Lessons For The Coming Week: More Life & Debt Issues, EU Fracture Signs

Part 2: Lessons, threats, likely market movers for the coming week from Europe, Emerging Markets, China, technical and fundamental issues for the week ahead and beyond that touch all major global asset markets

The following is a partial summary of the conclusions from the fxempire.com weekly analysts’ meeting in which we cover the key lessons learned for the coming week and beyond.

See here for Part 1.

TECHNICAL PICTURE

As we discussed here, the two week rally in global stock indexes shows, market fears of EM contagion threats have calmed.

WEEKLY CHARTS OF LARGE CAP GLOBAL INDEXES WITH 10 WEEK/200 DAY EMA IN RED: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, RIGHT: CAC 40, DJ EUR 50, DAX 30

KEY FOR S&P 500:10 WEEK EMA DARK BLUE, 20 WEEK EMA YELLOW, 50 WEEK EMA RED, 100 WEEK EMA LIGHT BLUE, 200 WEEK EMA VIOLET, DOUBLE BOLLINGER BANDS: NORMAL 2 STANDARD DEVIATIONS GREEN, 1 STANDARD DEVIATION ORANGE

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

02 feb 15 2056

The general picture is one of recovering uptrends and upward momentum as markets believe that there is no current threat that continued turmoil in emerging markets will spread like the US subprime crisis did back from 2007-2009.

FUNDAMENTAL MARKET DRIVERS

As noted in Part 1, Janet Yellen’s dovish testimony and willingness to blame recent US data on the temporary effects of bad weather helped boost markets last week. Here in Part 2 we look at lessons and market movers for the coming week from the rest of the world.

EUROPE

Data, Share Prices, EUR Steady-Higher, But Eroding Support, Banks Threaten In 2014

The past weeks have been a study in contrasts for the EURUSD.

On the surface the quantifiable things are mostly steady-higher. We’ve somewhat improving earnings results, economic data, and fund flows into European equities (versus outflows from US and Asian stocks), and continued complacency about EU crisis reemerging. The EUR remains in its overall uptrend since 2012.

Looking past the numbers and charts however, the seeds of the EU’s next crisis, if not its demise, are there to see.

Many have pointed out that although there isn’t broad popular support is for ceding real sovereignty and control over national budgets and how they’re disbursed, the elites continue to push ahead, either with or without awareness of their voters’ opposition.

For example, Jens Nordvig, head of Nomura’s fixed income department and author of The Fall of The Euro, argues persuasively that despite support among many of the EU’s elites, the lack of popular support for the needed integration to become the United States of Europe dooms the EU, and then spends the rest of the book looking at the different ways the EU can break up and how investors can best prepare for the EU’s ultimate demise.

Over the past week, however, that lack of popular support appeared on the official level in three different locales:

- Switzerland’s vote against free immigration into Switzerland

- Scotland’s edging closer to an independence vote, and the UK’s warning to Scotland that it won’t be allowed to keep the pound if it votes for independence

- The German Constitutional Court’s ruling on the legality of the OMT: As we discussed last week here, the Court didn’t simply refer the decision to the EU’s highest court. It also said that as far as Germany is concerned, the OMT program (that allows the ECB to become buyer of last resort for sovereign bonds) it illegal and therefore German participation (aka funding) is unlikely at this time.

Going a bit further back to the end of 2013, we then have the failure to of the single resolution mechanism to be the effective safety net for failed banks that it needed to be in order to restore confidence in EU banks, prevent another banking crisis, and allow the coming ECB bank stress tests to be rigorous enough to uncover all of the weak banks without risking a crisis from finding too many undercapitalized banks and no safety net for them. We’ve written a lot from November – January on this lurking disaster, for example, see here. In short, it is as US Treasury Secretary Jack Lew said, too small and too slow to be effective.

Why?

It’s too small because leaders of the wealthier nations do not want to have their voters held liable to pay for bank bailouts due to the corruption and/or mismanagement of others. Thus they’re phasing in the common fund over 10 years, and even those funds will only be available after funds from bank shareholders, bondholders, and larger depositors have been exhausted

It’s too slow because the individual states retain most of the decision making power to disburse funds, the result being that any disbursement must pass a long series of bureaucratic steps.

This week there will be progress reports on the SRM from the Eurogroup and ECOFIN meetings, so we may get some meaningful updates.

EM UPDATES

Although markets don’t see the current EM travails as a threat to the global rally, there are potentially market moving developments brewing that merit watching.

Ukraine On The Brink Of Default- Or Worse?

On Friday there were multiple reports that Ukraine is nearing default. Markets are reflecting the strong possibility.

FT.com reported that the yield on a $1.6bn bond of Naftogaz, Ukraine’s state gas company, due on September 30, had gone from an “apocalyptic” 30% to 34% in the past month and was still rising as of Friday. A combination of capital flight and short term debt ($65.8bn in ST debt falling due over the next 12 months) coming due that vastly exceeds its foreign currency reserves of less than $18 bln.

Source: Thompson Reuters

02 feb 17 1619

Here’s the Hryvnia (UAH) to the US dollar rate (UAHUSD) over the past few months.

Source: Thompson Reuters

03 feb 17 1623

The chart below shows the rising cost to of default insurance on Ukraine 5 year notes.

Source, DB, Sober Look

01 feb 17 1608

Euronews reports: – Financial experts have warned Ukraine is on the brink of default with some saying currency reserves are enough for only two months. Russia has provided the first three billion dollar tranche of a loan. With the political stand off the rest has been frozen. (via soberlook.com)

For those who haven’t been following it, the “political stand off” is essentially a battle over the fundamental future direction of the Ukraine, towards Western democracy and joining the EU (ok, perhaps not the ideal way to orient Westward) or towards slipping closer to its former status as a Russian vassal, whether technically still sovereign or not.

Some analysts warn that Russia could escalate its pressure on the former Soviet republic.

Stephen Blank of the WSJ wrote: Behind its coercive diplomacy in Ukraine is the threat of force, either incited by Russia or carried out by it. Recent reports of pro-government militant groups forming in eastern Ukraine, calls in the Crimean legislature for Russia to “rescue” them from Ukraine’s anti-government uprising, and repeated discussions in the Russian media about partitioning Ukraine, all point to a pattern of escalating pressure from Moscow—a pattern that paves the way for the use of force.

We don’t believe there is a contagion threat here, simply because Ukraine isn’t part of a larger currency union that risks being discredited if it doesn’t support Ukraine, and the nation is far from being a mainstay of the global economy.

Its potential market threat is more from its potential for geopolitical tensions if Russia gets more aggressive.

Kazakhstan: Great Success? Not

Kazakhstan devalued its currency 17%, the latest country to succumb to rate pressure on emerging markets. The tenge fell more than 100 points against the dollar. I’m sure there’s a Borat joke or reference to be found in this. Ideas anyone?

We would also remind readers that the EM crisis is not over. Not only is the US moving towards higher rates (and that alone has sent EM rates higher), so is China. Speaking of which…

CHINA – Can PBOC Tighten Without Causing Hard Landing?

China’s capital markets remain dangerously volatile, and threaten the feared ‘hard landing’ in which China’s economy contracts and sucks the global economy down with it.

China continues to aggressively pursue deleveraging, the main goal of which to reduce the size and scope of China’s sprawling and risky shadow finance sector, which is estimated to account for roughly one third of the financial system by size.

Thus far the damage has been contained to China’s bond market, sending commercial lending rates soaring.

Via FT.com

06 feb 17 1736

The big risk is that the deflationary impact will be felt worldwide. Per Ambrose Evans-Pritchard in his recent article entitled “World asleep as China tightens deflationary vice“…

China’s Xi Jinping has cast the die. After weighing up the unappetising choice before him for a year, he has picked the lesser of two poisons.

The balance of evidence is that most powerful Chinese leader since Mao Zedong aims to prick China’s $24 trillion credit bubble early in his 10-year term, rather than putting off the day of reckoning for yet another cycle.

This may be well-advised for China, but the rest of the world seems remarkably nonchalant over the implications.

As part of this process, the PBOC’s tightening, it is sowing fear in the hearts of risk taking investors seeking yield by allowing “trust” or “wealth management products” (essentially Chinese versions of junk bonds) to fail. Thus far the defaults have not been official, rather they’ve been classified as “delays of payments.”

Demand for these products has plunged.

Since January, 9 firms have delayed or canceled debt issuance plans (around $1 billion). These are privately-owned companies, which lack an implicit government guarantee, and which are too unstable to find cheaper credit via standard bank channels.

Non-performing loans in China have surged to post-crisis highs.

Source: Bloomberg (via zerohedge.com

04 feb 171719

The big fear is that China will be unable to contain the problem once real defaults begin (as opposed to the “delays of payment” seen thus far).

As FT.com reports here, the PBOC’s stimulus reduction is actually on a larger scale. The Fed has cut back bond purchases by $10 bln/month for the past 2 months. The PBOC has been cutting $83 bln/month for over 6 months.

GFC, EU Crisis Parallels

Remember, the GFC began with similar turmoil in the US banking sector in 2007-8.

The EU crisis began after the semi-sovereign fund Dubai world delayed payment on its debt in late 2009, and that got markets looking at other potential sovereign defaults from the ongoing global slowdown. They quickly found Greece, and the rest is history.

Implications of China Hard Landing

In 2013, Chinese economic growth slowed to 7.7%, its lowest level since 1999. A “hard landing” is generally defined as at least 2 quarters of year-on-year growth to 2%.

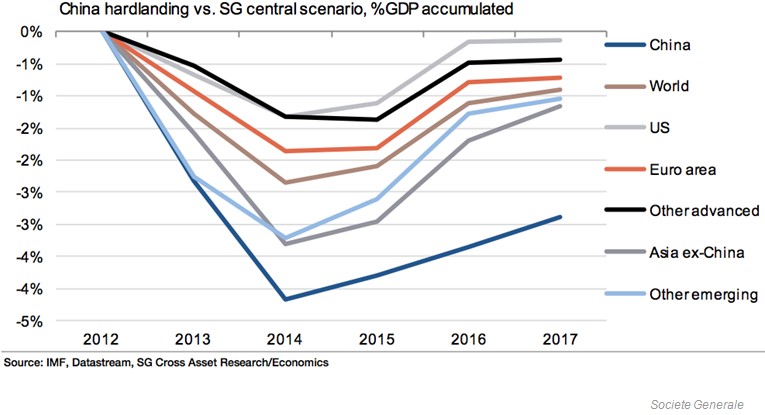

Per Societe Generale, This alone would cause a 30 % plunge in Chinese equities, a 50% crash in copper prices, and a dive in the price per barrel of Brent crude to $75. Imports account for 30% of China’s GDP, so its suppliers (most nations with significant export) would suffer badly. Its Asian suppliers would be worst hit, but keep in mind that China is even the US’s biggest single customer.

Just for illustration, here’s a chart on the global implications of a hard landing.

Via businessinsider.com here

07 feb 17 1754

Of course the true impact of a China hard landing is difficult to gauge, with EMs struggling and the EU, US, and Japan in what are at best weak, vulnerable recoveries.

That said:

Societe Generale’s current central scenario is for 6.9% growth.

The PBOC is quite aware of the stakes. As Reuters reported on Saturday:

China’s banks disbursed the most loans in any month in four years in January, a surge that suggests the world’s second-biggest economy may not be cooling as much as some fear.

Chinese banks lent 1.32 trillion yuan ($217.6 billion) worth of new yuan loans in January, beating a 1.1 trillion yuan forecast and nearly three times December’s level, the People’s Bank of China said in a statement on Saturday on its website.

Again, the big question is whether China, like the US and other nations, can walk the tightrope of a gradual deleveraging (reduction in debt levels) without causing a new global recession.

Perhaps the bigger question is whether the PBOC, Fed, and other central banks can do this at the same time.

As always, I look forward to your comments and questions.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.