The EU: The End Is Near? Existential Threats And Decisions Approach

As evidence of the EU’s failure and potential collapse mounts, the time for existential choices approaches

Summary

- Existential Threat #1: Unsustainable Debt Loads That Could Destroy The EU Require A Fully Empowered ECB

- Existential Threat #2: Undercapitalized Banks Present Systemic Risk To EU, Global Banking. This too requires a fully empowered central bank that can act fast with needed cash

- Implications: A US of Europe, but apparent lack of political will and popular support for implied loss of member state sovereignty may doom the EU

With EU stock indexes badly underperforming those of the US and Asia, EU economic data varying between weak growth and deep recession, and the EUR looking terrible from all angles, (details here), it’s no surprise that many are again focused on the EU’s depressing state and what can be done about it.

Here we’ll focus on just two existential threats that were in focus this week, and their immediate solutions and broader implications for the EU.

Existential Threat #1: Unsustainable Debt Loads That Could Destroy The EU

Low bond yields for the EU’s periphery indicated that the crisis remains in hibernation

Back in January of this year I argued here that the EU would ultimately have to choose between its own economic collapse and accepting massive money printing to fund a US or even Japanese style central bank stimulus program.

The past week saw an outpouring of articles concluding the same, from far more credible writers than yours truly.

I’ll summarize the key points of just three of them, then attempt to draw some practical, usable conclusions for profiting and protecting yourself based on both these articles and whatever I can add. I recommend reading the full posts.

First, there was Barcelona based economist Edward Hugh’s The Italian Runaway Train. It analyses Italy’s economic prospects and debt situation, and what’s likely to happen if the ECB doesn’t ride to the rescue with a QE/sovereign bond buying program big enough to matter to the EU’s third largest economy. Key points include:

Italian sovereign debt levels are unsustainably high and its weak economy and aging population indicate Italy cannot lower its debt/GDP ratio by growing enough to meet EU debt/GDP targets. Unlike Greece and Portugal, Italy’s sovereign debt is too big to deal with via the relatively painless steps used for these smaller nations, more lending of printed money to fund extend and pretend policies.

Regardless of what economic policy Italy pursues to recover from its current recession, its debt level is likely to rise.

- –If Italy chooses the EU-recommended route of spending cuts and other austerity measures, its debt/GDP problem remains, because GDP would likely shrink as fast, or faster, than it can cut debt. This route is less likely given the political resistance to the likely short term (?) further cutting of GDP

- –If Italy rejects that approach and seeks to stimulate growth with more debt in hopes of raising GDP faster than its total sovereign debt (an Italian version of Japan’s Abenomics), that debt still grows. This is the likely path as it produces at least some short term growth and austerity has not proven effective anyway as it has tended to shrink GDP and so leave debt/GDP unchanged or worse.

Italy is moving very slowly with reforms, but it doesn’t have the luxury of time, because markets will soon realize that it will ultimately default unless someone buys Italian bonds in order to keep Italy’s borrowing costs low – a European style QE currently illegal per the EU’s Maastricht treaty which forbids ECB funding of member states’ debt. However it’s unlikely that Italy can convince Germany, and other nations that would fund the ECB’s bond buying, that Italy could ever repay the ECB.

Thus at some point Germany and other funding nations refuse to risk becoming liable for an Italian default (as if that would be the only one in a world of financial contagion). They would want to let the bond owners take the loss, not the taxpayers.

In the near term, markets will remain calm due to the belief that Draghi not only intends to do “whatever it takes,” but that he actually has the ability to do so. Unless the ECB can find some way around the Maastricht treaty’s ban on printing money to fund sovereign debt, he can’t. The ECB’s mandate does include maintaining price stability, so perhaps that would provide the needed excuse.

In another related article, What Is The Risk The Euro Crisis Will Reignite?, Hugh argues that the risk of a new EU crisis is rising because:

Current ECB easing steps are unlikely to ease liquidity enough to combat deflation in the coming six months

So nominal debt/GDP levels of other peripheral EU nations besides Italy are likely to go higher due to a combination of persistent deflation and deteriorating GDP.

The ECB isn’t committed to the kind of large scale sovereign bond buying that might at least preserve bond market calm, leading us to the risk that again, confidence in the ECB’s ability to “do whatever it takes” breaks down as funding nations signal their unwillingness to fund massive ECB purchases of peripheral nation bonds that are unlikely to be repaid.

The Big Lesson

The conclusion I draw from the above is that to avoid a repeat of prior EU sovereign and bank debt crises that would follow from a collapse in confidence in peripheral bonds, the ECB needs to have the power print money needed to buy all the sovereign bonds necessary to keep market confidence up and rates down, inflation risks be damned.

That would add needed credibility to Draghi’s “whatever it takes” promise that halted the spike in Spanish and Italian borrowing costs which threatened widespread sovereign and bank (they hold too many of those the sovereign bonds to survive those defaults) defaults and collapse of the EU’s banking system.

Granting the ECB unlimited power to create all the Euros it needs to buy member state bonds would give those bonds a creditworthiness they’ve never had, because they’d now have a true buyer of last resort, just like the sovereign bonds of every other healthy currency zone.

Business Insider’s Joe Weisenthal’s analysis of Draghi’s Jackson Hole speech made very similar conclusions.

That Draghi mistakenly believed austerity programs imposed on GIIPS nations were necessary and correct. Weisenthal notes the ineffectiveness of these policies shows they were mistakes.

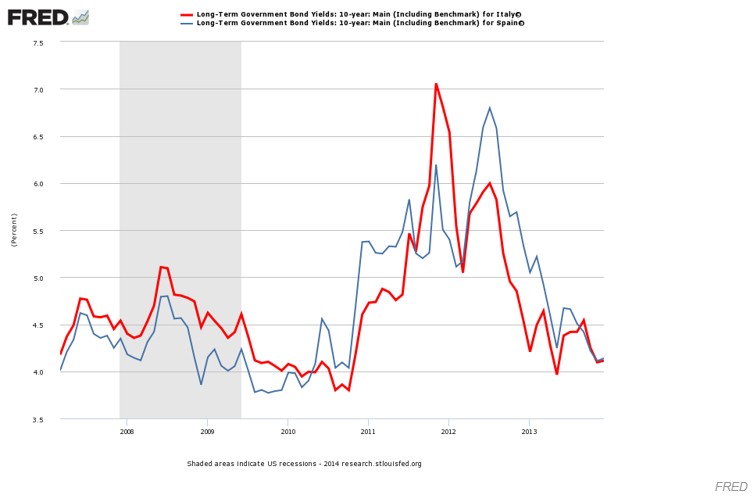

The fact the Draghi’s “do whatever it takes” promise in the summer of 2012 was what actually succeeded in easing the EU crisis by restoring confidence in GIIPS bonds, thus lowering their borrowing costs and removing near term default threats. He provided a useful chart showing how Italian and Spanish bond yields subsequently fell.

03 Aug. 24 17.58

FT.com’s Wolfgang Muchau went further, arguing here that with bond rates so low, even a massive ECB sovereign bond purchase wouldn’t help get yields much lower and wouldn’t get inflation rates higher. He advocates a more radical program in which the ECB buys equities, junk bonds, and subsidizes mortgages. These steps would first need to be legalized.

Like Edward Hugh above, he warns that unless the EU loses its fear of the money printing press, the EU risks “Japanification” as slow growth and an aging population bring intractable deflation and stagnation.

Conclusion

As I recall, the whole objection to ECB purchases of sovereign debt was fear that the implied excessive money printing risked what Germany feared most, inflation. Now that even Germany is suffering from deflationary pressures, and the EU remains an economic disaster, isn’t it time to fire up the money printing presses, and empower the ECB to do whatever it takes, inflation risks be damned?

Those risks are real, but Europe’s economy, like America’s at the start of the GFC, is analogous to a patient suffering from potentially fatal cancer. The chemotherapy may kill him at some point in the future. However without it, the cancer will likely kill the patient in a matter of months.

Existential Threat #2: Undercapitalized Banks Present Systemic Risk To EU, Global Banking

As we’ve written about repeatedly in the past (see here, here, and here) the EU banking union pact is too underfunded and slow to deploy to provide any likely practical help, or credibility, for the stability of EU banking.

We have thus noted that given that lack of real safety net that banks and depositors in the US, UK, and other healthy currency unions enjoy, the coming publication of EU stress tests on October 17th is likely to produce one of two possible outcomes.

–The tests are a joke, similar to the past two tests. The ECB lowers standards so that many weak, unstable banks get passing marks. The ECB recognizes that there are too many banks which don’t have the capital to survive the likely defaults that serious stress tests would reveal. The ECB, lacking the resources to rescue or shut down these banks without inflicting widespread investor and depositor losses that would risk market turmoil (bank runs, stock market and bank crashes, etc.). EU banking’s credibility is again undermined, perhaps fatally if a number of significant banks fail and cause losses for depositors, lenders, and investors.

–The tests are rigorous and reveal that there are numerous undercapitalized banks in peripheral nations that lack the means to recapitalize them or close them without widespread losses to depositors, lenders, and investors. The EU either finds a way to protect them or risks a loss of confidence in EU banks and a new phase of the EU crisis.

The New York Times came out last week with a report on how there’s a growing group of analysts that believe the coming ECB stress tests will be rigorous and thus reveal that EZ banks will need additional cash. Using the “Texas Ratio,” a metric developed to evaluate Texas banks during the Savings and Loan crisis of the late 1980s, a variety of analysts and investment firms using this metric have concluded that far too many EU banks are undercapitalized relative to the size of their estimated bad loans. See here for details.

Implications

The US Of Europe Or An EU Breakup

There are many, but the key idea is that a common currency means a common supreme legislature and central bank with authority over member state budgets. In other words, a United States of Europe, with member states ceding most of their control over their budgets, and thus, their full sovereignty. This is really the choice behind all the others.

Popular Support Lacking?

EU states have resisted this, as popular support for it has been lacking. If that continues, then it’s difficult to see how the EU as we know can make the above reforms needed to survive.

Bearish For European Assets, Especially The EUR.

Regardless of what Europe ultimately decides, the process will likely be messy and reinforce the EUR’s current downtrend. While individual European assets will prosper, investors must consider significant loss from a declining Euro. Just reaching parity with the USD would imply a roughly 25% decline.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts. For information on a free intro to currencies video course based on my award winning book, see here.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.