The Coming Week’s Top Market Movers, Lessons: A Normal Bull Market Correction?

How bullish and bearish forces align for stocks, indexes, forex and other global markets, both technical and fundamental outlooks, likely top market movers.

Summary

–Technical Outlook: Regional divergences and their implications

–Fundamental Outlook 1: The state of the key market underpinnings and other lessons

— Fundamental Outlook 2: Likely market drivers for the coming week

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we cover outlooks for the major pairs for the coming week and beyond.

Technical Picture

We look at the technical picture first for a number of reasons, including:

Chart Don’t Lie: Dramatic headlines and dominant news themes don’t necessarily move markets. Price action is critical for understanding what events and developments are and are not actually driving markets. There’s nothing like flat or trendless price action to tell you to discount seemingly dramatic headlines – or to get you thinking about why a given risk is not being priced in

Charts Also Drive Markets: Support, resistance, and momentum indicators also move markets, especially in the absence of surprises from top tier news and economic reports.

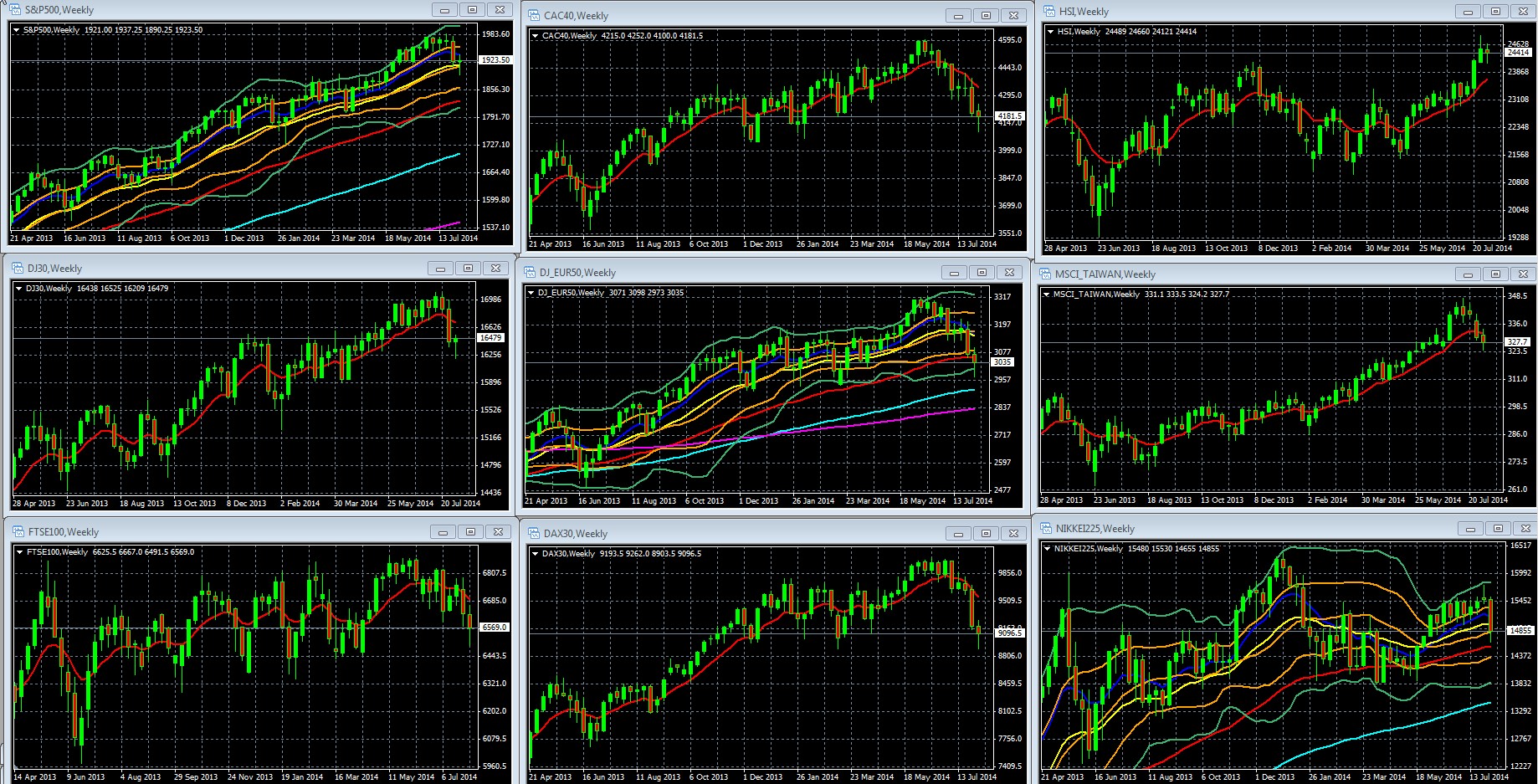

Overall Risk Appetite Medium Term Per Weekly Charts Of Leading Global Stock Indexes

Weekly Charts Of Large Cap Global Indexes April 21 2013 – Present, With 10 Week/200 Day EMA In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

Key For S&P 500, DJ EUR 50, Nikkei 225 Weekly Chart: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

06 Aug. 09 21.42

Key Take-Aways

The pullback in global indexes, and the implied risk aversion, continues. It has now officially reached the US indexes as they log their second straight week in their double Bollinger® band neutral zone. It could have been worse. For example, the S&P 500 would likely have closed the week much lower, and below key support at 1900, if Russia had not announced an end to military “exercises” on Ukraine’s border.

The risk aversion driving global markets has caused some kept the USD up despite falling treasury yields, as investors’ focus on safety rather than yield. See our fundamental analysis for more on that.

US and Asian indexes still look noticeably healthier than those in Europe.

Note how the S&P 500 and Nikkei remain in their double Bollinger® band neutral zones, so the odds are they stay in flat trading ranges in the weeks ahead. Note also how they’re in the upper half of that neutral zone, which means they’re not far from re-taking their upper Bollinger® band buy zones and resuming upward momentum. They also remain in overall uptrends.

In contrast, the DJ Eurostoxx50 closed out the week in its double Bollinger® band sell zone, which suggests more downside ahead. Note also that all of our sample European indexes have more developed downtrends.

What are the fundamental drivers behind these charts? See the below on market drivers and lessons for the coming week and beyond.

FUNDAMENTAL PICTURE

Lessons

How You’ll Know If The Bull Market Is Really Ending

We remind readers that the bull market in stocks and other risk assets has been driven mostly by low rates and lack of any big fear factor to drive investors to low yielding safe haven assets. Note that:

- -Rates Likely To Remain Low: This bullish support hasn’t changed. Even the Fed if/when the Fed starts raising rates (estimates for that starting range from late 2014 to late 2015), it is unlikely to make more than symbolic rate increases, like 25 bps/ year. We’re not alone in that assessment.

- –Last week Goldman Sachs reported that 10 year treasury yields would not hit 4.5% until 2018. This may be a bit too fast. The Fed itself projects 3.75% by 2018, and we don’t see 4% until sometime in 2020 at earliest.

- –Doubleline fund’s CEO Jeff Gundlach, Wall Street’s reigning Bond King, who was one of the few bond fund managers to correctly call the 2014 slide in rates (from their already modest levels), predicted a new round of QE in 2020 in an com interview last week.

- No Big Risk-Aversion Drivers Yet: They’re growing, as noted above, but markets are hardly running scared at this time. The pace and extent of market declines thus far don’t qualify as anything more than a minor normal bull market correction. Russia-Ukraine related sanctions have yet to have a material impact on markets, and Mideast turmoil has not materially influence oil supplies.

Therefore the fundamental drivers of the bull market remain in place. Keep that in mind as you read the financial press and try to distinguish between the bull and the market.

Just for reference, the S&P 500’s 200 day exponential moving average (EMA) is around 1870, and so to would be other variations on the 200 day moving average. A confirmed break below the 200 day moving average is widely viewed as an indication that an asset is heading lower. Obviously we never base our decisions on any one indicator, but I thought I’d throw that one out as a warning sign of rising likelihood of a more extended correction at minimum.

Europe Remains The Weakest

The above noted chart trends simply reflect how economic data out of Europe remains weaker than that of the US and Asia. For details see the fundamentals section of our EURUSD weekly outlook here, where we summarize the latest batch of weak data, banking woes, and how the #3 economy in the EZ is now in recession. This situation is unlikely to change in the coming months, as it struggles under the dual burdens of a dysfunctional currency union and greater vulnerability to the economic effects of ongoing turmoil with Russia and the Middle-East.

US Continues Slow But Steady Improvement

US data continues its modest recovery theme.

The four week moving average for weekly jobless claims fell to 293.5k, its lowest since February 2006. This says nothing about the quality of those jobs, and we know middle class incomes remain stagnant. Still, it’s a positive sign.

ISM services PMI was solid, though ignored, because its main news value is as a leading indicator of the monthly US jobs reports, which had come out earlier due to a rare scheduling quirk.

US GDP beat expectations last week, however the figure was widely held suspect as the product of inventory build-up that could foretell future poor GDP if demand doesn’t soak up those goods.

US household debt remains high: As Russ Koesterich of The Blackrock Blog details here, US consumer debt remains high. This not only casts doubt on how well US retail sales can grow while incomes remain stagnant, it also has very negative long term implications for US growth, as US households are aging overall. High debt and slow wage growth doesn’t sound like a recipe for a financial security for the huge cohort of baby boomers approaching retirement in the coming decade. Matthew C. Klein at FT Alphaville presents further details of the sad state of US households’ financial condition and retirement prospects (via Jeff Miller).

Asia Mixed

Japan has seen a recent slowdown in manufacturing activity and exports. Meanwhile, China’s trade balance on Friday crushed expectations (47.3 bln vs. a forecasted 26.0 bln).

Top Market Movers

Geopolitically Driven Risk Aversion

Overall the indexes made their big moves down on rising fears of a Russian invasion of Ukraine, and of another, increasingly damaging, round of economic sanctions that would follow. Friday’s bounce came on relief that Russia appeared to be pulling back.

Data Less Influential

A lighter economic calendar and lack of material surprises from top-tier data has meant that the weekly economic calendar’s events have taken a back seat to geopolitics.

Top Calendar Events To Watch

The coming week’s calendar is a typical mid-month “middle-weight” with few top tier events. Europe has the second quarter GDP reports from Germany, France and the Eurozone along with the German ZEW survey. For the USD, the top event is US retail sales. The Fed is believed to watch the JOLTS report carefully, though we doubt it will influence Fed thinking in the near term.

Saturday: China CPI, PPI (y/y)

Tuesday

EU: German, EU, ZEW economic sentiment survey

US: JOLTS job openings

Wednesday

Japan: Preliminary GSP q/q

China: Industrial Production y/y, fixed asset investment ytd/y, retail sales y/y,

EU: Industrial production, German 10 year bond auction

US: Retail sales, business inventories m/m (relevant because the recent bullish GDP figure was questioned due to high inventories), 10 year bond auction, NFIB small business optimism survey

Thursday

EU: French, German, EU prelim GDP q/q, EU final CPI y/y

US: Weekly new jobless claims (currently trending lower, bullish for the USD and thus bearish for the pair if that continues

Friday

US: PPI m/m, Empire state mfg index, TIC net long term purchases of US assets by foreigners, capacity utilization (an indicator about future trends in jobs, capex), industrial production, prelim UoM consumer sentiment

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts. For information on a free intro to currencies video course based on my award winning book, see here.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.