EURUSD Weekly Technical, Fundamental Forecast June 8, 2014: Huge Lessons, And Coming QE-EU?

FX Traders’ weekly EURUSD fundamental & technical picture, market drivers, likely EURUSD direction

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we cover outlooks for the major pairs for the coming week and beyond.

Summary

- Technical Outlook: Near term bullish, medium term neutral. As suspected we indeed got our “sell the rumor buy the news” bounce after the ECB fully met but did not exceed expectations. Odds favor some follow through higher to test likely resistance levels this week.

- The big technical question: With bearish uncertainty about ECB easing gone, will the pair resume its usual tracking of risk appetite as portrayed by the S&P 500 and other leading Western indexes?

- Fundamental Outlook: Summary of ramifications of the ECB’s package, what it meant and what it didn’t, and whether this and other fundamentals support a bounce.

- Trader Positioning: The bearish and bullish.

EURUSD Weekly Technical Outlook: Bullish As Strong Support Withstands ECB Easing, Odds (And Fundamentals) Favor Bullish Bounce

EURUSD Weekly Chart October 20, 2013 to Present

KEY: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange. Green downtrend line from EURUSD peak of July 2008 to present, green uptrend line from August 2012 to present.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

01 Jun. 07 22.27

Key Take-Aways Weekly Chart: Likely Trading Range This Week

As the weekly chart above shows, strong support held through the worst the ECB could throw at it. This support is buttressed by five layers of converging support:

- –The round 1.355 figure itself

- –The green uptrend line dating from mid-2012

- –The 50% Fibonacci retracement of the downtrend from mid-2011 to mid-2012.

- –The 38.2% Fibonacci retracement of the bigger downtrend from July 2008 to June 2010

- –Most importantly, the psychologically critical 50 week (aka 200 day) EMA in the 1.355 zone. For many medium and longer term traders, when something breaks below its 200 day moving average, that’s the time to exit longs and open short positions.

The pair managed to stabilize, and even close slightly higher for the week at 1.3643. Given the failed deep probe of lower support and fundamental outlook described below, the odds favor some follow through to test higher towards the next major resistance around 1.37 area comprised of the following elements:

- The psychologically significant round number of 1.37 area itself, which is the high close of the past 3 weeks.

- Convergence of both 10 and 20 week EMAs.

A confirmed break beyond that level opens the door for a test of the long term downtrend line around 1.376.

Thus the week’s range is likely within the 1.364 to 1.376 area.

Likely Trading Range For Coming Weeks

Looking beyond the coming days, the pair remains in its 17 week trading range, within its double Bollinger ® band neutral zone, suggesting that the pair remains with trading range in the coming weeks.

The fundamental outlook discussed below makes a solid case for the EURUSD having found a floor, but offers no compelling evidence for a serious attempt to break above the 1.39 area that comprises the top of that range.

The Bullish Wildcard: Will The EURUSD Resume Tracking The Indexes?

That said, with uncertainty over bearish ECB moves over for the coming months, the pair is now once again free to resume tracking overall risk appetite as reflected by the S&P 500 and other leading US and EU indexes, as it did before the ECB’s May hints of coming easing steps in June.

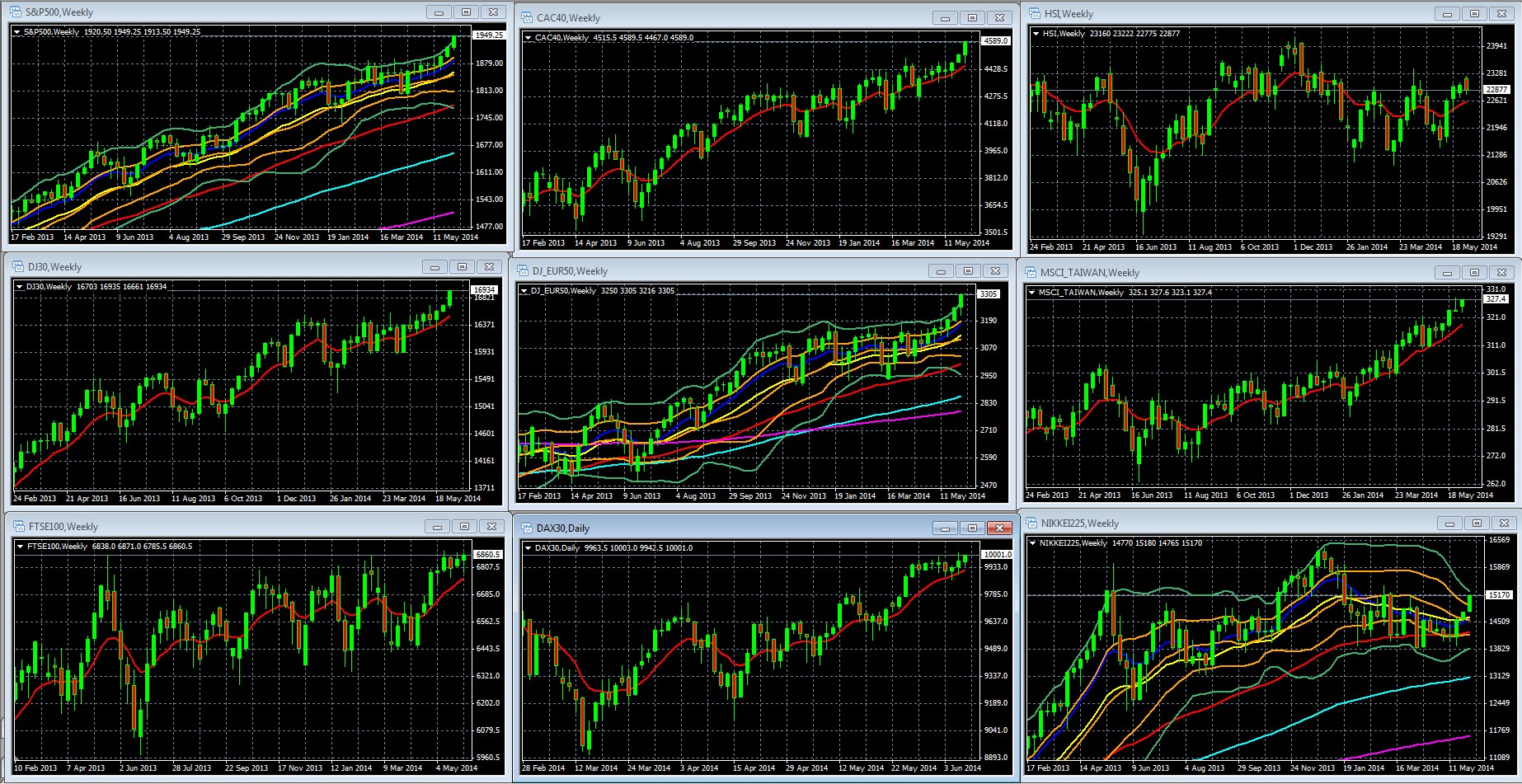

That adds another bullish element to the purely EURUSD technical picture. These indexes have all been moving higher and mostly remain firmly within their double Bollinger® band upper or “buy” zones that suggest the odds favor continued uptrend on the weekly charts.

Weekly Charts Of Large Cap Global Indexes February 17 To Present: With 10 Week/200 Day EMA In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

Key For S&P 500, DJ EUR 50, Nikkei 225 Weekly Chart: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

05 Jun. 08 01.46

The EUR’s best hope for a bullish breakout past that 1.376, then 1.38 areas, lies with its quickly reconnecting with the continued bullish risk trends displayed in these indexes. If the pair starts playing catch-up after a month-long disconnect it could be right back around 1.39 in short order.

Longer term the USD should eventually attain its long anticipated rate advantage, but that remains a distant prospect still about a year away at earliest per the current consensus.

Fundamental Outlook:

ECB Stimulus Steps

This was the biggest event for forex markets of the year thus far, and may prove to be the event of the year. We’ve prepared a special report detailing the key elements, lessons, impact, and likely future direction of the new stimulus package here.

Here’s a summary of the top ramifications for forex traders.

- Draghi says more coming if needed. This bit of forward guidance was arguably the key item.

Here’s why:

- –It will be needed and so it will come. Obviously the ECB alone cannot fix the EU’s problems. It’s only a central bank (in many ways less powerful than most). It’s not a government. All it can do is buy time for the politicians and policy makers, with more supportive policies. It can’t replace the needed increased political unification not the widespread needed economic reforms which that integration would make possible. Heck even the bank union plan completed earlier this year still needs to be funded sooner, and be faster to deploy.Given that its coming is only a matter of if, not when (for these and other reasons as we predicted back in January here):

- –May Limit EUR Rally: It limited the short covering/buy the rumor sell the news rebound into the weeks’ close and could do so in the coming week. Even though no new measures are likely due for months, investors may well want to take some time to digest the move. Anticipated ECB attempts to “jawbone” the EUR lower should keep EUR bulls cautious. No doubt the ECB was hoping for further EUR weakness, and would like to contain the current rebound. The verbal intervention has already started, as ECB Executive Board member Benoit Coeure reminded France Inter radio on Saturday that ECB rates should remain lower than those of the US and UK in coming years.

- –EU Data Now Gains Influence Versus US Data As Markets Speculate On Coming “Q.E.U”/”QE-EU”: Thus EU policy is still in flux at the very time when Fed policy is widely viewed as set for the foreseeable future (for reasons we gave in our special report here). That’s significant because it means markets now become more sensitive to EU data than US data. The Fed and ECB still dominate the pair’s fate, so news continues to influence the pair largely to the extent that it’s believed to influence the respective central banks. The ECB should be seen as more sensitive to monthly data than the Fed, making EU top tier reports more important in moving the pair (and other markets) than they’ve been in the past.

- –As we saw when new QE plans were on the menu in the US, expect markets to move with the data believed to determine timing and scope of the likely coming “Q.E.U.” As we discuss in our special report, the ECB is already moving faster in that direction. Anyone doubting that should note that the traditional German opposition to any such potentially EUR dilutive and inflationary moves has disappeared. The only question now is not when but how much Germany will accept. This alone is a sea-change in EU potential EU policy options. Inflation-phobic Germany now truly sees deflation as at least as big a danger as inflation.

- –That said, neither the ECB nor Fed appear likely to make further policy changes for the coming months, if not the coming year. As we detailed in our special report here, after QE ended no further tightening moves are anticipated beyond minor, token steps amounting to about 25 bps per year. The ECB will likely give the current steps time to take effect before doing more. That leaves the pair to move with any changes in the respective US and EU benchmark rates and overall risk appetite as reflected in leading Western indexes like the S&P 500, which it generally tracks fairly closely. As noted above, if the pair resumes tracking these indexes it should move higher. If investors think it’s time for the EURUSD to play catch-up with those indexes (now that uncertainty about ECB easing of the past month is gone) the rebound could be strong and fast.

- Impact of the combination of refi-rate cuts and negative deposit rates:

- –Should help interbank lending and liquidity. It’s less clear if these steps will actually boost lending to the non-financial corporations, SMEs, and households (ex-mortgages).

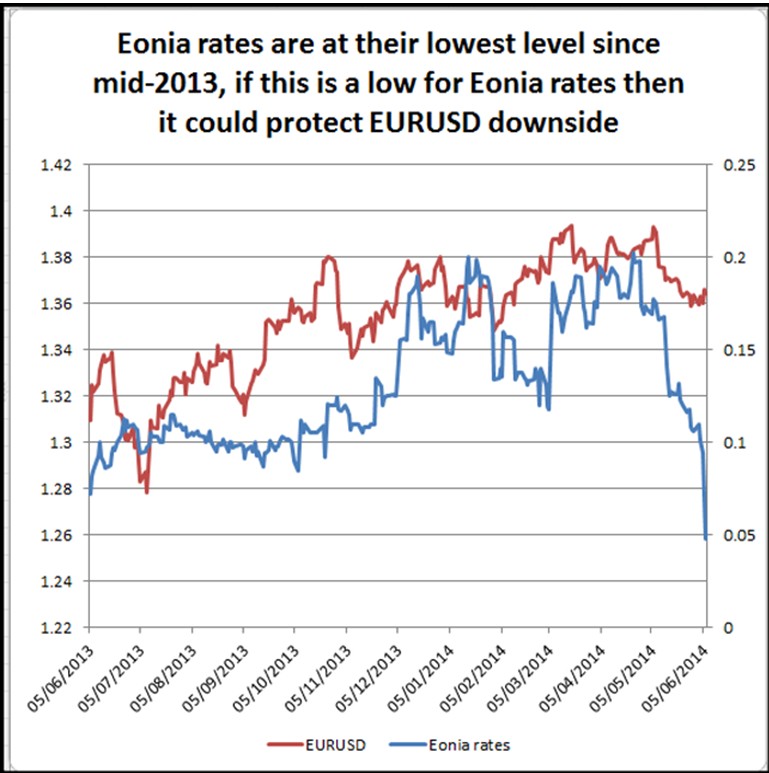

- –Draghi indicated rates cuts done. If in fact that means Eonia rates (which are based on ECB rates) have bottomed, that too should support the EUR and help prevent further declines.

Source: forex.com here

06 Jun. 08 01.59

- Why stocks cheered but forex yawned. All US and European stock indexes moved higher on the news and closed higher on the week, while the EURUSD barely moved. In essence, forex markets anticipated the ECB better than stock markets.

- Beware of Unintended Consequences: This new easing should to some degree have the usual effects of big new stimulus packages. For the EURUSD, the ones of most interests are the risk of feeding asset bubbles everywhere but particularly in the EU and US. The biggest risk is that it sends even more cash into GIIPS assets, making the risks from these fragile economies all the greater.

Again, full details on these see our special report here.

Trader Positioning

Evidence Builds That US Rates Tumble Is Temporary Short Covering Bearish Because Suggests Coming Rate Bounce

The Commitment of Traders (COT) for the 10-year Treasury note futures two weeks ago showed short positions getting cut back. Last week’s report, the most recent we have, shows traders again showed a small net gain in short positions, so the short covering that drove down 10 year yields (and supported the EURUSD) appears done for now.

Latest COT Shows EURUSD Could Get Some Bounce From Short Covering

In addition to the technical factors cited above, another reason to believe in a EURUUSD bounce this week is that per the most recent COT reports, before Thursday’s ECB announcement speculators had the smallest long position since last July and the largest gross short position since last August.

In contrast, the smaller but real-time sample of retail traders shown below shows traders essentially split between longs and shorts.

Source: forexfactory.com

03 Jun. 08 01.20

May US Jobs Report Irrelevant, Losing Influence Too?

The news here is that this usually big, at times climactic monthly report had no impact on the pair. Worth noting:

With the Fed policy widely believed to be set (for reasons we cited in depth here) for the foreseeable future unless it sees key trend changes in inflation, jobs or other top tier data, one month’s data means little. That means the jobs reports are generally less influential than a year ago, when every report was seen as possibly moving sentiment on Fed policy, particularly the coming, dreaded QE taper.

The report was in-line with expectations and the ongoing slow but steady recovery theme, thus further reducing its impact to zero.

US Data Continues To Outperform EU

The past week’s reports showed US data continuing to show slow but steady recovery. US jobs, manufacturing, car sales, inflation data either met or beat expectations. Meanwhile the EU continues showing weakness.

Here’s a chart showing how things have mostly worsened over the past month.

Source: bkassetmanagement.com here

04 Jun. 08 01.37

Note in particular the weakness in German inflation data. No wonder Berlin has softened its stance on inflationary policies. Remember too that the last batch of GDP reports showed multiple core EU nations, including France, on the brink of recession.

Top Calendar Events To Watch

Sunday: China trade balance

Monday: Nothing likely to materially influence the EURUSD, Swiss, French, German bank holidays. Forex brokers open but lower liquidity that can make for very low volatility, but occasionally very dramatic volatility if sudden major surprises.

Tuesday

China: CPI, PPI y/y

US: JOLTS job openings, said to be an important metric now for the Fed, however US jobs announcements have lost some of their importance because the Fed’s policy is believed to be set for now. For reasons we discussed two weeks ago in our special report 2014’s Biggest New Investment Theme: Lower US Rates For A Much Longer Time, fed policy is believed to be fixed in dovish mode for the foreseeable future unless there are major changes in the current “slow but steady” US recovery story, be they bullish or bearish. Thus market sentiment on Fed policy direction is no longer influenced by any one month’s labor statistics, as it was back when fed policy was seen as more fluid and influenced by each month’s jobs data. Monthly jobs reports will only again become more influential again when they appear to be forming a new trend, be it bearish (implying more dovish fed policy) or bullish (suggesting faster tightening and rate increases).

Wednesday: Nothing likely to materially influence the EURUSD.

Thursday: US retail sales, weekly new jobless claims

Friday:

China: Industrial production y/y, fixed asset investment ytd/y

US: CPI, PPI, m/m, preliminary UoM consumer sentiment

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts. For information on a free intro to currencies video course based on my award winning book, see here.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.