EURUSD Coming Week Technical, Fundamental Outlook & Why USD Rising While Rates Fall

Why there’s fundamental and technical evidence to support a bounce this week, and why the pair’s prospects remain firmly bearish. An FX Traders’ weekly EURUSD fundamental & technical picture

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we cover outlooks for the major pairs for the coming week and beyond.

Summary

- Technical Outlook: Short term neutral, medium term bearish

- Fundamental Outlook: Neutral to bullish if Ukraine situation stays calm, longer term fundamentals remain bearish, favoring USD gains.

- Why USD remains resilient despite falling US rates

- Top questions for EURUSD traders

- Real Time Sample Trader Positioning: Our sample continues to be a solid guide for what not to do.

TECHNICAL OUTLOOK

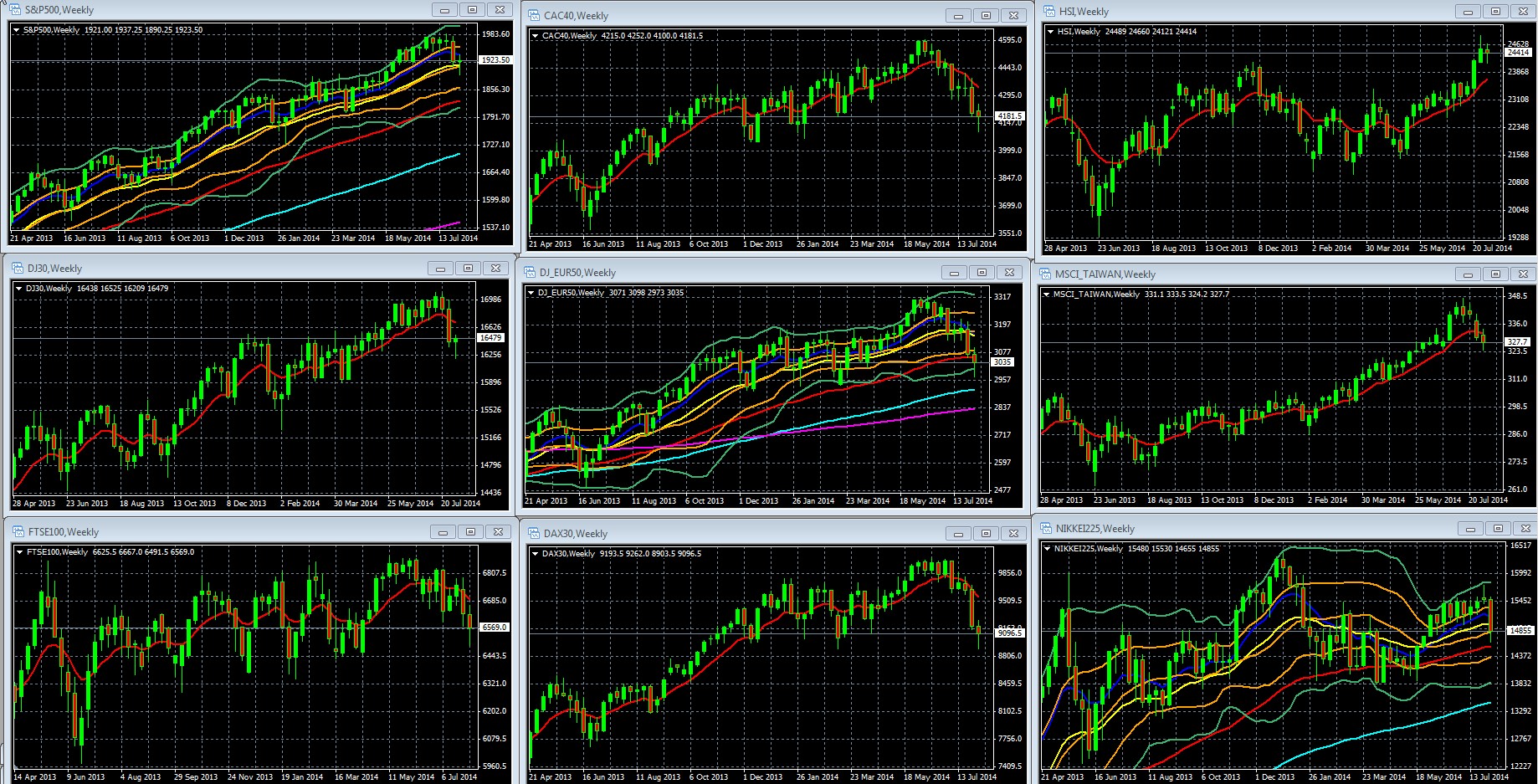

First we look at overall risk appetite as portrayed by our sample of global indexes, because the EURUSD has been tracking these fairly well recently.

Overall Risk Appetite Per Weekly Charts Of Leading Global Stock Indexes

Weekly Charts Of Large Cap Global Indexes April 21 2013 – Present, With 10 Week/200 Day EMA In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

Key For S&P 500, DJ EUR 50, Nikkei 225 Weekly Chart: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

06 Aug. 09 21.42

Key Take-Aways Geopolitically Driven Risk Aversion Adds Bearish Context

The pullback in global indexes, and the implied risk aversion, continues. It has now officially reached the US indexes as they log their second straight week in their double Bollinger® band neutral zone. It could have been worse. For example, the S&P 500 would likely have closed the week much lower, and below key support at 1900, if Russia had not announced an end to military “exercises” on Ukraine’s border.

The risk aversion driving global markets has caused some kept the USD up despite falling treasury yields, as investors’ focus on safety rather than yield. See our fundamental analysis for more on that.

EURUSD Weekly Technical Outlook

EURUSD Weekly Chart July 15 2012 to Present

KEY: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange. Green downtrend line from EURUSD peak of July 2008 to present, green uptrend line from August 2012 to present. White Fibonacci retracement lines for downtrend of August 2008 To June 2010, yellow Fibonacci retracement lines for downtrend of May 2011 To July 2011.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

07 Aug. 09 21.57

Key Take-Aways Weekly Chart: Short Term Bottoming, Medium Term Remains Bearish

Continuing from last week, the medium term outlook continues to deteriorate from a variety of technical perspectives, chart patterns, support breakdowns, and strengthening downwards momentum. In addition, the pair continued its slow grind down within its descending channel from May after a 5 week breakout above it.

That said, support at the 200 week EMA continues to hold and has slowed the decline to the point where we may have a near term bottoming, particularly if the fundamental driver behind the recent decline – the Ukraine situation – continues to ease. Here are the details.

- -Bearish Head And Shoulder Pattern Gets Further Confirmation: The past weeks additional declines, after the prior week’s pause (due to a below-forecast US jobs report), confirm the bearish medium term pattern. It’s hardly a classic H&S pattern given the head is dispersed over a few weeks and the somewhat asymmetrical and lopsided shoulders in December 2013 and June 2014 (the June shoulder’s a bit lower).

However the principal behind the H&S pattern applies here. That is, a failed attempt to rally, followed by further declines that suggest the EURUSD’s rally that began in mid-2012 is officially over.

Note the specific elements of the Head and Shoulders Topping Pattern:

- –We’ve a temporarily successful bounce off late January lows and drive a to new highs from December 2013 to March 2014

- –A pullback that bottoms in mid-June

- –A failed rally that tops out in early July, which, significantly, topped at resistance created by the medium term uptrend line dating back to June 2012, which proved its strength by resisting 4 straight weeks of tests. The current move lower has created a new series of lower lows and lower highs, aka a downtrend. The technical evidence of the new downtrend also includes violation of key support as detailed below.

- -Violation Of Key Support: Over the past 4 weeks the pair has broken through no less than 3 strong support levels, within which were 5 key technical support indicators:

- –1.3575 area, which also includes the term 38.2% Fib retracement of the long term downtrend beginning August 2008 – June 2010 (white).

- –13560 zone, which also includes the 50% Fib retracement of the medium term downtrend from May – July 2011 (yellow), and the 50 week (200 day) EMA (red)

- –The 1.3455 area, which includes the 100 Week EMA (turquoise)

- –The 1.3400 support area, which includes the very significant 200 Week EMA (violet), is closer to breaking. Last week it held, thanks to the weaker than expected US NFP and unemployment reports (and thus reduced USD rate hike speculation). This week it bent further but ultimately held, again thanks to some positive Friday news, the end of Russian military exercises on Ukraine’s border.

- -Accelerating Downward Momentum

- —All EMAs trending lower except for the longest term, least sensitive 100 and 200 week EMAs, which have flattened. The 10 and 20 week EMAs (red and yellow) are close to crossing below the 50 week EMA (red), which would signal more entrenched momentum, as does…

- —The pair completes its 9th straight week in the DBB sell zone, and its 3rd straight week of hugging the very bottom of this zone.

- Remains In The Middle Of Its Descending Channel (pink): NB: we’ve widened that descending channel compared to last week, in order to better reflect the true price range and downward slope, and allow for normal counter moves like we saw in June.

Likely Trading Range For The Week Ahead

Looking at both weekly and daily charts for the EURUSD:

Upside limited to around 1.345, where it would meet resistance from prior week highs as well as from its 10 and then 20 day EMAs, and 100 week EMA.

Downside appears limited to around 1.333, the lows of the prior week, in which the pair survived bearish data, geopolitical events, and ECB comments. More on these in our fundamental analysis.

The recent violations of support and accelerating downward momentum open the way for a test of the next meaningful support level around the 1.333 zone, which provided support and resistance at 4 different times on the weekly EURUSD chart in 2013. After that, there’s no meaningful medium term support until around the 1.330 – 1.3255 band, which includes both these psychologically important round numbers as well as the 38.2% Fibonacci retracement of the May 2011 July 2012 downtrend.

Concluding Thoughts

The unequivocal message from the weekly charts is that the pair will find itself lower in the months ahead, albeit with the usual short term bounces.

The 200 week EMA, the last big medium term support level, has bent more but has yet to break. When it does (and the above bearish picture indicates it will), there is nothing to stand in the way of the strong downward momentum, as detailed above.

Fundamental Outlook: Top EURUSD Market Movers

Top EURUSD Drivers: Risk Aversion, Data Advantage Boost USD Despite Falling US Rates

Risk Aversion Trumps Lower USD Yields

The pairs 2 big moves, on Tuesday and Thursday, illustrate how risk aversion has the pair’s key fundamental driver.

The big drop for the pair came on Tuesday despite falling US 10 year Treasury note rates, mostly due to rising fear over the impact of additional exchanges of economic sanctions between and the West (though poor Spanish unemployment data EU PPI didn’t help the EURUSD’s performance either).

The pairs’ big move up for the week came on Friday, in response to reduced fears of a Russian invasion of Ukraine as Russia ended military exercises on Ukraine’s border and began pulling back its forces.

Although USD resilience in the face of falling US yields seems odd, history has shown that when risk aversion is paramount then investors will buy both Treasuries (thus driving rates lower) and the USD, both top safe-haven assets. For example, we saw this behavior during the Great Financial Crisis and 9/11.

US Data Advantage, ECB Comments Fuel Speculation On Coming USD Rate Advantage

The other key fundamental EURUSD drivers last week were the continued better US economic data and dovish ECB comments.

Economic activity in the Eurozone was revised lower for the month July due to slower growth in the service sector. Improvements in Spain were offset by weakness from Germany and Italy. Perhaps this data, and the recent losses in the euro, had investors positioning for more dovish ECB comments at the coming Thursday ECB meeting.

These negatives were somewhat offset by News of Portugal’s Banco Espirito Santo rescue (even though hitting bank shareholders and junior bondholders with losses will hurt this and similar banks’ chances for future access to capital via share offerings or additional debt sales).

Italy tipped into recession on Wednesday. A surprise second consecutive contraction in Italy’s economy, per 2Q GDP figures, pushes the Eurozone’s third largest economy back into recession. Bad as this is by itself, it also carries additional, spreading ramifications beyond falling Italian stocks and rising in Italian yields.

As we’ve noted repeatedly, particularly in our posts about the failed EU banking union, none of the real causes of the EU crisis has been addressed, nor have there been any meaningful reforms to prevent another round of EU contagion risk. The complacency about EU crisis risk, born of ECB president Draghi’s great bluff in 2012 that the ECB actually could do all that was needed, rests mostly on sheer confidence that everything will somehow work out, despite the lack of reforms or meaningful growth.

This latest recession risks raising the record low borrowing costs for Italy and the rest of the GIIPS and it could metastasize into a crisis if that a sustained spike in rates comes, and starts a rapid outflow of the capital buildup of the past two years. As Portugal’s BES troubles have reminded us, the EU’s periphery is on its own if they face a bank failure. There is no Fed-like safety net or anything like it, as the banking union doesn’t even exist yet and even when it does, will have too little money and too much bureaucracy to support confidence that the EU can respond quickly to banking crises in member nations, even those that threaten to spread to all of Europe and beyond.

In contrast, US data continues to support the slow but steady recovery theme. The last monthly jobs reports missed forecasts, but not by much and were still over 200k. The 4 week moving average of weekly new jobless claims continued falling after beating the latest forecasts, and services PMIs beat forecasts.

Given the above US growth advantage over Europe, it’s no surprise that ECB President Draghi used the ECB’s monthly press conference to remind markets of the coming USD interest rate advantage, as the Fed would likely raise rates long before the ECB, perhaps even before the ECB had even finished easing.

Granted, one could dismiss his remarks as another attempt to jawbone the EUR lower, however the reality of the US’s better economic performance and lower exposure to Russian economic sanctions compared to Europe, justify the ECB’s taking a more dovish position than the Fed.

EURUSD Lessons For The Coming Week

So, what did we learn for the coming week and beyond?

Highlights, Summary Of ECB Policy

Highlights of Draghi’s remarks from the ECB’s monthly rate statement and press conference include:

- USD Rates Will Be Higher Than The EUR’s For A Long Time: The Fed is winding down its own QE and is expected to begin raising rates by no later than late 2015, possibly as early as late 2014. The ECB is still looking to ease further and has no timetable for raising rates.

- More Stimulus Coming: The ECB is intensifying its preparation for some kind of outright purchases of asset-backed backed securities as an additional form of stimulus.

- The ECB Views EU Recovery As Slow, Uneven: It’s slow even in the more prosperous countries, and non-existent in many of the weaker ones. As noted above, on Wednesday Italy had officially tipped into recession.

- ECB Is Worried About Economic Effects Of Russia Sanctions: On Thursday Russia banned food imports from the European Union in response to the financial sanctions enacted by the EU last month. Although it’s too soon to assess the economic damage, Russia is the world’s 5th largest food importer. The prospect of rising energy prices is a longer term concern, although for now crude oil prices are trending lower.

EU’s Weaker Economic Performance Vs. US Continues

- Peripheral Banks Under Suspicion With BES Bailout: The Portuguese bank woes have shaken confidence and risk renewed scrutiny on peripheral banks and the lack of EU safety net, even after the banking union that was agreed on earlier this year

- Italy Falls Back Into Recession: Last week Italian GDP contracted for a second consecutive quarter for the third time since the start of the GFC.

02 Aug. 08 18.26

- EZ Retail Woes: Even German retailing is weakening.

03 Aug. 08 18.28

- German Manufacturing Slowing On Reduced Europe Demand: Even without considering the loss of Russian, business, Germany’s economic mainstay, manufacturing, is suffering from falling demand from its neighbors.

Source: Deutsche Welle (via WALTER KURTZ, SOBER LOOK)

04 Aug. 08 18.30

(via businessinsider.com here)

05 Aug. 08 18.36

In contrast, US data continues to show a slow but persistent improvement.

When Risk Aversion Is Strong, USD Can Rise With Falling US Rates

To reiterate what we noted above, although currencies generally rise or fall with their benchmark interest rates, that’s not the case with the USD when fear is high, because that risk aversion not only drives up demand for dollars, it also drives up demand for US Treasuries and thus sends treasury yields lower.

Top Calendar Events To Watch

The coming week’s calendar is a bit light, with Europe having most of the events likely to move the pair. The most important EUR calendar events are the second quarter GDP reports from Germany, France and the Eurozone along with the German ZEW survey. For the USD, the top event is US retail sales. The Fed is believed to watch the JOLTS report carefully, though we doubt it will influence Fed thinking in the near term.

Saturday: China CPI, PPI (y/y)

Tuesday

EU: German, EU, ZEW economic sentiment survey

US: JOLTS job openings

Wednesday

Japan: Preliminary GSP q/q

China: Industrial Production y/y, fixed asset investment ytd/y, retail sales y/y,

EU: Industrial production, German 10 year bond auction

US: Retail sales, business inventories m/m (relevant because the recent bullish GDP figure was questioned due to high inventories), 10 year bond auction, NFIB small business optimism survey

Thursday

EU: French, German, EU prelim GDP q/q, EU final CPI y/y

US: Weekly new jobless claims (currently trending lower, bullish for the USD and thus bearish for the pair if that continues

Friday

US: PPI m/m, Empire state mfg index, TIC net long term purchases of US assets by foreigners, capacity utilization (an indicator about future trends in jobs, capex), industrial production, prelim UoM consumer sentiment

Biggest Questions & What To Watch To Answer Them

- Will treasury yields continue to fall, and if so, will the USD remain resilient? As noted above, if geopolitical events continue scaring investors, then the EURUSD remains under pressure. If markets relax, then the pair likely gets a bounce this week.

- Will the risk aversion sentiment ease? The main thing scaring markets was the risk of a Russian invasion of Ukraine and the economic damage of further sanctions that would follow. Russia appears to be pulling back. If so, then that would support the pair and likely allow it to attempt a bounce off of the strong support levels where it closed last week. Mideast events have yet to have a major impact on risk appetite, and won’t until oil supplies are threatened. However we’ve already got reports of suspended production from certain oilfields in Iraq.

- Is the EURUSD downtrend over? For the coming week, if the Russia-Ukraine situation doesn’t escalate, then probably. Longer term, the Eurozone’s economic weakness, and the EURUSD’s technical weakness on the weekly charts, both point to further moves lower, as noted above.

Sample Retail Traders Positioning

Forex factory’s real time sample of retail trader positions shows:

- A modest shift to short positions from the prior week.

- Since July traders shifted strongly to the long side, anticipating a resumption of the uptrend that never happened, and stayed long regardless of the trend’s continued moves against them.

08 Aug. 09 23.48

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts. For information on a free intro to currencies video course based on my award winning book, see here.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.

{kind=link}