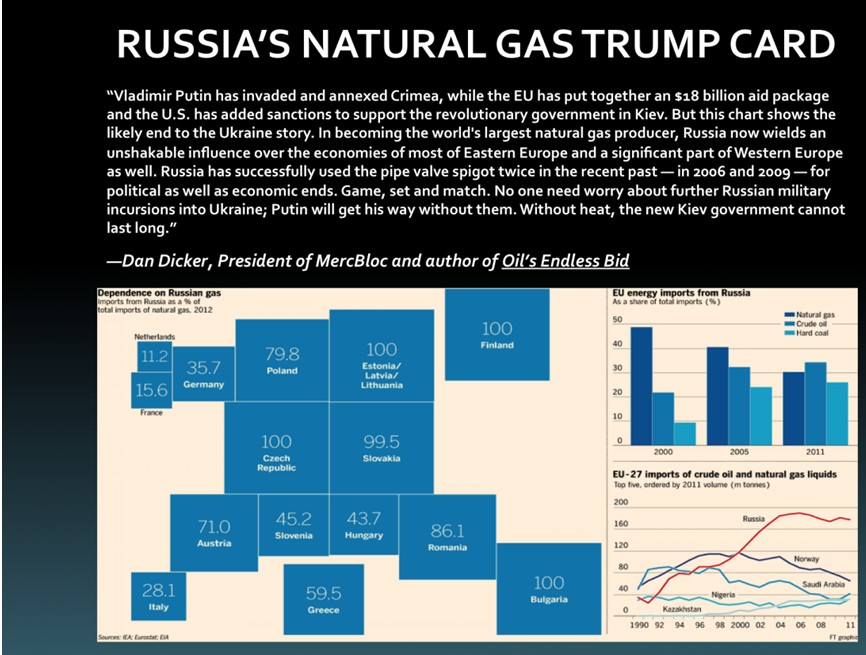

2. EUROPE GAS PAINS: HOOKED ON RUSSIAN ENERGY

Via: Business Insider/Matthew Boesler

06 Apr. 20 04.37

Given the facts in just this one graphic, Europe has every motivation to avoid a sanctions war with Russia.

Lack of Near Term Substitute

Meanwhile, as reported by ft.com here, at least one potential US gas exporter CEO has dismissed America’s capacity to replace Russian energy was “nonsense” and that no more than eight out of over 20 proposed rival export projects were “real”.

Note how the above graphic shows Germany and France relatively less vulnerable to Russian energy cutoffs. That hasn’t made them any less ambivalent about imposing sanctions. Note the following.

3. EUROPE’S BUSINESS LEADERS RESISTING SANCTIONS

The most recent round of sanctions show that EU leaders business and political leaders remain opposed to imposing any material sanctions that would materially interfere with business as usual.

For example, the Wall Street Journal reported last week that large German firms like Siemens and BASF are resisting further economic sanctions. “As the Ukraine crisis has worsened, German officials have faced a barrage of telephone calls from senior corporate executives, urging them not to take steps that would damage business interests in Russia, people familiar with the matter say.” (Via businessinider.com here).

Of course they’re far from alone. Energy firms such BP and Eni are reminding a variety of government officials that Europe can’t replace Russian energy. BP owns 20% in Russian oil giant Rosneft.

Britain and Cyprus both have opposed sanctions that might limit their financial sectors’ considerable dealings with Russia.

US business lobbies are working to discourage Washington from introducing sanctions that might lead to retaliation against US interests. The US has expressed caution about getting too far ahead of the EU in its sanctions. Given the EU’s foot-dragging, that means no serious sanctions are likely.

4. EUROPE BANK VULNERABILITY TO RUSSIAN DEFAULT: LEAD BY FRANCE

Here’s where things get really dangerous, because if markets even suspect that, just maybe, the global contagion-prone banking systems might be in the crosshairs, even central banks may be challenged to maintain calm.

As we wrote last week here, the EU’s banking union pact is so flawed that the ECB’s coming stress tests are being steadily watered down because it knows there is no bank safety net to calm markets given the number of troubled banks it expects to uncover if it uses the rigorous standards that it was promising just a few months ago.

Russia has nearly $700 billion is owed by banks and corporations, with European banks having about $150 bln in Russian exposure, and much of that is with banks in key EZ banking systems that, as ECB actions noted above indicate, are already vulnerable to defaults and related contagion risks.

(Via zerohedge.com)

05 May. 07 18.31

Note that France’s $50 billion exposure is on a similar scale to the $70 billion exposure it had to Greece in 2010, when French President Sarkozy was so scared of the contagion risk to French banks that he successfully pressured Germany to support a Greek bailout. Back then, France was able to take advantage of the ECB’s Securities Market Program (SMP) to dump Greek bonds, thus mutualizing their Greek exposures across the Eurozone.

Can France, or anyone else, depend on the ECB providing another such program for Russian debt?

As zerohedge.com notes here, much of French banks’ Russian exposure is illiquid, “such as Société Générale’s ownership of Rosbank, Russia’s 9th largest bank by net-asset value ($22 billion).”

Even at this early stage of mostly symbolic sanctions, the bank is already feeling the pain. As ft.com reported on May 7, companies with significant Russian operations are already reporting damage to their bottom lines. For example, Société Générale reported a €525m hit to its balance sheet from writing off the goodwill of its Russian assets. It blamed the economic downturn, the falling ruble and operating uncertainty, which dragged its quarterly profits down 13%.

If Russia feels threatened enough, it need not even default on its loans. It need only threaten to default on some of them. Which ones? Who cares? The mere hint of hidden default threats can be enough to freeze up interbank lending. Remember the sub-prime crisis?

What could make Russia feel threatened enough to threaten a new EU crisis? A Western threat of a new Russian financial crisis could, of course. The West has even more weapons of economic warfare than Russia.

5. RUSSIA UNLIKELY TO PUSH WEST FAR ENOUGH TO RISK MEANINGFUL SANCTIONS

Mr. Putin’s likely goal is the one both he and the Russian foreign ministry have outlined repeatedly since February: the federalization of Ukraine, a strategy aimed at weakening the central government in Kiev as large portions of the country fall under Moscow’s influence. In other words, Putin’s primary goal is to prevent as much of Ukraine as possible from falling into the West’s sphere of influence and avoid a pro-NATO nation on his South Eastern border.

Putin can achieve that goal without the serious military intervention that could provoke meaningful limits on West-Russia trade, even if the West had the will to impose them.

Even if Putin would consider more provocative actions, he has plenty of reasons to avoid risking serious economic sanctions.

Russia Has Reason To Fear Serious Western Sanctions

Although the West doesn’t have the same willingness as Russia to absorb real economic pain, it still has enough more than enough financial weapons to worry Russia, especially given Russia’s own economic vulnerabilities.

6. Russia Is Hooked On European Gas Revenues

Any pain inflicted from energy cutoffs will flow both ways, because about 80% of Russian gas exports come from sales to the EU alone, and Russia doesn’t have many other gas export alternatives in the near term. Oil and gas sales together fund about 50% of Russia’s budget.

7. Russia Is Hooked On Western Credit

Just as Europe is Russia’s energy junkie, so too is Russia the West’s credit junkie.

Since the Ukraine crisis erupted, Russia’s private companies have been shut out of global capital markets, and may soon be dependent on state aid to survive. The Telegraph recently reported that

“‘No Eurobonds have been rolled over for six weeks. This cannot continue for long and is becoming a massive issue,’ said an official from a major Russian bank. ‘Companies have to roll over $10bn a month and nothing is moving. The markets have been remarkably relaxed about this, given how dangerous it is. Russia’s greatest vulnerability is the bond market,’ he said.

That credit crunch, and the instability it threatens, has caused capital outflows of over $65 bln thus far, risking a repeat of the capital flight and credit squeeze for Russia similar to that seen globally in 2008.

Of course in theory China or other BRIC or neutral nations could provide fill Russia’s credit gap.

8. America’s “Nuclear” Option In The Sanctions War To Cut Off Credit To Russia

Here’s why they haven’t, and won’t.

In addition to the range of normal sanctions, the US has a special nuclear option. As The Telegraph’s Ambrose Evans-Pritchard reported here, an elite cell at the US Treasury has constructed a financial nuclear weapon designed to put an enemy nation under economic siege until it surrenders under threat of financial starvation.

The weapon is an official accusation against a specific financial institution of money-laundering or underwriting terrorist activities, a conveniently vague offence. Under Section 311 of the US Patriot Act, any bank that wants to do business with the US or US businesses abroad, even if it has no operations in the US, must sever all dealings with the accused bank.

The strategy rests on America’s dominance over the global banking system, reinforced by a network of allies and the reluctant acquiescence of neutral states. It’s already been used successfully over the past 12 years against Ukraine (of all places) to shut down Russian organized crime operations there. It has also been used to cut North Korean terror support (as Chinese and other banks stepped away) and to bring Iran negotiate a nuclear deal. Quoting a former key Treasury official and expert on this kind of financial warfare Pritchard writes:

“This would be a calibrated escalation, issuing the scarlet letter to Russian banks that help Syria’s regime…’If the US Treasury says three Russian banks are “primary money-laundering concerns”, do you think that UBS, or Standard Chartered will have anything to do with them?’

This will graduate to sanctions on Russian defence firms, mineral exports and energy – trying not to hurt BP assets in Russia too much…culminating in a squeeze on Gazprom should all else fail. Whether you are for or against such action, be under no illusion as to what it means. We would be living in a different world, and Wall Street’s S&P 500 would not be trading anywhere near 1,850.”

He also notes that Putin cannot necessarily count on global allies, given that his only supporters at the UN over Crimea were a club of economic nobodies: Venezuela, Bolivia, Cuba, Nicaragua, Belarus, North Korean, Syria, Sudan, Zimbabwe and Armenia.

The threat of this weapon has in the past brought cooperation from China and other economies that might have the needed size to fill the Western credit vacuum.

Washington is forcing the pace of Russia’s credit siege, using this regulatory weapon to force banks across the world to pull back from Russia. The US said Russian operations in six Ukrainian cities involve well-trained units in bullet-proof vests and olive-green uniforms without insignia, constituting an assault on the country. In other words, the US is framing its accusations in language used to impose a ban on banks dealing with Russia.

9. Forget The Marines, US Sending In The IRS

Who needs the leather-necks when you can send in the “pencil-necks?”

Back in 2010, Congress passed the FACTA (Foreign Account Tax Compliance Act), a law to prevent the use of overseas accounts for tax evasion. Starting in July, U.S. banks will be required to withhold 30 percent tax on certain payments to financial institutions in other countries that have not signed agreements to share information about U.S. account holders with the IRS. The withholding applies mainly to investment income.

Russia, along with dozens of other nations has been negotiating information-sharing agreements with the U.S. in order to avoid these harsh penalties.

However in March, after Russia annexed Crimea and was seen as stoking separatist movements in eastern Ukraine, the Treasury Department suspended negotiations. With the July 1 deadline approaching, Russian banks are now concerned that the price of investing in the United States is about to go up. A lot.

After July 1st, Russian banks that buy U.S. securities will forfeit 30% of the interest and dividend payments on virtually all stocks and bonds, including U.S. Treasuries, including most stocks that were bought before that date.

Private investors using Russian financial institutions for these securities trades also face the withholding penalty. Those private investors could later apply to the IRS for refunds, but the inconvenience, and thus manpower costs involved, would be enormous.

Added to Russian bank credit troubles described above, Russian banks become far less competitive.

Unlike current sanctions, FACTA applies not just selected Putin associates and oligarchs, but to everyone, from Gazprom on down. See here for full details

In order to “encourage” compliance, U.S. banks that fail to withhold the tax will be liable for it themselves. Recently, the Treasury Department issued guidance saying it will give U.S. banks a temporary reprieve. As long as U.S. banks make a good-faith effort to withhold the proper tax, they won’t be liable for mistakes until 2016.

Russian banks face another hurdle: an expired deadline to make a deal with the IRS and avoid the withholding and need to claim refunds. In June, the Treasury Department will release a list of foreign banks that are exempt from withholding. If a bank isn’t on the list, U.S. banks are required to start withholding 30 percent of your payments in July.

The deadline for getting on the list was Monday May 5th, mere weeks after the U.S. and Russia suspended negotiations.

10.OTHER DAMAGE TO RUSSIA’S ECONOMY

There are of course other sources of economic damage that are already well known. These include capital flight from Russian banks, the falling ruble, rising interest rates, Russian business loses from Ukraine exposure, and reduced investment on projected slowing growth, possibly as low as 0% this year.

The combination of Western economic weapons and Russian economic vulnerability should limit Putin’s actions so that this crisis probably ends in one of the stalemate scenarios described below.

The most likely variations on that theme include:

- The May 25th elections bring in a pro-EU/Western president and government. This would be the logical follow up on the original drive for reforms to improve the economy and tackle corruption that inspired the overthrow of the former pro-Russian regime. Russia avoids an invasion of eastern Ukraine, but remains hostile imposing some degree of trade and other economic sanctions. Economic growth is slow, hampered by Russian sanctions, a heavy foreign debt burden, and foreign direct investment limited until the political situation is stable. Tensions between ethnic Ukrainian and Russians remain high. Again however, remember that Putin is far more interested in keeping the West out of Ukraine than conquering Ukraine.

- Depending on a variety of factors, it’s conceivable that pro-Russian administration could win. That might actually lead to greater long-term stability by appeasing Russia and thus removing the immediate cause of destabilization in the east. However, this would likely mean an end to the drive for economic and anti-corruption reforms. In this less probable scenario, Ukraine would return to its former bias towards maintaining close economic ties with Russia, while keeping its more viable of its economic connections with the EU.

In sum, for all the potential drama to come, Russia will be careful not to provoke meaningful economic sanctions, and will have some wiggle room given the West’s extreme reluctance to impose them.

GUIDELINES FOR HOW TO PROFIT FROM UKRAINE TENSION SELLOFFS

That means that anything that sells off on Ukraine tensions is a possible bargain, and anything that soars higher could be an interesting short position play. These are classic applications of Warren Buffett’s rule: “Be fearful when others are greedy and greedy only when others are fearful.” The key qualification is that one may need patience to allow time for the dust to settle, fears to ease, and for any of the above mentioned FACTA related threats or actual sanctions ease off.

Long The Russian Ruble (RUB)

The mere threat of Russian isolation has already got the Ruble falling hard in 2014

Long Russian Energy Suppliers To Europe

Chief among these is Gazprom (OGZPY: OTC US) and Rosneft (RNFTF: OTC US). At the recent Sohn Investment Conference, a top annual hedge fund industry gathering which we covered here, Bloomberg TV caught fund manager Jim Grant giving a bullish call on Gazprom. His reasons:

- It’s cheap, selling at 2.5x earnings versus 10x in 2006, reflecting much of the worst case scenario ahead already being priced in

- In pays a roughly 5% yield (assuming FACTA related issues allow that dividend to reach you).

- It has a terrific balance sheet, with debt payments covered 40 times over by operating cash flow

See here for further details.

Long European Firms With Heavy Russian Exposure

The list would include most of Europe’s largest companies in virtually every sector , given that Russia is Europe’s third largest trading partner after the US and China. For example, Siemens (manufacturing), consumer goods (Renault, Nestle), and of course as noted above, banking (Deutsche Bank, Société Générale’) and energy (BP).

Beware Shorting Other European Gas Suppliers

Although tensions may send non-Russian sourced gas and oil suppliers higher (VET, STO, etc.) we’d be reluctant to short them on the basis of an assumed drop in demand once Russian energy supply fears ease. The current crisis has been a wake-up call for Europe to diversify its energy supplies, so these sources are unlikely to suffer as tensions ease.

The Usual Suspects

Of course expect most risk assets to get hurt if we get a sustained period of real sanctions, so global stocks and risk currencies could well drop. The USD, JPY, and CHF, as the leading safe haven currencies would be beneficiaries. Given the radical inflationary policies of Japan, any JPY spike would make a tempting entry point.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts. For information on a free intro to currencies video course based on my award winning book, see here.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.